How did the stock market deliver such strong returns despite inflation, geopolitical conflict, tariff uncertainty, and persistent interest rate concerns?

In this Quarterly Market Commentary, Beacon Wealth’s Chief Investment Officer, Hillary Sunderland, joins Director of Financial Planning, Jake Preston, to break down what happened during the second quarter of 2026 and what investors should be watching in the months ahead.

Topics covered include:

- Why U.S. stocks reached new highs despite investor anxiety

- The expanding impact of artificial intelligence (AI) on the economy and financial markets

- Inflation, oil prices, tariffs, and what they could mean for future interest rates

- Why bonds lagged stocks and what may be ahead for fixed income investors

- The importance of diversification beyond the “Magnificent Seven”

- Why investors should not wait for a market pullback before investing

- Market outlook for the second half of 2026

Whether you’re a long-term investor, nearing retirement, or simply trying to understand today’s market environment, this discussion provides timely perspective on the forces shaping the economy and investment markets.

(Full transcript below)

Transcript

Jake Preston

Well, hello, we are excited to welcome you to another market update. My name’s Jake Preston, I am the Director of Financial Planning here at Beacon Wealth, and I’m joined by Hillary Sunderland, our Chief Investment Officer. Hillary, it’s great to be with you again.

Hillary Sunderland

Great to be with you, Jake. Thank you.

Jake Preston

Well, it feels like investors have spent most of the year worrying about items like inflation, things that are happening in the Middle East, tariffs and interest rates, and yet, markets continue to be very resilient and move higher. So, can you give us an overview of what happened during the second quarter?

Hillary Sunderland

Yeah, sure. So during the quarter, the headlines really suggested that investors should have a lot of caution, but the fundamentals told a very different story. What was particularly impressive in the second quarter is really the number of challenges the markets absorbed. So we’ve navigated a war in the Middle East, sticky inflation, tariff uncertainty, and a lot of shifting expectations around the direction of interest rates.

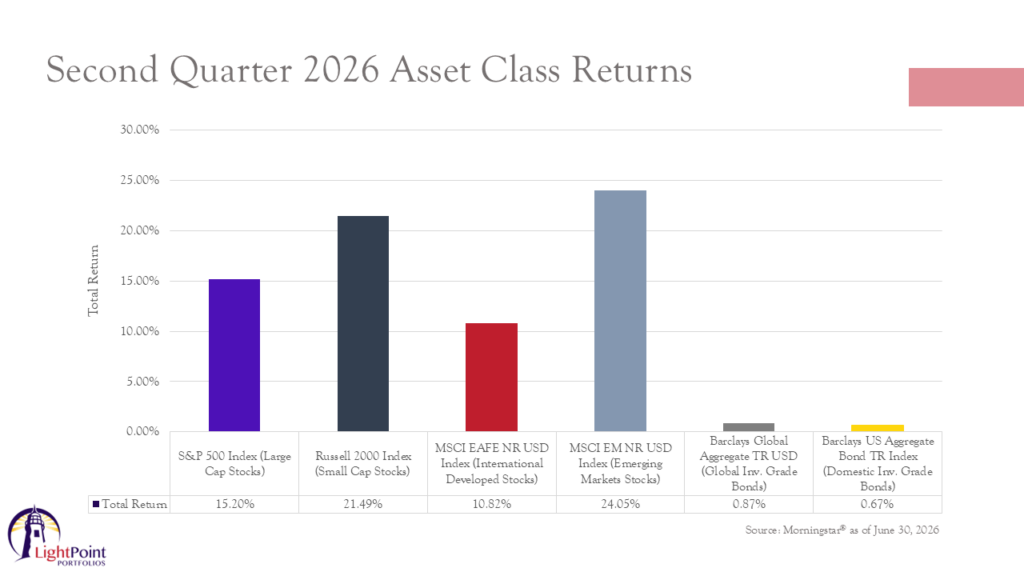

But at the same time, corporate earnings remain very strong and the economy has continued to grow. And with that backdrop, we had a very impressive quarter in terms of returns. As shown on this chart, the S&P 500 advanced just over 15%. Small cap stocks were up about 21 and a half percent. International developed stocks returned just under 11%. And the star of the quarter was emerging markets. Those are countries like China and Taiwan. They had returns of just over 24%.

So overall, very impressive returns for risk assets over the last 3 months, and these are numbers that you would maybe expect to get over a year, but it’s quite, mind-boggling to see it happen in just 3 months.

Jake Preston

Yeah, that’s for sure. And so you’re saying that it wasn’t just a handful of technology companies carrying the market like we’ve seen in the past?

Hillary Sunderland

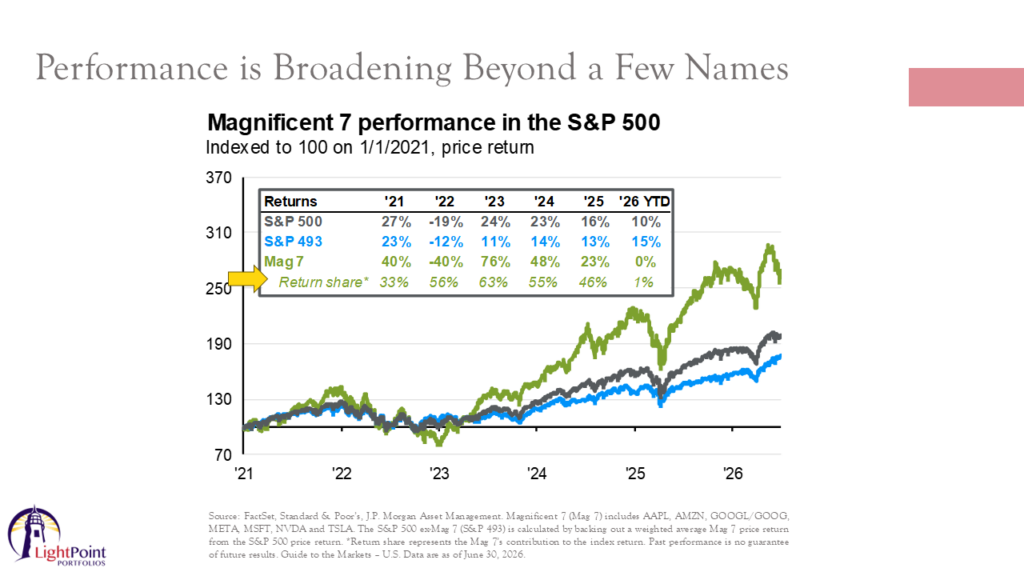

Yeah. No, not this time. One of the healthier developments this year is that market leadership has started to broaden beyond the Magnificent Seven. So those are the large technology companies that drove a significant share of the returns in recent years.

As shown on this chart from 2022 through 2024, more than half of the S&P 500’s return came from just seven companies.

In 2025, that share fell to just below 50%. And then this year, the rest of the market is actually outpacing the Magnificent Seven, because we’ve seen that AI theme, that artificial intelligence theme, really expand into more sectors which is something that we did forecast would occur. We talked about this on a call late last year. So for clients, that matters because broader participation in the market advance is very constructive for investors.

Jake Preston

Alright, so that really seems to further emphasize the importance of being well-diversified across every sector of the market.

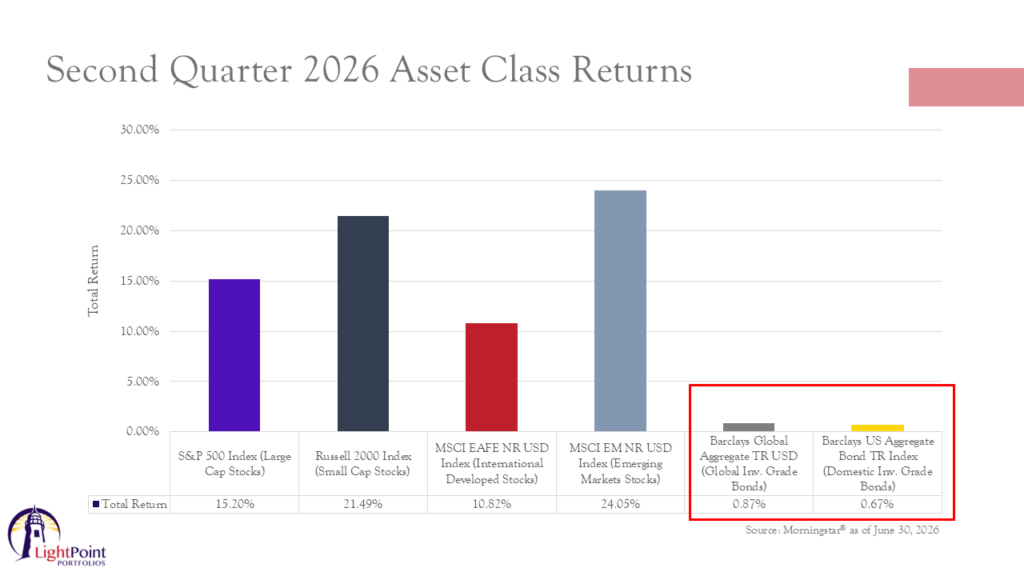

And so it’s easy to tell that stocks had a terrific first half of the year, but I noticed on the asset class returns chart that you showed a bit ago that bonds did not really participate in that rally. And so for investors that find themselves in more conservative or balanced portfolios.

What can you tell us about what happened in fixed income, and should these investors be concerned going forward?

Hillary Sunderland

Yeah, you’re right, Jake. So fixed income was one of the more disappointing areas of the market. As shown on this chart, core investment grade bonds returned less than 1% for the quarter. And that’s largely because interest rates moved higher.

So you may recall that coming into the year, the expectation was that the Fed would be cutting rates by now. But instead, inflation has remained stubbornly elevated.

That’s mostly due to an increase in energy prices due to the war in the Middle East.

That repricing of energy prices have really pushed bond yields higher across much of the yield curve, and that’s created headwinds for bond prices. Now, that said, we may be entering a more constructive environment for fixed income. If inflation begins to ease as energy prices decline and tariff pressures continue to moderate, upward pressure on interest rates could, begin to subside.

So fixed income continues to have very attractive starting yields, and a potentially more stable interest rate environment could create better opportunities in the second half of 2026.

So I would say this is not the time for investors to give up on fixed income.

Jake Preston

That’s very helpful and clarifying for sure.

So let’s shift back into talking about stocks and in particular about what is powering stocks. So we know that AI, artificial intelligence is everywhere. It seems like we can’t go an hour of our day without hearing something about AI. And so with regards to the markets, is artificial intelligence still the biggest market story?

Hillary Sunderland

Yeah, without question. So, AI really remains the dominant investment theme, but what’s really changing is where that opportunity is showing up. So, early on, over the last couple of years, investors focused primarily on technology platforms and semiconductor companies.

Today we’re seeing the AI theme investments spread much more broadly into areas like data centers and power generation, infrastructure, cooling systems.

We’re seeing very wide adoption across different sectors of the economy. And what’s important is that the story does continue to be supported by fundamentals, so analysts expect roughly 24% earnings growth for the US companies this year. That’s one of the strongest growth rates we’ve seen in decades.

So if those forecasts hold, it would mark three consecutive years of double digit earnings growth for the first time in about 20 years. So I would say even though this market is has been on a tear lately, I don’t think this is a speculative story like it was in the early 2000s when we had the tech bubble because unlike some of the previous technology cycles we’ve been through, investors are actually seeing substantial revenue growth and real business investment supporting this theme. There are earnings behind the numbers that we’re getting.

Jake Preston

That’s very, very interesting. I think it sounds like artificial intelligence is certainly here to stay. Well, a couple of items that you referred to earlier that I want to revisit are inflation and interest rates. These remain front and center for many investors. What can you tell us about what has changed recently?

Hillary Sunderland

Sure. Well, inflation does remain elevated, as I’m sure most of our clients have noticed when they go to the store.

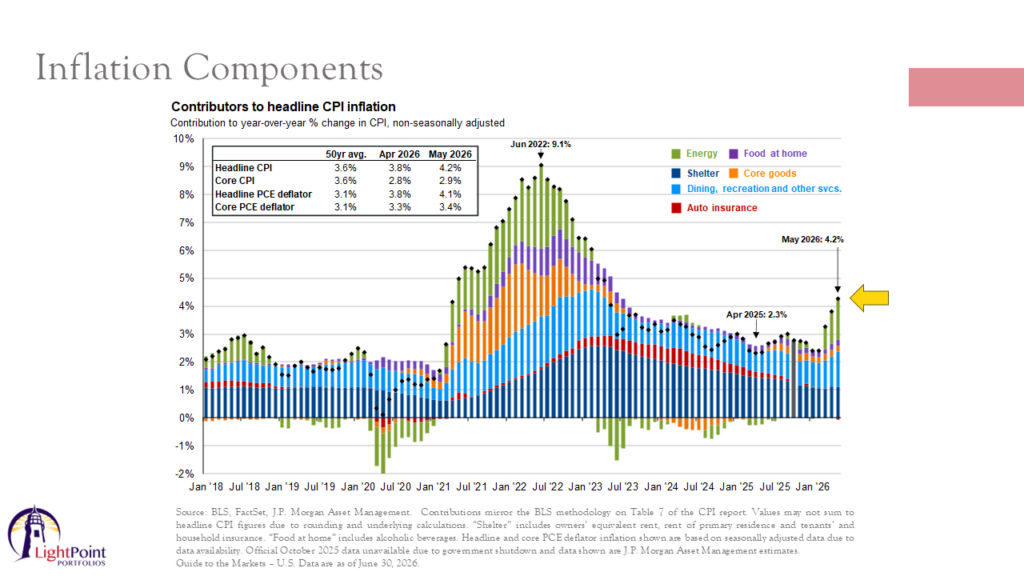

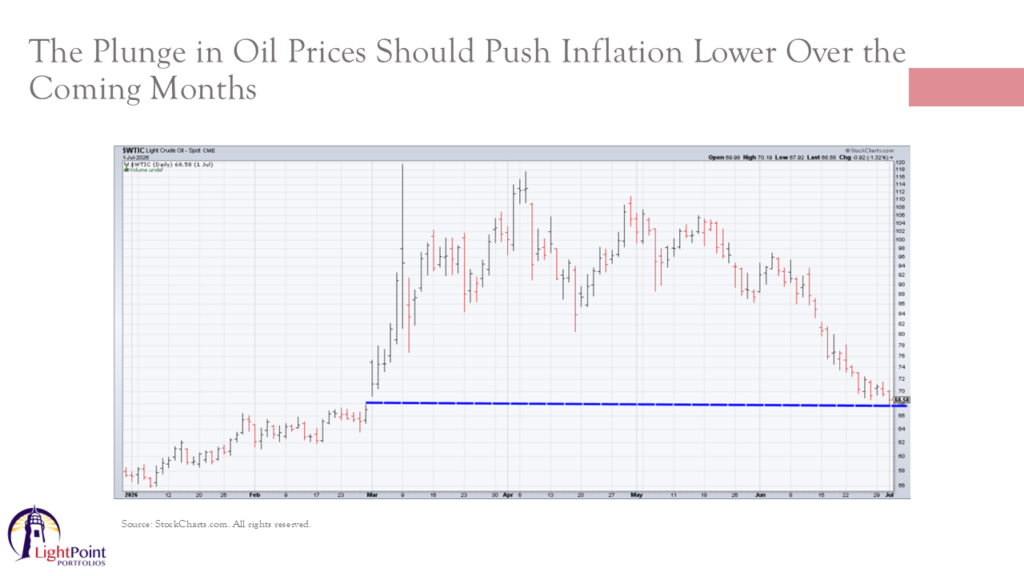

As shown on this chart, headline inflation reached, 4.2% year over year in May. The nice thing about this chart in particular is that it’s color coded. So it shows the different components of inflation. And you can see here that a lot of the spike in inflation over the last few months is green meaning it came from the energy sector due to the war in the Middle East.

However, there are reasons for some cautious optimism moving ahead. So the biggest development is really energy prices. So last quarter in this call, we talked a lot about how energy prices could reverse very quickly once there was de-escalation in the war. And that is what has transpired over the last few weeks. What you can see from this chart is that crude oil has fallen to below $70 per barrel which is back to where it was at the beginning of March.

We were above $100 a barrel when we talked at the end of the quarter, but now we’re back below 70 just three months later.

Gasoline prices have also declined throughout June, and those declines should really help ease inflationary pressures over the coming months.

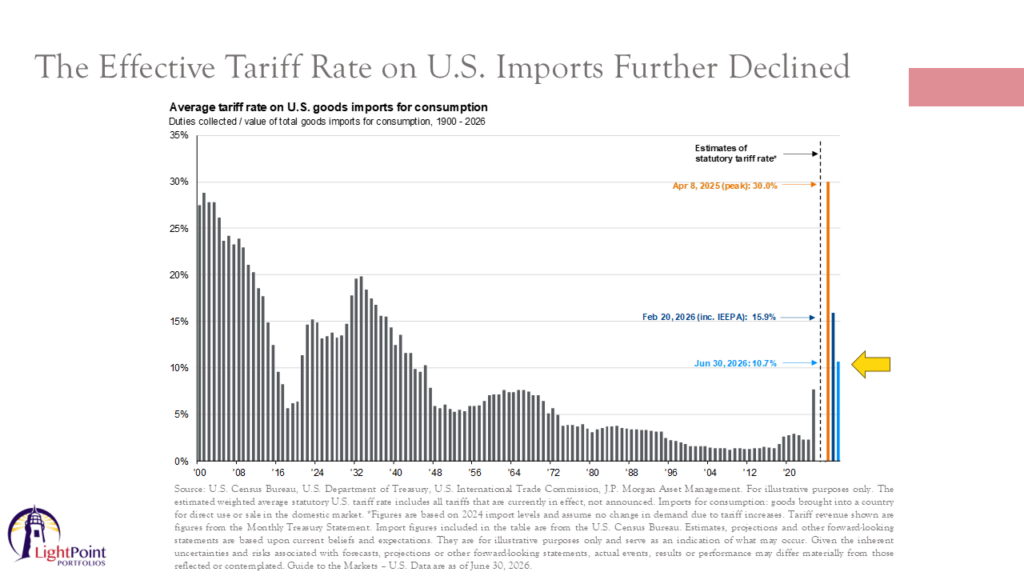

Additionally, the effective tariff rate has declined even further since last quarter, as shown here.

Court rulings and tariff refunds have lowered effective tariff collections, so the effective tariff rate has also fallen substantially from levels seen late last year. And there are affordability concerns broadly in the U.S, and that’s important ahead of the midterm election cycle that’s approaching. So, I do believe there’s less political appetite for additional tariffs to come on board. Taken together, I think both the decline in energy prices as well as the tariff rates easing over time should then, temper inflation going forward.

Jake Preston

So given your outlook on inflation, what should investors expect in terms of interest rates going forward?

Hillary Sunderland

Well, overall, the Fed still faces a difficult balancing act between inflation that’s still elevated, you know, their target’s about 2%, we’re running above 4 right now, and signs that some inflation pressures may be easing. So, over the quarter, the market priced in another interest rate hike.

But my take on it is that the Fed could also just choose to keep rates on hold for a while, outside of some shock to the markets. I don’t see a rate cut this year, but, the Fed may just stay where they are until some of that inflation has some time to roll off the numbers.

Jake Preston

Very interesting. Yeah, it’ll be fascinating to see what happens with the new Federal Reserve Chair as well, to see the decisions that might come down the pike. Well, one more surprising thing this year is that many investors still seem nervous, even with markets near record highs, and so my question is, if markets are doing so well, why does it feel like investors are still so worried?

Hillary Sunderland

Oh, that’s a great question, Jake. So you’re right. Even though the market has performed very well this year, many investors are uneasy about what’s ahead. One way we look at that is to look at something called investor sentiment. And we can do that through a survey from the American Association of Individual Investors.

So they ask everyday investors whether they think the market will move higher or lower over the next six months.

And right now, almost half of investors surveyed expect stocks to decline, and only 30% of investors expect them to rise. What’s even more startling to me is we’re halfway through 2026, and there were only 9 weeks this year where more investors felt optimistic than pessimistic about the returns.

And those are very pessimistic statistics, and historically speaking, it’s highly unusual to see such a big disconnect between how investors are feeling versus what the markets are actually doing. It really suggests to me, Jake, that investors are still focused on different risks such as inflation and interest rates and geopolitics, even as the earnings and economic growth numbers that are coming in continue to support the market.

You can also see investors being nervous just by looking at how much cash is sitting on the sidelines. So assets and money market funds reached a record $7.9 trillion during this quarter. That is a lot of dry powder to potentially come off the sidelines and back into the markets when investors get more comfortable. Now, I wouldn’t expect all of that cash to move back into the market, but even a modest allocation of that cash back into the market could provide additional support for stocks over time.

And then just one more note on that is, you know, it’s actually good when many investors remain cautious despite the market going up so much, because historically, markets perform well when sentiment is depressed, which is what we’re seeing right now.

Jake Preston

Oh, that’s very interesting. Well, that does bring up another question, and that is that oftentimes we will hear that, okay, the market is at an all time high or it’s near record highs, have I missed my opportunity? And then flowing from that, should I wait for a pullback before investing? And so if a client asked you that, or an investor asked you that, how would you respond to that question?

Hillary Sunderland

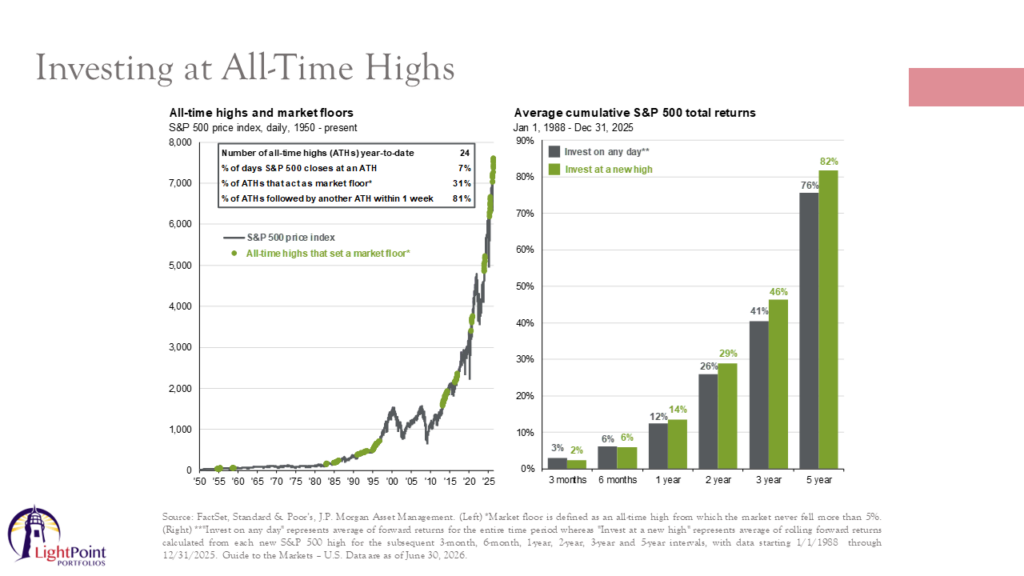

Yeah, it’s a very understandable concern, but history suggests investors need to be careful about letting record highs keep them on the sidelines. All time highs are a normal feature of a healthy bull market. We’ve already seen dozens of new highs this year, and that’s often what happens when corporate earnings continue to grow as robustly as they have.

I thought this chart would be fascinating to show to our clients. So the left hand side of this chart shows that about 30% of new highs have effectively become a market floor, meaning the market doesn’t go back beneath that level.

And then if you look at the right hand side of the chart, the green bars represent the average forward returns when investing in the S&P 500 at a new high, while the gray bars show the average returns from investing on any random day. And surprisingly, since 1988, investors have actually done better by buying at new highs than by buying, at any other given day in the markets. The other thing that’s interesting this year, and I’ve heard this a lot, is, you know, clients or, you know, investors may be concerned that, oh, things must be more expensive now because the market has gone up. But that’s actually not what’s happened.

Valuations in this S&P 500 particularly have actually become cheaper as the year has gone on because earnings growth has been so strong. But the price of the stock has not gone up as much. So if you look today as the end of the quarter we look at something called the price-to-earnings ratio. The forward price-to-earnings ratio in the S&P 500 has declined from roughly 22.1 times earnings at the start of the year to 21 today. So, in other words, while stock prices have moved higher, the earnings supported those supporting those prices have moved even faster, which helps explain why the new highs don’t necessarily mean that the market has become overly expensive for investors.

Jake Preston

That’s very helpful, and it reminds me of the quote that we repeat around here quite a bit, and that is that investing success is not determined by trying to time the markets, but by time in the market, and so obviously, you know, past performance is never a guarantee of future results, but historically, it shows that the quicker that you can get your cash to work invested in great companies that are doing really good things in the world, then that usually works out well for investors.

And so you have looked back at the previous quarter and even year to date and given us a lot of helpful things to think about, some really keen analysis. And so looking ahead, how should investors be thinking about their portfolios in the second half of the year?

Hillary Sunderland

Well, I think investors should be cautiously optimistic. So risk assets delivered an exceptionally strong first half.

And if tensions in the Middle East continue to de-escalate, that could help ease inflationary pressures and reduce those upward pressures on interest rates. At the same time, it would not be surprising to see markets consolidate as we move higher.

As we move closer to the midterm election cycle, investors will continue to weigh inflation, Federal Reserve policy, and the strength of economic growth. So even so, the broader foundation remains constructive. Corporate earnings are growing, the economy has been resilient.

We continue to see opportunities across both stocks and bonds. I think really the key takeaway from this year is that markets don’t wait for uncertainty to disappear. Long-term success comes from maintaining, really, a disciplined investment plan, staying diversified, and remaining focused on your goals, even when the headlines can feel a little unsettling.

Jake Preston

I think it also, you know, it underscores the importance of having a trusted advisor who can help you when the headlines seem very pessimistic and negative. And I know that I speak for the rest of our advisory team when saying that we are very grateful for Hillary and her team and all the work that they do on a daily basis to help us stay ahead in terms of our investments and stay on top of what’s happening and making good decisions.

So, Hillary, thank you so much for joining us again, and if you have questions, those that are watching, you can contact your advisor, or feel free to reach out to our home office. We want to thank you for being part of this market update.

Hillary Sunderland

Thanks, Jake.

Sign up for our newsletter!

Get news, market commentaries, videos, and faith-based investing articles from Beacon Wealth Consultants in your inbox.