What is Sequence of Returns Risk?

There are a number of risks when it comes to investing for retirement. Are you saving enough? Do you have enough time for your investments to experience compounding growth? Will market volatility adversely impact your portfolio? Will you outlive your money?

Investors are aware of these risks and work with advisors to develop financial plans that mitigate them. One risk that investors may not be aware of is sequence of returns risk.

Investors understand that investment returns rise and fall over the years. Sequence of returns risk is the risk associated with the order in which the returns occur. Specifically, the risk is greatest when investment returns decline early in retirement at the same time that the retiree begins taking withdrawals.

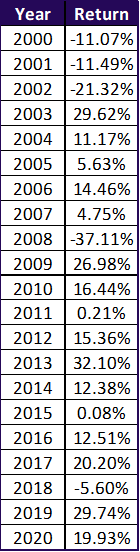

Let’s look at a hypothetical example to help illustrate the problem. For our example, we’ll use the historical returns from the Wilshire 5000 index from 2000 to 2020[1].

In the scenarios below, Ingrid Investor begins retirement with a $1,000,000 portfolio. She wants to withdraw $50,000 at the end of each year. We’ll illustrate a 21 year period using the returns from the Wilshire 5000 index above.

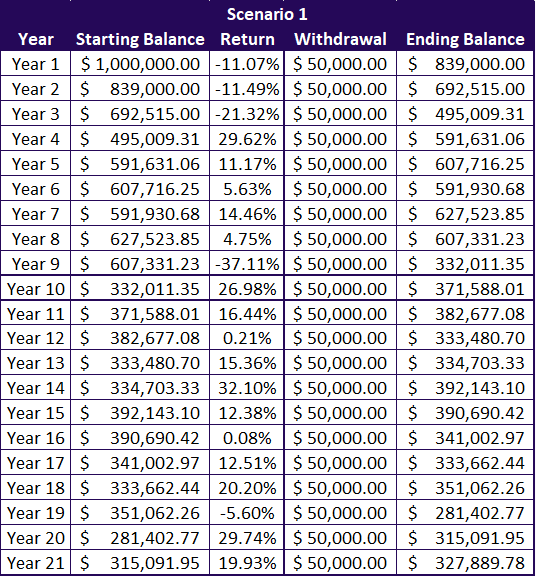

Scenario 1

The first scenario shows Ingrid’s returns in retirement begin with three years of negative returns, reducing her portfolio. However, the returns generally improve over the years with only 2 additional years of negative returns. At the end of the period she has a portfolio balance of $327,889.78.

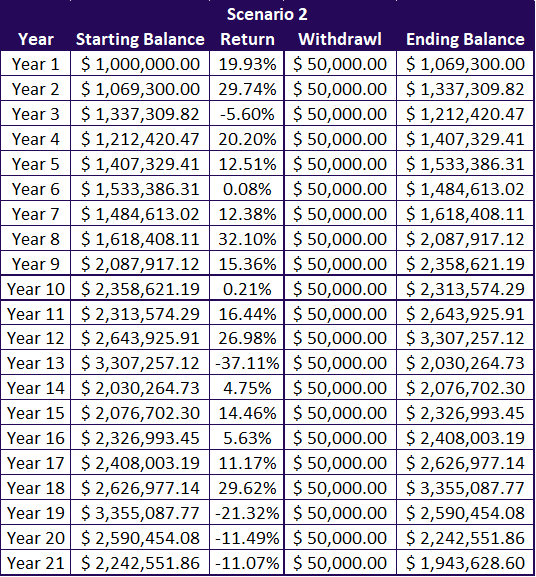

Scenario 2

In the second scenario, we have the exact same returns but occurring in inverse order. So the returns in retirement start out well and remain generally positive except for the 5 years of negative returns. The last 3 years of the period are all negative returns and Ingrid finishes out the period with a portfolio balance of $1,943,628.60.

The difference between the ending balances is a whopping $1,615,738.82! The same returns, same withdrawals, the only difference is the order in which the returns occurred.

Hopefully this example helps illustrate the damaging effect that a period of negative returns early in retirement, coupled with withdrawals, can have on a retirement portfolio. In fact, in the first scenario, Ingrid may need to rethink her whole retirement plan. Depending on how long she lives she may now be in danger of running out of money. She may need to drastically alter her withdrawal strategy and standard of living to account for the losses.

One of the most frustrating aspects of sequence of returns risk is that the order and magnitude of the future returns is unknown. This is one of the frustrating truths of investing! With the return of normal market volatility, retirees or those nearing retirement should be thinking about sequence of returns risk and how to mitigate it in the event of market declines early in their retirement.

Common strategies to mitigate sequence of returns risk

Advisors and investors employ several different strategies in an effort to guard against sequence of returns risk. Which scenario is best really depends on each investor’s individual situation and goals and so should be planned out with the help of a financial advisor. Let’s look at a few types of strategy.

Good portfolio management

One of the best initial defenses is having good portfolio construction and management. Having a portfolio that is diversified across numerous assets classes that is rebalanced regularly is foundational to sound investing and mitigating a number of risks.

Lifestyle changes

If a period of market declines kicks off your retirement, sometimes it makes the most sense to simply keep working or to return to workforce so that you are not reliant on portfolio income to meet your expenses. Another option would be to tighten your belt and reduce expenses as much as possible. These are not popular options, but they may make the most sense in a retiree’s situation.

The obvious benefit of this approach is that you do not take any withdrawals from your portfolio, allowing the full balance to increase with better returns. One possible downside is that some retirees, for health or other reasons, are not able to keep working.

Systematic withdrawal strategy

The systematic withdrawal approach is a common strategy used by investors. It is often known as the “4% rule” based on research in the 1990s by William Bengen. Bengen’s research used a 50/50 stock/bond portfolio and historical data to argue that using a 4% withdrawal rate, adjusted for inflation, would enable a portfolio to last for 30 or more years.[2]

This rule of thumb is popular because it is relatively easy to calculate and employ. Possible disadvantages include that 4% does not represent a lot of income for many investors and that investors may end retirement with more money left over than intended. Some researchers wonder whether a range of withdrawal rates might be more appropriate given differences in investor risk tolerance and increased longevity, lower market returns, and higher inflation.[3]

Adjusted withdrawal strategy

A related strategy that has emerged is adjusting withdrawals based on market returns and need. More could be withdrawn in years with good market returns and lower amounts taken in years with declining returns. This is perhaps a more precise way of taking withdrawals, but one possible difficulty is making continual lifestyle adjustments, particularly if the need arises to cut back on portfolio withdrawals and spending.

Bucket strategy

Another common strategy is the income “bucket” strategy. Under this approach, the portfolio is divided in buckets of money to be used at different time intervals in retirement. Investors might have a bucket of cash or money market instruments to spend down in the early years of retirement that is more stable and less affected by sequence of returns risk. Then there are one or more buckets of diversified investments to use later down the road, which have the benefit of time to weather volatility and hopefully guard against inflation and longevity risk.

One reason this approach is popular is that it is easy for investors to understand the concept however one possible difficulty is maintaining and managing the different buckets.

Income floor strategy

Another approach is to create a stream of income to act as a floor for expenses, often to cover basic living expenses. This income floor could be constructed by using part of the portfolio to create a bond ladder or purchase an annuity and then investing the rest of the portfolio in diversified investments that can hopefully grow over time and from which additional withdrawals could be taken.

This approach may be out of reach for many Americans who have simply not saved enough to create the floor and then have money left over to create the portfolio.

Which strategy is best?

You can see that these different approaches each have pros and cons, so where does that leave investors concerned about sequence of returns risk? The selection of strategy is best done as part of a comprehensive financial plan developed with the help of a financial advisor. The right approach for you will depend on your unique situation, your goals, your risk tolerance, and other factors. There is no “one-size-fits-all” solution.

If you’re concerned about guarding your retirement against sequence of returns risk, you don’t need to figure it out alone. Give us a call! We have a team of experienced Christian financial advisors who can help you understand your options and develop a plan that is appropriate to your situation and goals.

Disclosure: This information is for educational purposes only. The performance examples presented are examples only and are not representative of the performance of any actual customer account. Actual returns will vary. If you invest you may lose some or all of your money.

[1] The FT Wilshire 5000 Index is a broad-based market capitalization weighted index that aims to capture 100% of the US investible market. The FT Wilshire 5000 Index Series comprises of the large, mid, small, and micro capitalization segments of the US equity market.

[2] https://www.retailinvestor.org/pdf/Bengen1.pdf

[3] https://www.financialplanningassociation.org/article/journal/MAR12-spending-flexibility-and-safe-withdrawal-rates