By: Chad Hamilton, CFP

Traditional economics assumes we act rationally when making financial decisions, and we always act in alignment with our own economic self-interest. According to economic theory, we think as clearly as Albert Einstein and exercise the willpower of Mahatma Gandhi.

In reality, however, we are often guided much more by emotions than by rational decision-making. An example of emotion over logic is the challenge of losing weight. As many of us have experienced, it’s often much more difficult than simply applying the mathematics of calories in versus calories out.

Behavioral finance is a relatively new field within financial planning that applies knowledge about human behavior to the investment world. It provides a better framework for understanding how we make financial decisions and our reasons for doing so.

Behavioral finance has identified several types of investment errors that are both irrational and predictable. Here are three of the most common errors along with tips for avoiding them.

1) Recency Bias:

We tend to overemphasize recent events when making decisions. For example, people tend to like stocks after the market has had a strong upward trend and dislike them after a downturn. This often leads to “buying high and selling low,” which is contrary to the mantra for successful investing.

Given this tendency, it is best to avoid overly scrutinizing your investment portfolio or watching the news headlines too closely. If you look at your portfolio daily, you will see a loss 46.7% of the time. If, instead, you look at it yearly, you only see losses 27.6% of the time.

Evidence shows that the more frequently we look at our portfolios, the more likely we are to trade. The more we trade, the more likely we are to destroy value.

2) Loss Aversion:

Most of us tend to strongly prefer avoiding losses over acquiring gains. Studies have shown losses to be twice as psychologically powerful as gains.

In order to overcome loss aversion, you must first understand that risk does not equal market volatility. Risk is the chance that you will not achieve your goals. You can eliminate volatility and avoid losses by putting all of your money in cash, but that is actually a very risky strategy. Earning a 0% return in a bank account means you will not be able to keep up with inflation and virtually guarantees that you will outlive your assets.

The reason that stocks outperform most other types of investments is because they are scary! The reason you receive a premium for investing in stocks as compared to other assets is that you can lose money. If stock market investing meant a smooth upward trajectory, all money would be in stocks and there would no longer be an excess financial return for doing so.

3) Herd Behavior:

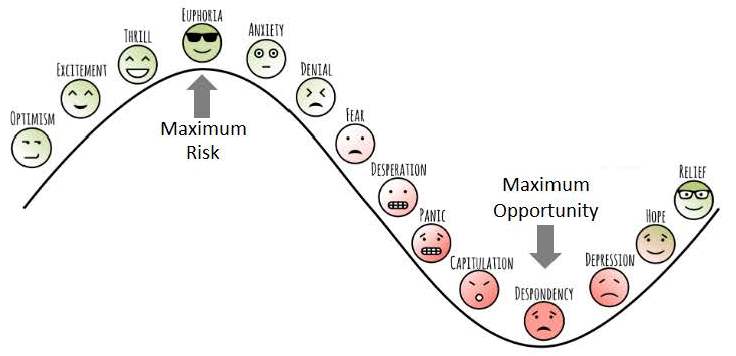

We have a natural tendency to mimic the actions of a larger group. We typically prefer being wrong as part of a collective to being wrong by ourselves. This poses a real challenge for investing because the best investors are contrarian.

Warren Buffet has said of his investment philosophy, “We simply attempt to be fearful when others are greedy and to be greedy only when others are fearful.”He is, of course, describing the exact opposite of herd behavior. You can see why this is true by considering the emotional cycle of investing as depicted in the following chart.

When the news reports are reporting the worst point decline in history and that worse news is ahead, that is actually a better time to invest than when are the headlines are rosy and the market is reaching new highs.

The Need for Context

Given all of this, there can still be a tendency to then want to guess where we are in a particular market cycle, but that is only ever apparent in hindsight. Instead, the single most important thing you can do is have a plan.

Without a comprehensive financial plan, there is a lack of context to help you understand the consequences of market volatility. You are likely to be more susceptible to reactive, emotional decision-making when it is unclear how a loss in your portfolio value will impact your long-term financial situation.

Having a plan, on the other hand, provides a more meaningful backdrop to market volatility. With a plan, you know how changes in your account value may alter your ability to reach your goals. You may not be able to control fluctuations in the market, but you can make adjustments to your cash flow, goals or asset allocation that can positively impact your financial situation.

Let’s make a plan! Give us a call today to get started or update yours at (540) 345-3891.

Financial Planning & Investment Advisory services offered through Beacon Wealth Consultants, Inc.