If you’ve ever read the financial news or watched a TV segment that includes a market update, you’ve likely been bombarded with terminology that you may not be able to define but that could make a BIG difference in your emotional reaction to market events. For example, what is the difference between a pullback, a correction, and a bear market? If a headline flashes that the Dow Jones Industrial Average shed 500 points, is that a terrible event for your investment account or just a natural blip in the markets?

Market losses can be unnerving, but part of becoming an astute investor is not only knowing the terminology surrounding market losses but also having a plan that is informed by an historic perspective in order to be guarded emotionally when volatility comes. Let’s look at some common questions we receive from our clients:

Should I be concerned if I hear on the news that the Dow Jones Industrial Average (DJIA) shed 500 points? While the news media seems to have an infatuation with multiples of one hundred or one thousand, a drop of 500 points needs to be put into its proper context. If the DJIA is trading around 25,000 (which it is as of the time of this writing) a drop of 500 points is only a loss of about 2%. While this may signal a sudden increase in market volatility, this is no cause for panic. In the depths of the last bear market, the DJIA was trading around 7,000. At those levels, a drop of 500 points is equivalent to a loss of 7.1% in one day. This would be more of a cause for worry as a sharp drop in percentage terms is much more relevant to an investor and can signal a more severe geopolitical, economic, or market upheaval is at hand.

While the news media seems to have an infatuation with multiples of one hundred or one thousand, a drop of 500 points needs to be put into its proper context. If the DJIA is trading around 25,000 (which it is as of the time of this writing) a drop of 500 points is only a loss of about 2%. While this may signal a sudden increase in market volatility, this is no cause for panic. In the depths of the last bear market, the DJIA was trading around 7,000. At those levels, a drop of 500 points is equivalent to a loss of 7.1% in one day. This would be more of a cause for worry as a sharp drop in percentage terms is much more relevant to an investor and can signal a more severe geopolitical, economic, or market upheaval is at hand.

What is a pullback?

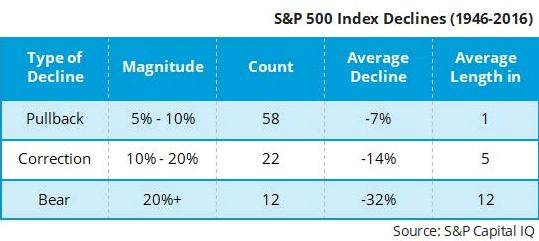

A pullback is simply defined as a drop of 5% – 10% from a recent high. Pullbacks are a natural occurrence as investors react to new information and take profits. According to S&P Capital IQ, between 1946 and 2016, 58 pullbacks occurred with an average decline of 7%. While several pullbacks can occur in a year, on average, they occur about once per year. Professional investors often welcome pullbacks as they can be the “pause that refreshes,” and they can provide the opportunity to “buy on the dip.”

The average length of a pullback is one month. Because the average length of a pullback is so short, it is a fool’s game to attempt to protect a portfolio from these losses because a bounce back can easily occur shortly after selling, and you would effectively be selling low to later buy back high. Rather than reallocate portfolios from stocks to bonds during a pullback, it is often better to add to stocks.

What is a correction?

A correction is a drop of 10% – 20% from a recent high. Corrections tend to be more emotionally unnerving than a pullback given that they are deeper in scope and can mark the start of a bear market. In terms of frequency, there have been years in which several corrections occurred, and there have been time periods where the markets have gone several years without a correction, such as 2012-2014. So, while they are not uncommon, they do vary in frequency. On average since World War II, corrections have occurred once every three years. The average decline during a correction is 14%, and the average length is five months. Corrections generally will not undermine a well-diversified portfolio given that the overall decline is relatively limited.

What is a bear market?

A bear market is a decline of at least 20% from its high. There have been 12 bear markets since World War II, and the average decline and length of a bear market varies. Nine of the 12 bear markets had market declines of 20% – 40%, while three of them had declines greater than 40%. Selloffs of this magnitude can compromise financial plans and take longer to recover from – especially if you are periodically withdrawing money from a portfolio.

How do you know when a correction will turn into a bear market or when a bear market will be unusually severe?

While all investors would like to know this ahead of time, the fact of the matter is that it is very difficult to predict the severity of any downturn in advance. One must remember that markets are NOT logical. Markets move on the whims of investors, which are guided by emotions, not necessarily based on the intrinsic value of any particular investment. However, there are general guidelines that one should consider.

The first is fundamental valuations. The further valuations are stretched, the further the market is likely to fall. Why is this? Think about the housing bubble. At its peak, a house may have been selling for $500,000, but the house was only worth $250,000. As such, the decline to get back to its fair price was 50%. However, if the house was actually worth $400,000, this required a decline of only 20% to get back to fair value.

One must remember that the stock market is a market and prices will decline until enough investors look at the price and say, “Yes, I’ll buy it here for $X”. Once you get enough buyers, (demand) the price will stabilize and the bear market will hit its bottom.

The other guideline is the economic environment. Most, but not all, bear markets have been accompanied by a recession. Historically, those bear markets with the steepest declines and the longest recovery periods have been associated with economic recessions. As such, the probability of a recession is a key data point to consider when trying to determine how low the market may go.At this juncture, we believe that the global economy is on firm footing, and the probability of a recession occurring in 2018 is low.

Overall, investors’ level of concern and willingness to reduce exposure to stocks should increase as fundamental valuations increase significantly over fair value and/or as recessionary flags wave given that the probability of a severe decline increases under both scenarios. At Beacon Wealth Consultants, we monitor the economic, fundamental, and technical environment closely and will adjust portfolio allocations as warranted. As always, please reach out to us with any questions you may have.

Hillary Sunderland, CFA

Chief Investment Officer

Financial Planning and Investment Advisory services offered through Beacon Wealth Consultants, Inc.