The Banking System: Turmoil or Crisis? – April 2023 Market Update

A third bank failure this week, First Republic Bank, has left many worrying about another financial crisis like 2008. Are we on the verge of a banking crisis or is this current turmoil related to unique situations at these three banks?

In our April 2023 update, Beacon Wealth Consultants’ Chief Investment Officer Hillary Sunderland, CFA®, CKA® looks at the recent bank failures and discusses:

-

- Is this the beginning of a financial crisis or are these banks unique?

- How is our current situation different than 2008?

- What do we see going on in the market?

If you’re worried about the banking sector, listen to the video below and be sure to rewatch last month’s commentary where Hillary discusses the safeguards in place to protect your assets.

If you have any questions about your financial situation, please reach out to your wealth advisor and we would be glad to address them for you. Thank you for being a valued client of ours.

Full transcript below.

Transcript

Hello, my name is Hillary Sunderland and I’m the Chief Investment Officer for Beacon Wealth Consultants and LightPoint Portfolios. Welcome to the April 2023 market update. Well, over the last few weeks there has been some turmoil in the US Regional banking system, which has understandably increased investor anxiety and has left many wondering whether we are on the cusp of another financial crisis similar to the one experienced in 2008. So in this short video, I hope to address these concerns.

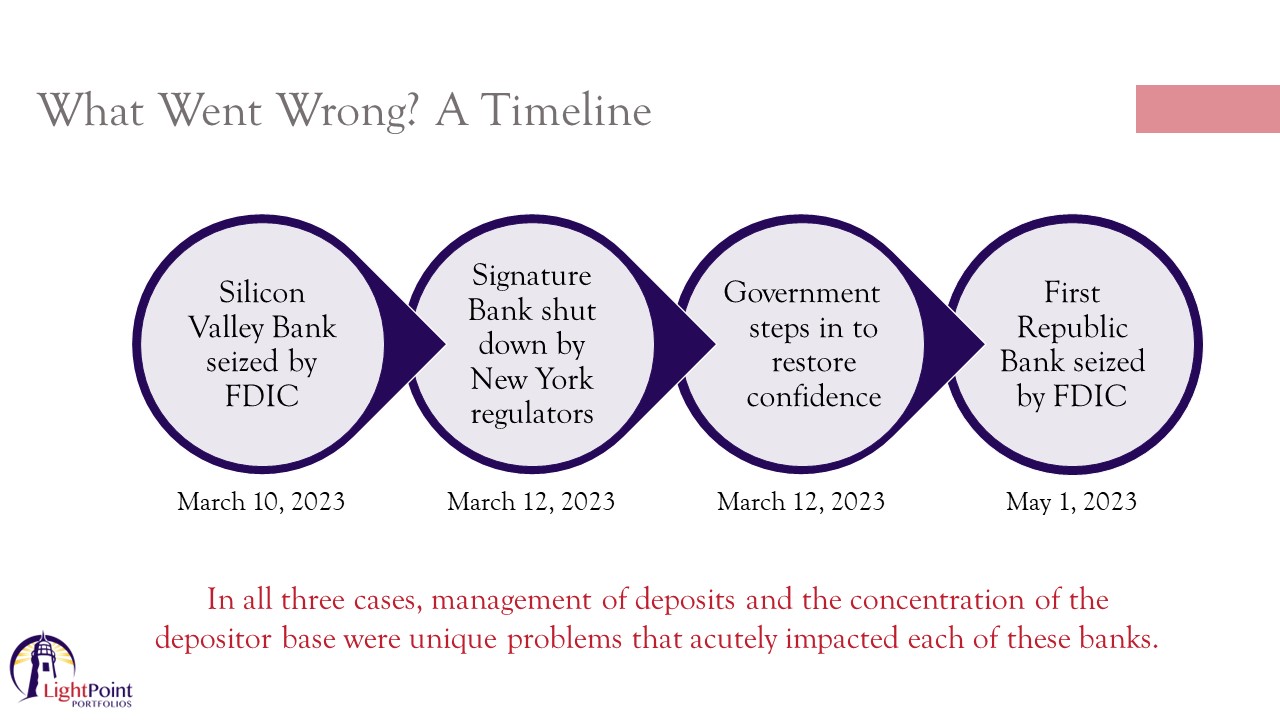

Let’s start by reviewing what has happened over the last few weeks. So in March, Silicon Valley Bank, a regional lender to the tech industry for 40 years with $210 billion in assets, collapsed, and that marked the largest bank failure since the 2008 financial crisis.

Silicon Valley Bank was a unique risk in and of itself. More than 90% of its deposits were uninsured by the FDIC, which is not the norm for banks. And the deposit base at this bank was unusually concentrated in tech startup firms. So as the Fed hiked interest rates at a rapid pace over the last year, the higher rates hit areas of the economy that had benefited the most from cheap financing, which included technology and crypto related firms. And those firms began withdrawing their deposits at a fast pace due to the difficult operating environment.

Now, one of the issues with a rapid withdrawal of funds from the banking system is that banks only hold a portion of the deposit of funds in cash and a large percentage of the funds are invested in bonds and are used to make loans. So as a result, banks are not equipped to have all of their deposits suddenly leave and still be able to maintain liquidity.

This led Silicon Valley Bank into forced asset sales and unfortunately, they had invested in long-term, low interest rate treasury and agency bonds and did not take steps to hedge their portfolio from a rising interest rate environment. This led to a liquidity crunch and then the seizure of the bank by the FDIC on March 10th.

Just two days later, came the fall of New York-based Signature Bank. Signature Bank also had an undiversified customer base. However, their customer base was related to the cryptocurrency industry, and I think we all know why that space is considered to be risky. Signature Bank fell prey to fears of a bank run among those banks who held risky assets. That bank was shut down by New York regulators on March 12th of this year.

So at this point, given that confidence in the banking system is of paramount importance, the Federal Reserve, the US Treasury, and the FDIC stepped in and announced a plan to cover all deposits at Silicon Valley Bank, which helps many well-known companies such as Roku and Etsy, which banked there. They also covered all deposits at Signature Bank.

Additionally, they created an emergency liquidity facility for other banks whereby banks can pledge their assets such as Treasury securities. Now this is important because remember, as long as the bond issuer doesn’t default bond holders, in this case, the banks get back par, which means all of their money if they are able to just hold the bonds to maturity. So the creation of this facility basically allows banks to pledge assets that are currently trading at a loss on their balance sheets, but will most likely mature at par, which is a very nice backstop for the banks.

This step that the government took effectively plugged a $620 billion hole created by the unrealized losses on securities holdings within the banking system.

So now you may be thinking, well, if the move by the government was supposed to restore confidence, why was there another bank failure over the weekend?

Well, First Republic had actually been in the news for quite some time because the bank had characteristics that were similar to both Silicon Valley Bank and Signature Bank. First Republic catered to wealthy clients who rarely defaulted on loans. The bank wooed wealthy clients with very cheap mortgages when interest rates were at rock bottom levels. And then as interest rates spiked over the last year, this made First Republic’s mortgage loans far less valuable to the bank than when they were originally offered to their wealthy customers. Additionally, because the bank catered to wealthy individuals, when Silicon Valley Bank and Signature Bank failed, wealthy customers fled First Republic as well.

First Republic saw unprecedented deposit outflows beginning around March 10th before the government stepped in. And the reason for this is that as of the end of 2022, two thirds of First Republic’s deposits were uninsured by the FDIC, which is very high. This resulted in a classic run on the bank and led to the FDIC taking over the bank on May 1st and then immediately auctioning it to JP Morgan over this past weekend. First Republic has been in a slow decline for some time.

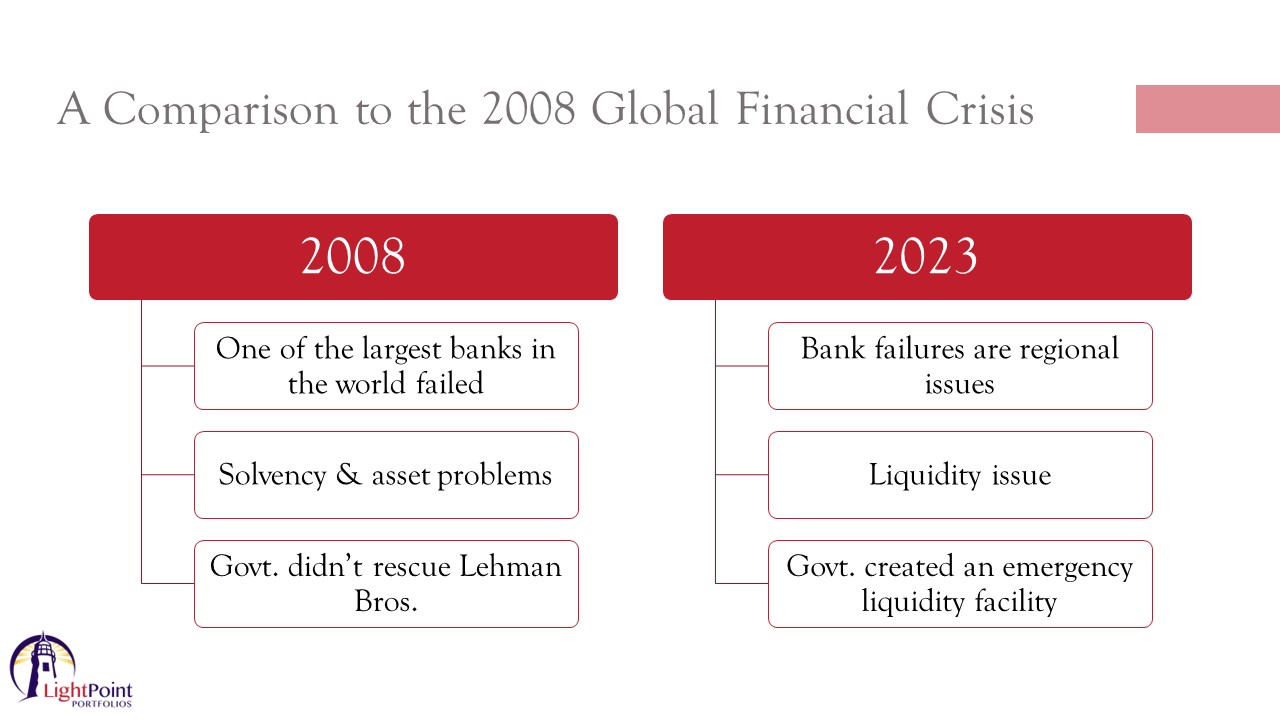

So the point of this is really just to say in all three cases how these banks managed deposits in a low interest rate environment and the concentration of their depositor base were unique problems that acutely impacted each of these banks and led to their downfall. The current banking turmoil that we’re seeing right differs in many respects from the 2008 financial crisis.

2008 was a global financial crisis due to the relevance of Lehman Brothers. When Lehman failed, it was one of the largest banks in the world. The banks that failed in the US over the last few weeks, are regional banks, and they are not on the same stage in terms of their global impact that they could have given a failure.

It’s important to remember that the banking crisis of 2008 was really about solvency and asset problems. In 2008, banks were highly levered and they were thinly capitalized. They had made too many bad loans, both in the form of residential mortgages and subprime as well as in corporate loans. Many banks had too little capital to absorb losses. In comparison to today, bad loans are not the source of today’s banking turmoil. When you look at the asset quality of banks today, it’s good. Today, banks hold more cash, fewer risky real estate loans and have a much lower loan to deposit ratio than they did back in 2008.

The US regional banks that failed over the last two months had solvency but not immediate liquidity due to the losses sustained in their portfolios because of rising interest rates and their inability to hold those assets to maturity due to customer deposit outflows.

Also, it’s important to note that the government did not step in to rescue Lehman Brothers, which led to a domino effect of multiple financial disasters, which eventually became the global financial crisis. This year, the government immediately stepped in to create that emergency liquidity facility to help those banks that are currently experiencing liquidity issues, which should restore confidence in the banking system.

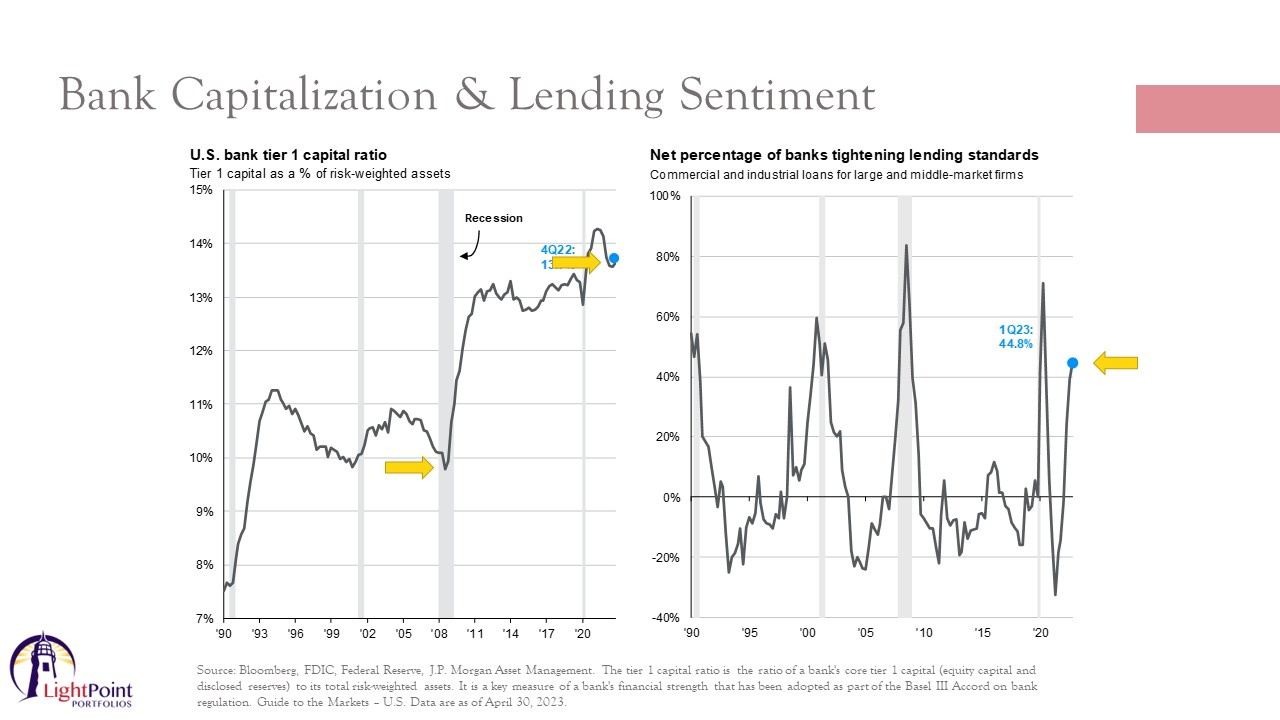

Since they established that facility, mid-size banks have been reporting first quarter results and in many cases we have seen a stabilization in deposits, which is key to restoring confidence in the US banking system. The other thing to note here is that following the global financial crisis, banks were forced to increase capital buffers, which reduces the likelihood of banks running into trouble during economic downturns.

And that’s what you can see on the left-hand side of this chart. The tier one capital ratio is a measure of the bank’s financial strength because it represents the first line of capital available to absorb losses. Currently, that ratio stands near multi-decade highs. You can see here that this chart goes back to 1990 and we are near highs for the tier one capital ratio.

So overall, the banking sector is significantly healthier today than it was during the global financial crisis when tier one capital ratios were around the 10% level. So overall, while there could be some additional weakness that comes through for some regional banks, we’re not concerned that this is going to be a systemic issue that impacts the global financial system. However, that doesn’t mean that it won’t have negative implications for the US economy.

As the chart on the right shows, lending conditions have tightened meaningfully since the second quarter of 2022, and we expect the regional banking turmoil will cause lending conditions to tighten further. Small and mid-size businesses in the US tend to rely heavily on regional banks for their lending needs. So this reduction in capital that is available to businesses will likely be a further drag on economic growth and it does increase the odds of recession.

As we’ve said for some time though, we do expect any recession to be short and shallow given that the labor market still remains strong relative to history. So with this backdrop, where are we now in terms of how markets are performing? It’s often said that markets climb a wall of worry and that is what we are seeing so far this year.

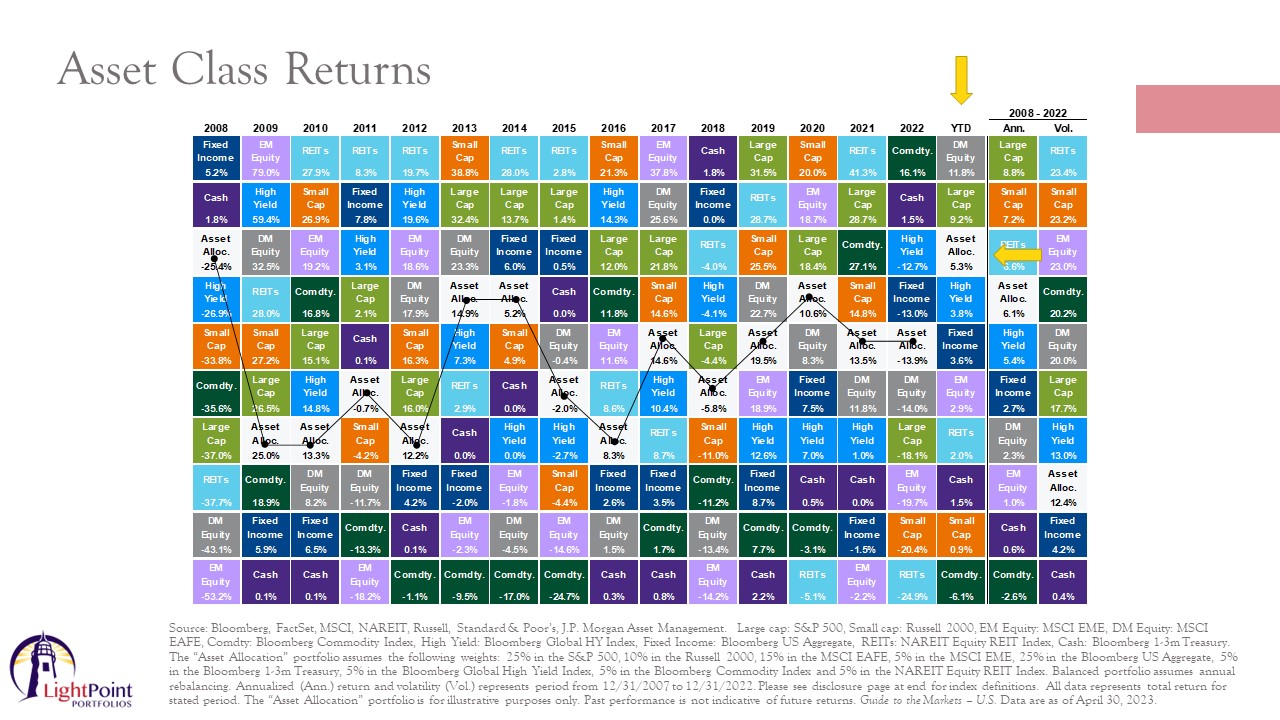

This asset class return slide shows returns for each calendar year since 2008 and it is ranked from the best performing asset class to the worst. Unlike last year, most asset classes are exhibiting positive returns after last year’s losses. Historically, the stock market does tend to bottom prior to a recession even being called as the stock market is forward looking. It’s also very rare to have consecutive years of declines for the S&P 500 index.

One thing you’ll note here is that international developed stocks, the gray box there, has been outperforming domestic. We are seeing very good valuations in international markets in comparison to the United States, and a weakening dollar suggests that international equity outperformance should continue. So for investors with us, we have a healthy percentage of your portfolio dedicated to that asset class in order to capture this trend.

And additionally, after a rough 2022 bonds are looking much more attractive. We have been steadily reducing our exposure to hedges that we put on the portfolio last year in order to increase our allocation to this area. There is the potential for the Federal Reserve to cut interest rates sometime over the next year if we enter a recessionary environment, and bonds are likely to offer income capital appreciation and diversification benefits once again.

Most importantly, as you consider the risks that are on the horizon, it’s important to appreciate the benefits of diversification and what that has offered to you as an investor. That is shown by the white asset allocation boxes on this chart. As this slide implies, it’s very challenging to cherry pick the best and worst performing asset classes each year, whereas a diversified portfolio has delivered investors a smoother ride with solid returns over the long term. And so we remain diversified investors when we are allocating assets within your portfolio.

I hope this review of the current banking turmoil has been helpful for you. We thank you for your continued confidence and please reach out to us with any questions you may have.

Do you know what Business Practices You Are Supporting through your Current Investments?

Or Contact Us to Schedule a Phone Call or Meeting.

Call us today! (540) 345-3891