I’m worried about the banking system. How are my assets protected?

Given the recent bank failures, many people are worried about the safety of their deposits and assets. In our March 2023 update, Beacon Wealth Consultants’ Chief Investment Officer Hillary Sunderland, CFA®, CKA® responds to several common concerns we’ve heard from clients:

- How are my assets protected if a custodian, such as Charles Schwab, fails?

- Charles Schwab also operates an FDIC member bank. Does that mean that my assets are FDIC insured?

- What happens if the mutual fund company I’m invested in fails?

Watch our video to learn more about the various safeguards in place to protect your assets.

If you have any questions about your financial situation, please reach out to your wealth advisor and we would be glad to address them for you. Thank you for being a valued client of ours.

Full transcript below.

Transcript

Hi, my name is Hillary Sunderland and I’m the Chief Investment Officer of Beacon Wealth Consultants and LightPoint Portfolios. Well, given the recent failures of Silicon Valley Bank and Signature Bank, we have received questions from some of our valued clients regarding the banking turmoil. Now, if you have specific questions related to those bank failures, please reach out to me or your wealth advisor, and we’d be happy to address any questions you have regarding these events.

But the purpose of this video will be to answer one of the most commonly asked questions from our clients over the last few weeks, which is, how are my assets protected if Charles Schwab, or a mutual fund company, I’m invested in fails. Let’s jump right in.

Well, as an investment advisor, we are required to maintain client funds and securities with a qualified custodian. A custodian is a financial institution, which is usually a bank or registered broker dealer that holds customer securities for safekeeping. This custodian, in our case Charles Schwab, holds your securities for safekeeping to minimize the risk of theft or loss. They also manage the settlement of financial transactions, account for the status of your assets, and ensure compliance with tax regulations.

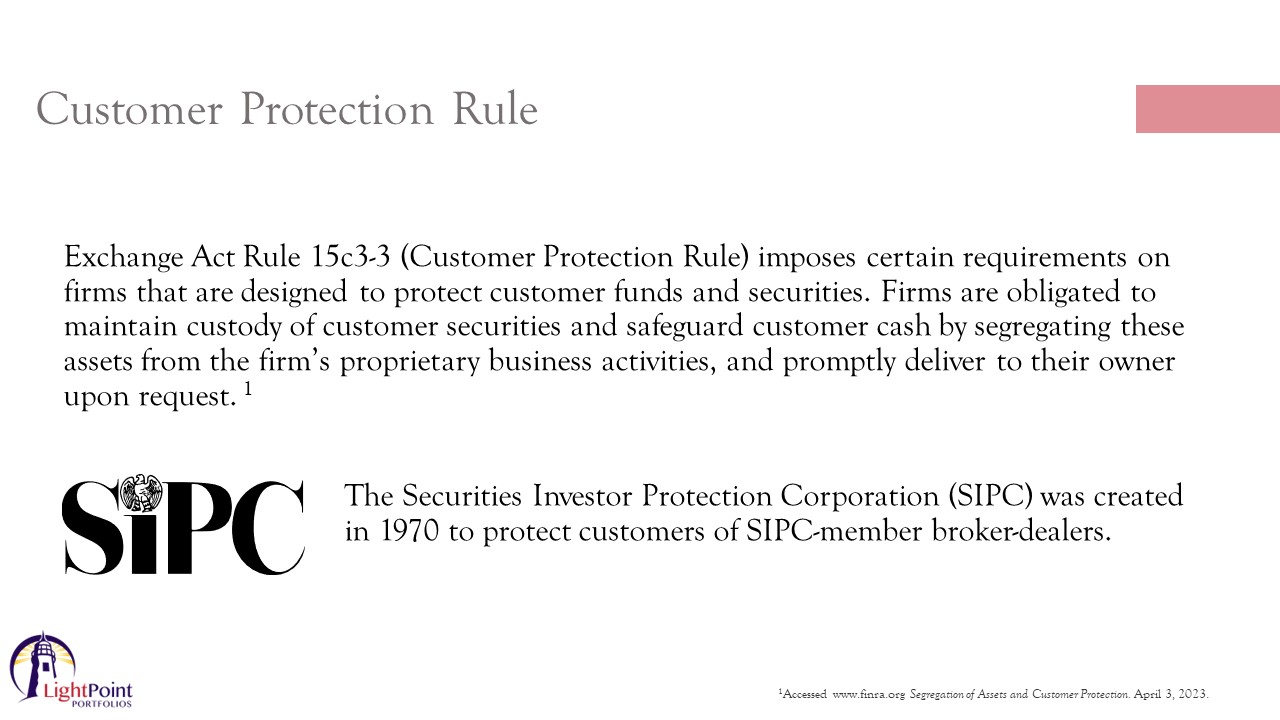

In the unlikely event of insolvency of Charles Schwab, your assets are not available to general creditors and are protected against creditors’ claims. And the reason for this is that Charles Schwab, in compliance with the SEC’s Customer Protection Rule, which is shown here, is obligated to maintain custody of customer securities and safeguard customer cash by segregating these assets from the firm’s proprietary business activities.

They’re also obligated to promptly deliver securities and cash to their owners upon request. So if a firm such as Charles Schwab or another custodial firm were to fail financially, the Securities Investor Protection Corporation or SIPC for short, will step in to get these segregated customer securities back to their owners.

SIPC was created in 1970 to protect customers of SIPC member broker dealers, and what typically happens is that in the event that a custodian needs to liquidate, SIPC will typically ask a federal court to appoint a trustee to liquidate the firm and protect its customers. The trustee will often arrange to have customer accounts transferred to another brokerage firm. Customers then have the option of staying at the new firm or moving to another firm of their choosing.

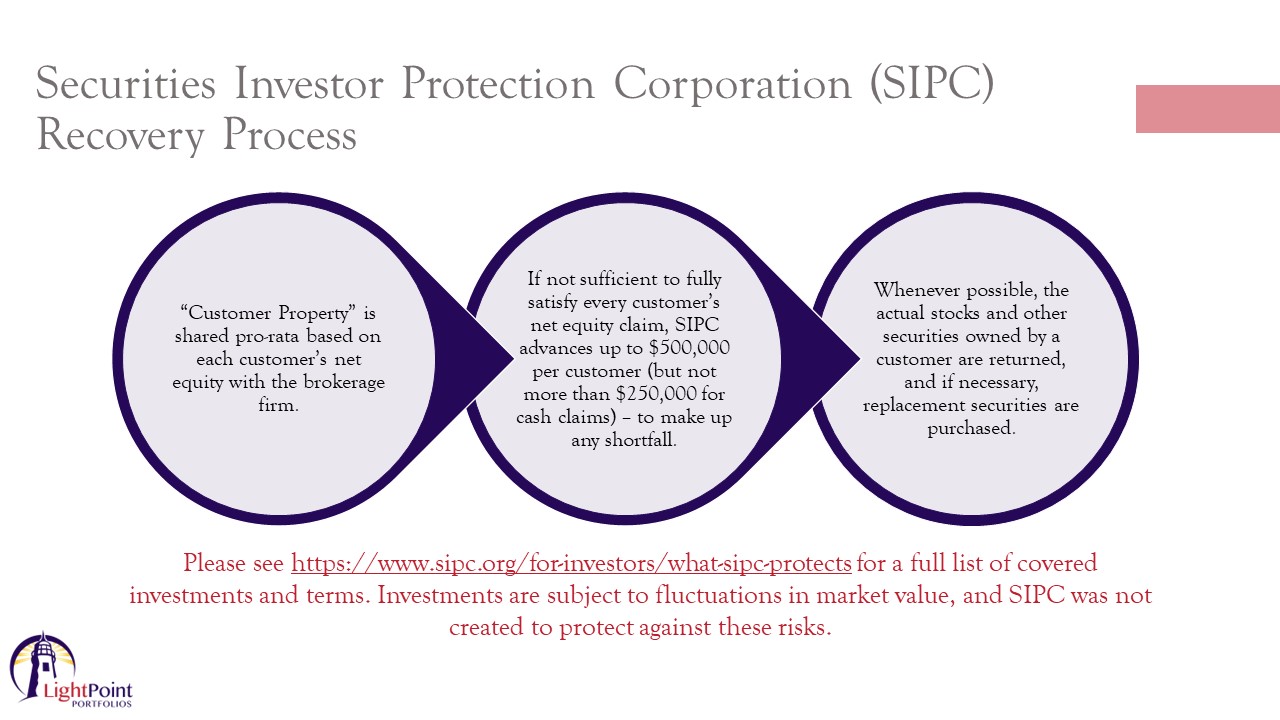

So what specifically does this recovery process look like? Well, in that liquidation of a SIPC member brokerage firm, you would have claim against the brokerage firm in the amount of your net equity, which is the value of cash in securities that you own, minus any debt that you owe to the brokerage firm. The cash and securities held by the brokerage firm is called Customer Property and is shared pro rata based on your net equity.

So for example, if the fund of a customer property consists of 95% of what should have been held by the brokerage firm for customers, then all customers receive 95% of their net equity claims from this fund. Well, in many liquidations, the fund of customer property is not sufficient to satisfy fully every customer’s net equity claim. So in that case, SIPC advances its funds up to $500,000 per customer, but not more than $250,000 for cash claims to make up any shortfall.

Whenever possible, the actual stocks and other securities owned by a customer are returned and if necessary, replacement securities are purchased. Now, an important point to make here is that while SIPC covers the more common investments such as stocks, mutual funds, bonds, certificates of deposits, SIPC does not cover certain types of investments such as fixed annuities or precious metals such as gold and silver coins.

You can visit the website shown here to learn more about the details regarding the $500,000 coverage limit and what securities are covered. Also, please note that SIPC does not protect the value of any security. Investments are subject to fluctuations of market value, and SIPC was not created to protect against market value fluctuation.

So at this point, you might be thinking, well, the SIPC coverage sounds good, but how effective has it been historically in recovering customer assets when a custodian fails? Well, they actually have an excellent track record. According to their website, since 1970, they have made possible the recovery of no fewer than 99% of persons who are eligible to get their investments back. This equates to the recovery of $141.8 billion in assets for an estimated 773,000 investors.

And probably the most high profile case of SIPC account protection was the collapse of Lehman Brothers during the great financial crisis of 2008, SIPC was well suited to deal with the most complex insolvency in history. They fully satisfied the 111,000 customer claims, totaling more than $106 billion. In that case secured, priority, and administrative creditors also received 100% distributions, and they can be commended for a job well done.

So even though we view the failure of Charles Schwab as a highly unlikely event, and even though SIPC has an excellent track record, I wanted to point out to you that when you choose Charles Schwab as your custodian, you actually receive coverage above and beyond SIPC limits.

Charles Schwab provides clients who custody with them an extra level of SIPC coverage. They have selected Lloyds of London, which is a well-respected name in the insurance industry, as underwriter for additional brokerage insurance. This excess SIPC protection of securities and cash is provided up to an aggregate of $600 million, limited to a combined return to any customer from SIPC and Lloyds of London of $150 million, including up to $1,150,000 in cash.

This additional protection becomes available in the event that SIPC limits are exhausted and client accounts have not been made whole. So as you can see here, you have an extensive amount of protection in the event of a Charles Schwab failure. Again, we do not have any concerns with Charles Schwab as a custodian for your assets. Otherwise, we would not have chosen them for you.

So this leads to the next client question. In addition to the brokerage arm, Charles Schwab also operates an FDIC member bank. Does that mean that my assets are FDIC insured? Well, a quick review of FDIC, the Federal Deposit Insurance Corporation is a US federal agency that protects investors against the loss of their deposit accounts such as checking and savings in the event of a failure of an FDIC insured bank.

The FDIC insurance amount is $250,000 per account holder per insured bank for each ownership category. And for more details on the specifics of that, please visit www.fdic.gov. Now, note that the FDIC does not insure money invested in stocks, bonds, mutual funds, life insurance policies, annuities, or municipal bonds, even if those investments were bought from an insured bank. The FDIC covers deposit accounts such as checking and savings.

So you can think of it this way in terms of your account subject to the terms and conditions of SIPC. You have SIPC coverage on securities held at Schwab. You have excess SIPC coverage through Lloyds of London, and you also have FDIC insurance on a portion of your assets.

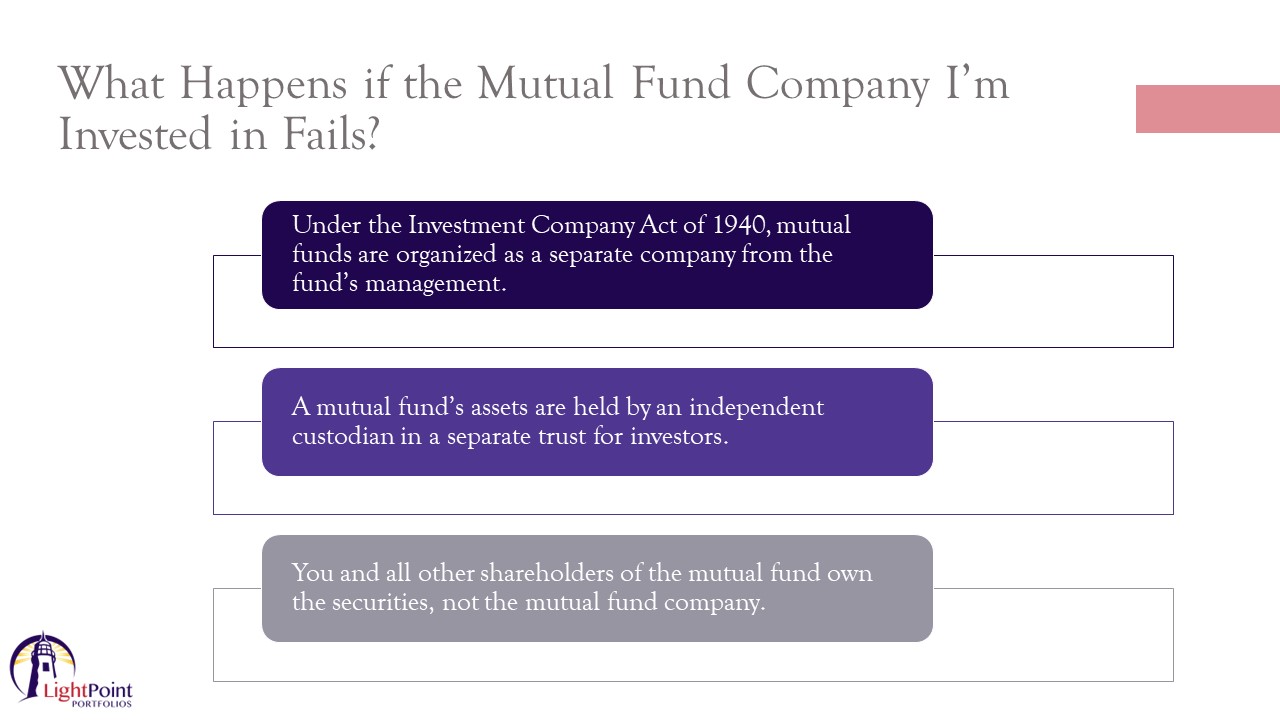

Then finally, for our last question, well, what happens if the mutual fund company I’m invested in fails? Well, this is going be a similar answer to the custodian question. There are several safeguards in place to ensure that your money is safe if a fund management company goes bankrupt. These protections, of course, have nothing to do with the value of the shares, which will rise and fall depending on the value of the underlying investments.

Mutual funds are subject to very strict regulations that protect your money in the event that a mutual fund company goes bankrupt. Mutual funds are under the Investment Company Act of 1940, and as such are organized as a separate company from the fund’s management. A mutual fund’s assets are held by an independent custodian, usually a specialized bank. So even if the fund management company goes bankrupt, it’s creditors can’t touch the money in a mutual fund, which is held in a separate trust for investors. Remember, you are a shareholder in a mutual fund.

Your money is not an asset of the fund company itself. You and all the other shareholders in the fund actually own the securities, not the mutual fund company. In addition to this, mutual funds also must provide detailed reports to the SEC, provide financial reports to shareholders, and are audited annually. So as you can see here, there are many levels of protection in place if a mutual fund company were to go bankrupt as well.

I hope this review of the various safeguards that are in place for your assets was helpful to you. We thank you for your continued confidence and please reach out to us with any questions you may have.

Do you know what Business Practices You Are Supporting through your Current Investments?

Or Contact Us to Schedule a Phone Call or Meeting.

Call us today! (540) 345-3891