By Dennis Gillard, CPA

The 10-40% of taxes you pay to the government on your earned income is called your “ordinary” tax rate.

The opposite of ordinary is special, right? That’s what capital gains rates are, special rates for special income. There are two types of income that get this special treatment, Qualified Dividends and Long-term Capital Gains.

In a blog earlier this year we defined dividends (How does my account grow?) A Qualified Dividend is simply a dividend paid by a company that has been held for a specific sixty day period.

A long-term capital gain occurs when an appreciated capital asset (like a stock) is sold after being held for longer than one year. Only the appreciation (gain) is taxed, hence “capital gains tax.”

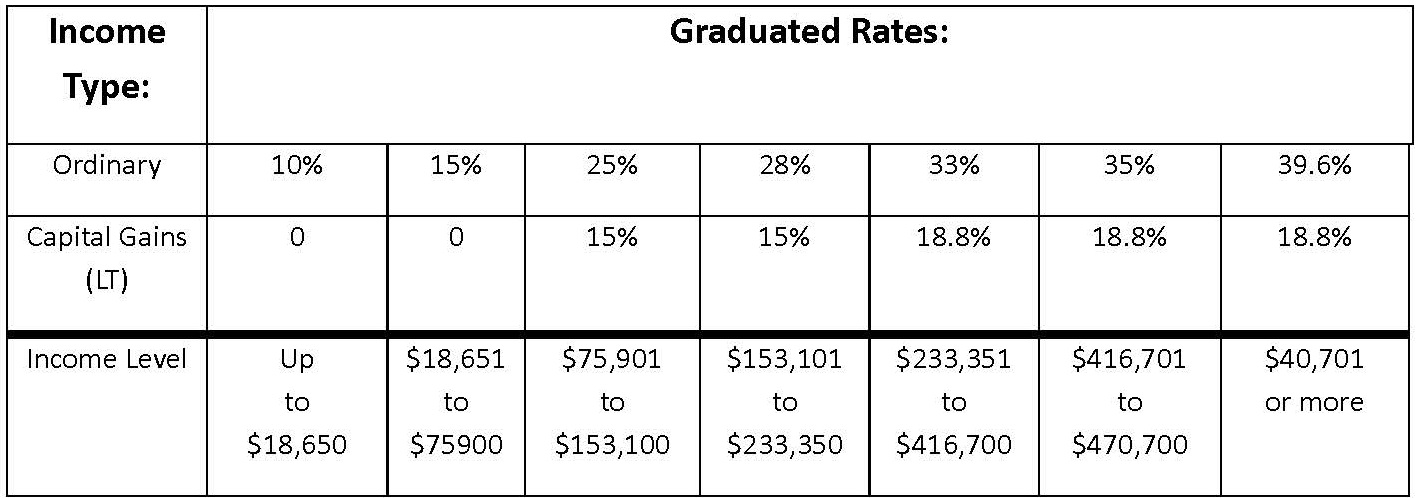

Breaking down the differences

So, what is so special about this tax rate? Like most tax concepts, it’s difficult to explain both simply and accurately at the same time, but the following table should help you get the idea. To determine your capital gains rate, you must first determine your ordinary tax rates. That is, the rates that apply to all other income.

Tax Rate Chart:

To help better understand the significance this makes consider the following hypothetical tax scenarios:

A) The Ables, a married couple, have $96,000 of gross income made up entirely of interest or other forms of ordinary income for 2016. After subtracting a standard deduction and two personal exemptions their taxable income is $75,300. Using a combination of 10% and 15% ordinary rates their income tax is $10,374.

B) The Betters, a married couple, have $96,000 of gross income made up entirely of qualified dividends and/or capital gains. After subtracting the same standard deduction and personal exemptions their taxable income is the same $75,300. HOWEVER, the capital gains rate is ZERO for anyone whose rate would “ordinarily” be 10% or 15% thus, the income tax for the Betters is $ZERO.

So, the impact of this special rate for special income can be significant. I encourage you to consider including ways of shifting from ordinary income to capital gains income in your wealth building strategies.

Short Term and Long Term Capital Gains

One such strategy is to know what you are selling. Ordinary tax rates apply to short-term capital gains. That is, you have owned the asset one year or less. In the above examples, assume the Ables’ ordinary income was from a short-term capital gain. The tax consequences would be identical to above. But, if the Ables could have held out long enough to reach the year and a day mark, they would have enjoyed the same benefits as the Betters. Sound far-fetched? Not so. I have a realtor friend who made a very shrewd purchase of real estate and sold it exactly one year later at a handsome profit. I encouraged him to delay closing by one day so as to move from short-term to long-term capital gain. The buyer would not reschedule. It was very costly for my friend.

A professional advisor can help you avoid costly mistakes

As stated above, capital gains are a very complex subject with many nuances. The more significant the money involved the more I encourage you to seek professional guidance with this area of your planning. For specific guidance, please contact us at (540) 345-3891.

Contact us for a free portfolio review:

Financial Planning & Investment Advisory services offered through Beacon Wealth Consultants, Inc.