by: Cassandra Laymon, CFP®, MBA

As a financial advisor, I’m often asked the question, “When should I start taking my Social Security benefit?” As in all cases of financial planning, there is no one-size-fits-all answer to this question. At the heart of this question is the desire to maximize the amount of money you are collecting. That is a fair question – this is money you and your employers have paid into the Social Security system over your work life. If you haven’t started thinking about Social Security yet, and you’re not sure how it works, I want to walk you through the highlightsand some of the factors you should consider.

First, it’s important to know your Full Retirement Age (FRA) for Social security purposes — the age when you are eligible to receive your full benefit. Currently, FRA is somewhere between 65 and 67 years of age, depending on your birthdate. (Click here to find our your FRA). Even though your full retirement age might be 66, you have the option to start your benefits as early as age 62 or delay your benefits to start at age 70. And that’s where the questions arise…

Simply put, there is an 8% reduction in your benefit for every year you start Social Security before reaching your FRA. On the flip side, there is an 8% increase in your benefit for every year you delay taking your benefit past your FRA (up to age 70). Here’s a real-life example:

At full retirement age (67): $2,460 a month

At age 70: $3,051 a month

At early retirement age (62): $1,728 a month

You can see that there is a $1,323 difference between starting at age 62 and age 70. So, should you take a lower amount early or wait until age 70? In general, it’s better to wait as long as you can, particularly if you are in good health and have family longevity on your side.

Here are some factors that you should consider when making this crucial decision:

• Health status

• Life expectancy

• Need for income

• Whether or not you plan to work

• Survivor needs

I want to stress how important it is to have this conversation with your financial advisor. People often make these decisions without all the information, and they end up losing out on income over time.

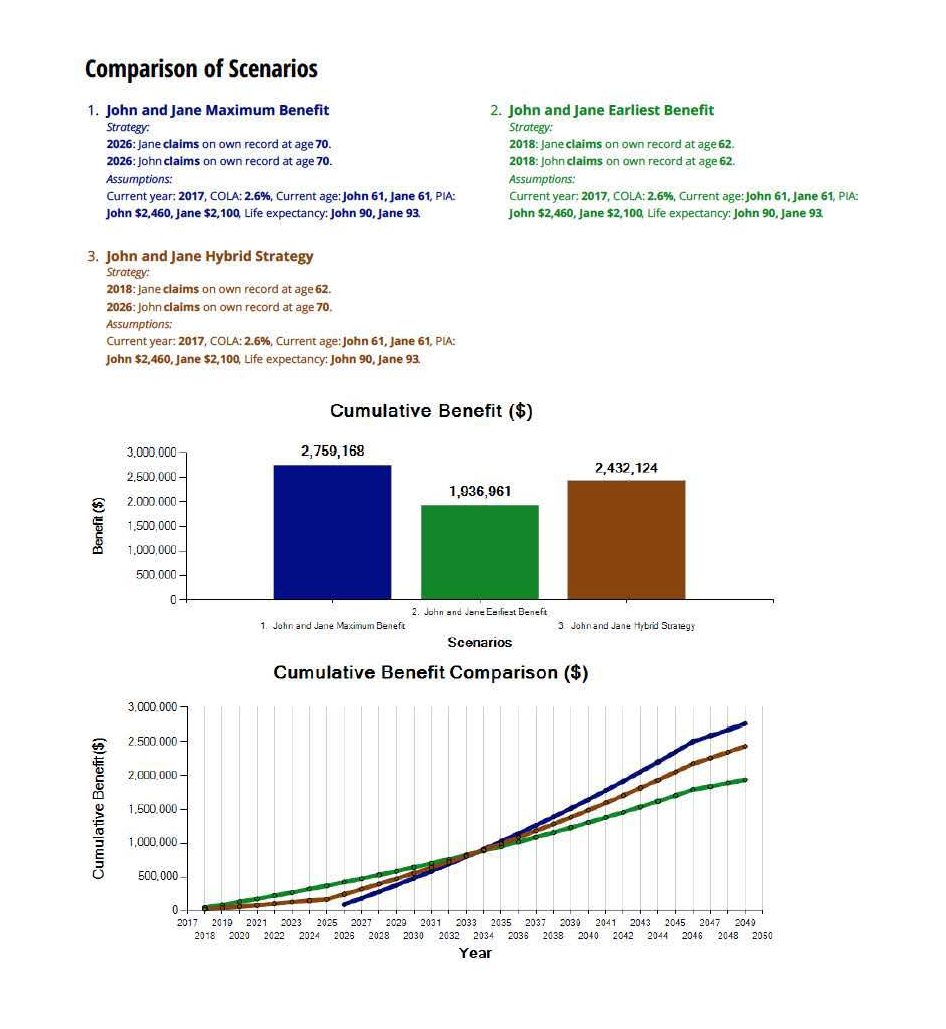

To help in making these decisions with our clients, we use different calculators to determine the best time for you (and your spouse) to claim your Social Security benefits. Here is an example what an analysis would look like:

We are able to look at the factors that are important to you, and run multiple scenarios so you can make an informed decision about starting your Social Security benefit that you won’t regret later.

The second most asked question we get about Social Security: Will it even be there when I retire? Currently, the Social Security trust is fully funded until 2034. At that time, the system will only be able to pay 79% of promised benefits. A number of reforms have been suggested, including raising the retirement age or raising payroll taxes on current workers. These changes will not likely affect Baby Boomers to any great degree.1

Of course, Social Security is a complicated topic that can’t be fully covered in a short blog. Be sure to talk with your financial advisor about how you can make the best decision for you and your family.

1 “The Baby Boomer’s Guide to Social Security,” Horsesmouth, LLC, 2016.

Financial Planning & Investment Advisory services offered through Beacon Wealth Consultants, Inc.