In our September 2022 Quarterly Economic and Market commentary, Beacon Wealth Consultants’ Chief Investment Officer Hillary Sunderland, CFA®, CKA® looks at several topics on everyone’s mind:

- What is going on in the markets and inflation? (Including some positive indicators)

- What is the cause of the latest volatility?

- Will the midterm elections affect the markets?

- What are we doing within our LightPoint Portfolios?

We hope the discussion will give you some hope and encouragement to stay focused on your long-term investing goals.

Thank you for being a valued client of ours, and please reach out to us with any questions that you may have.

Full transcript below.

Transcript

Hi, my name is Hillary Sunderland and I’m the Chief Investment Officer of Beacon Wealth and LightPoint Portfolios. This is your September 2022 market update.

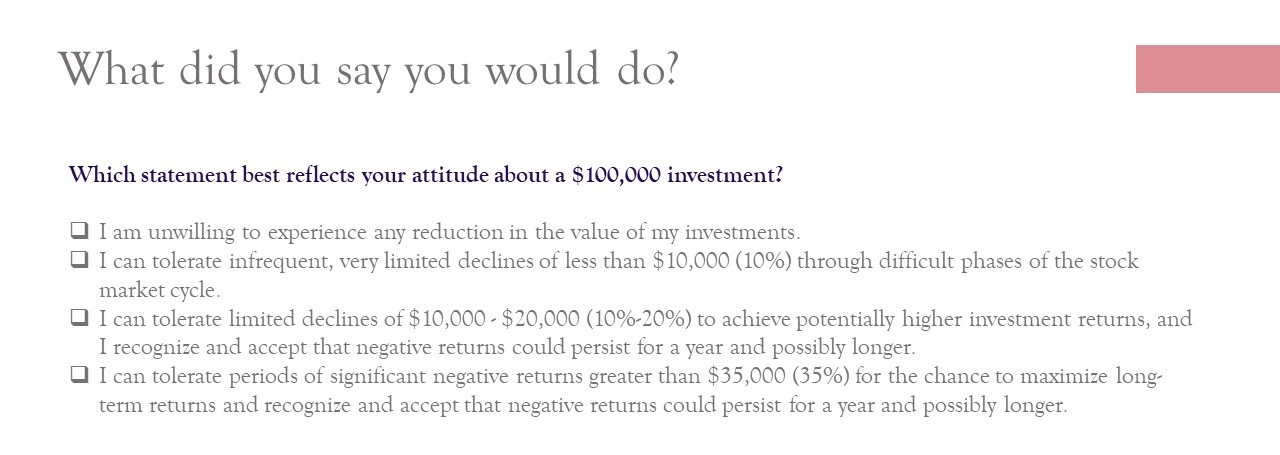

Well, do you remember when you sat down with your wealth advisor and went through a risk profiling process to assess your willingness to withstand market losses? It probably looked something like this.

And at that time you likely had a theoretical conversation about what you would do if your portfolio lost 10%, 20%, or even 40% of its value. You may have selected that you’d be okay with a 20 to 30% decline your portfolio because perhaps you thought that decline would be short lived. It was a theoretical conversation without the advantage of knowing why stocks were declining in value. Well, today you have the benefit of knowing why your portfolio’s down, but unfortunately, it’s no longer a theoretical conversation. Here’s a chart of the S&P 500 index to give you a picture of what investing in the stock market has looked like over the last 18 months, and it has been a time period that’s been difficult to stomach.

We’ve had a land war in Europe for the first time in several decades, which has caused spikes in both energy and food prices, leaving inflation elevated for longer than anticipated to combat this and also to make up for lost ground because both fiscal policy and monetary policy were too easy for far too long. Over the last decade or so, the Federal Reserve has responded with large interest rate hikes over a very short period of time, and this has increased the odds of recession by quite a bit over the last few months. As a result, both the stock and the bond markets have done their best to draw EKGs all over the charts, and it looks like the S&P 500 index will end the third quarter at about the same market levels or maybe even lower than where we ended the second quarter. And this has likely left you thinking, you know, this is not what I had in mind when I said I could withstand a decline of 20 or 30% in my portfolio.

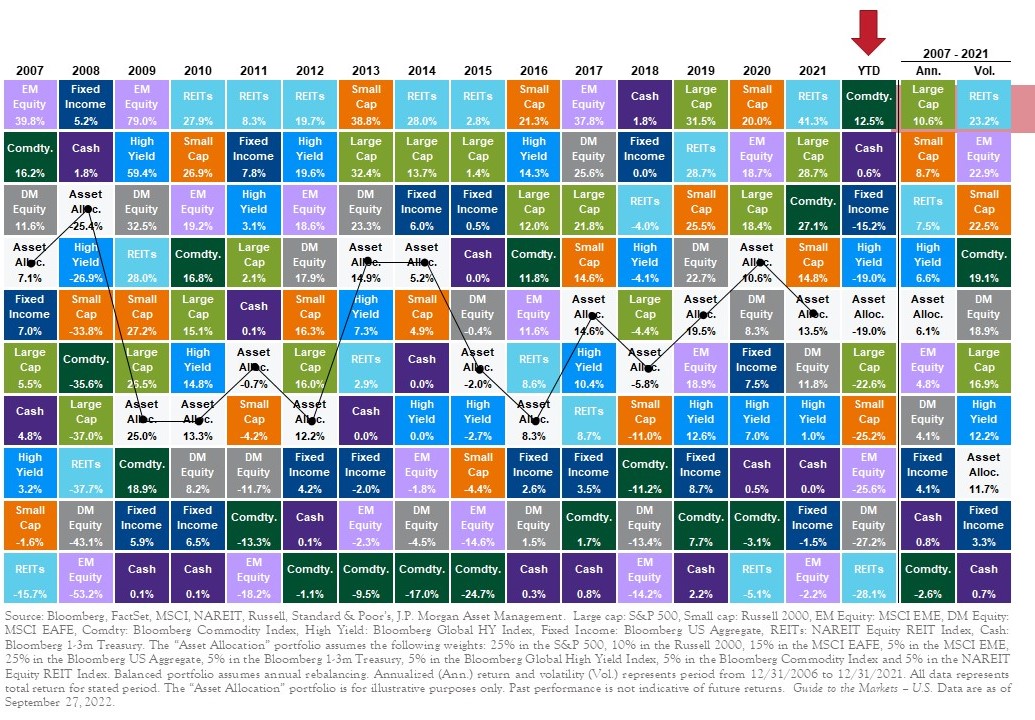

I wanted to show you this chart. This is what we call the periodic table of asset class returns.

If you go across the top, you can see the returns for each calendar year with the best performing asset class in the top row, ranked down to the worst performing asset class in the bottom row, and the arrow there is pointing to where we are year to date through September 27th, and it has been a brutal year for investors. The only major asset class that has been positive year to today is commodities with return of just over 12%, and that’s actually down quite a bit from where it was earlier this year. Next we have cash with a return of just under 1%, which would still be negative though if you were to adjust for inflation of eight to 9%.

Next we have fixed income investment grade bonds, which are down over 15%. High yield bonds down about 19%. Your typical balanced portfolio about 65% stocks, 35% bonds down 19%. Domestic stocks down anywhere from 22 to 25% and so on. So as you can see from this chart, there really hasn’t been a place to hide. So even though in the LightPoint Portfolios, we took action many, many months ago to reduce our exposure to fixed income in our portfolios and to add exposure to alternative investment such as commodities to hedge some of the risk. In a market like this where the baby’s being thrown out with the bath water, it’s very difficult to shield portfolios from these losses.

So even though in our more conservative LightPoint Portfolios, even though those are well ahead of their benchmarks year to date, I know the losses have still been difficult to stomach. And this is really where the reality of investing takes center stage.

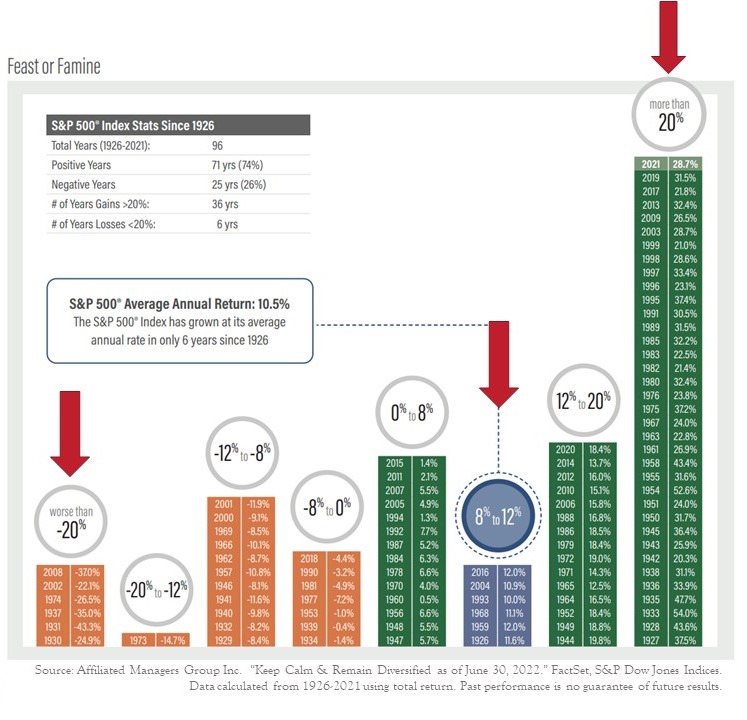

Many investors have anchored in their minds that they’re likely to earn a specific rate of return each year because what’s commonly quoted is that the S&P 500 index on average earns eight to 12% a year, which is what this chart’s showing as well.

But the key part of that sentence is that it earns that return on average. Reality is that since 1926, in the last 96 calendar years, the S&P 500 has only earned an annual return of between eight and 12% in six of 96 calendar years.

In 36 years, gains have been more than 20%, and in six years the losses or have been worse than negative 20%. So it’s actually been a very bumpy ride to get to that on average number. And it’s important to remember right now, especially that any losses you’ve incurred this year only exist on paper.

As you continue to own the investments, the market values will continue to fluctuate up and down, but given enough time, it’s highly likely that you’ll recover the loss. It’s because remember, you are investing in companies that provide essential products and services to the global economy, and the majority of those companies are highly likely to continue to be in existence for many decades to come.

When it comes to investing, having the discipline to stay invested, so to do what you said you would do on that risk tolerance questionnaire so that you can earn interest on your interest is one of the keys to investing success as Albert Einstein once said,

Compound interest is the eighth wonder of the world. He who understands it, earns it, and he who doesn’t pays it.

So where are we right now? While it’s really the inflation story that’s driving a lot of the calamity in the markets, as I stated in commentaries earlier this year, our base case was and continues to be that inflationary pressures in the US will ease in the second half of 2022. And that is what we are seeing is just coming down very slowly and more slowly than we anticipated as well.

So back in June when, when I gave my last economic update, we had a year, a year seasonally just an inflationary reading of 9.1%. In July, the inflation rate was unchanged for the month, so we were down to 8.5% inflation year over year. In August, the inflation rate was up one 10th of 1% for the month. In year over year, we were down to 8.3% inflation. So while the decline in inflationary pressures has been slow, there has been a little progress on a number of fronts, and that’s one of the things I wanted to show you today. So for example, inflation expectations have declined, which is good because when people have the expectation that inflation will continue, it can be a self-fulfilling prophecy, but we’re seeing very large decreases in inflationary expectations. I’m not showing the chart for you here, but that is what we are seeing when we look at the data.

Additionally, there have been substantial declines in commodity prices, especially in oil as you can see on this chart, and you’ve likely noticed this at the gas pump, a lot of production has been able to come back online. The US rig count, which is a number of active drilling rigs throughout the US is at a current level of 764 as of last week, which is right about where it was prior to the beginning of the Covid 19 pandemic. So we have seen most of that production come back online that’s helped ease a lot of the oil prices, which was causing a lot of pressure at the gas pump. The price of copper has dropped and lumber has dropped as well.

Lumber was a big story during the COVID 19 pandemic, especially with home builders. So I wanted to show you where we’re with that right now. Lumber has dropped about 67% from its high earlier this year, and lumber prices right now are approaching pre-pandemic lows.

So some of these commodities that were really elevating all those inflationary readings over the last two years, a lot of those pressures are starting to abate or have abated quite a bit. Additionally, on the supply chain front, the COVID 19 shock is waning. The global supply chain pressure index is what I have shown here, and it’s a measurement of supply chain conditions.

And what it does is it helps us to understand how much logistics challenges are playing a role in trade and inflation and in other business trends. And when the index is high, that means that there’s more supply chain pressure than usual, and when it’s low, that means there’s less pressure.

And we have had a substantial easing in supply chain pressures. We’re back to the levels of mid-February 2020 just before the COVID 19 lockdown started in the United States.

So each of these developments, lower inflation expectations, lower commodity prices, and vastly improved supply chains is material in its own right, but together they suggest that a marked improvement in inflation will be forthcoming. It’s just taking a little bit longer than anticipated.

So given all that, what’s the cause of all the latest markets turmoil? Well, it’s the view that the Federal Reserve is not being patient enough. We’re seeing within some of these indicators again, that inflation is likely to continue moderating, but the Fed seems very determined to kill inflation quickly, and they’re being, in my view, too aggressive with interest rate hikes. After their meeting in late September, they indicated that interest rates will be higher for a longer period of time than the markets anticipated, which led to a sell-off in stocks. The aggressiveness that the Fed is showing on the inflation front is very likely to tip the US into recession because higher interest rates for longer will weaken economic growth. And we are seeing this take shape in the economy already.

The Conference Boards index of leading economic indicators or LEI peaked at an all time high early this year and has declined for six consecutive months. This is important because early weakness in the LEI has preceded every recession over the last 60 years.

Also, the difference between the 10 year treasury to three month T Bill, which I’ve spoken about extensively on past calls, is also close to inverting, and that yield curve has inverted before every recession since World War II as well.

Additionally, and this hasn’t been talked about much on the news lately, but in terms of the market anyway, but the midterm elections are just weeks away, just over month, and that usually does cause some market jitters. Historically, you do see sideways to a down market in the weeks leading up to the midterm election. So the recent dip is not unusual in that context. So what, what do we see here on the midterm elections? Well, currently the Senate is split 50/50 with Vice President Harris casting tie breaking votes on items that require a simple majority and in the upcoming midterm elections there are 35 Senate seats that are up for election. Now, 60% of those are currently held by Republicans and 40% of those by Democrats. So while Republicans only need to flip one seat to regain control of the Senate, there are some highly contentious races which make the race too close to call.

And in the House, all 435 seats are up for grabs. Now, typically big swings occur in midterm election years as midterms are often a referendum on the new administration and economy. And Biden’s approval rating is still stuck in the low forties. In midterm election years, the President’s party has lost House seats 90% of the time since World War II. So these statistics don’t bode well for the Democrats retaining control of both chambers of Congress.

Well, what does all this mean for the markets? Going in reverse order here. It’s policy, not politics is what impacts the economy and the markets. And if the midterms play out as history suggests and we have a divided government, we’re likely to experience political gridlock.

And while political gridlock is frustrating for many citizens, it’s actually good for the markets because when we don’t expect much to be accomplished by Congress, there aren’t many surprises for the markets. With a divided government, there’s often less spending, which is good for the less budget deficit long term, but it does result in slower economic growth. A divided government has been the most common political configuration and it’s occurred 61% of the time since World War II. Overall, I don’t think the outcome of the midterm elections is going to have much of an impact on the market this year, although I will say that historically markets have tended to rally following midterm elections.

Okay, in terms of the stock market right now, the stock market is sitting slightly below its mid June lows. As the market’s digest, interest rates likely staying higher for longer. And if we follow the Federal Reserve’s own predictions for how high they’re going to raise interest rates, we’re now about two thirds of the way through the rate hiking cycle.

From a historical perspective, the stock market usually moves higher before the Federal Reserve is done raising rates. Major parts of the bond market are currently trading at yields that haven’t been this appealing in more than a decade. So looking forward, a lot of the pain is probably already done and we’re starting from a good, um, it’s a good starting point right now. That doesn’t mean it’s gonna be smooth sailing from here. All I’m saying is that forward returns look much more compelling today than they were at the start of the year.

Additionally, one of the things we’d like to monitor is investor sentiment to get a sense of how optimistic or pessimistic investors are in the current environment, because extreme levels of pessimism are contrarian indicators and historically resulted in better than average forward looking returns. And this is the environment in which we find ourselves.

For example, the American Association of Individual Investors does a survey every week to see how bullish or bearish investors are about the market. And last week’s investor sentiment reading indicated that 61% of people think that the stock market will be lower six months in the future. So for context, that is the most pessimistic reading since the great financial crisis in 2009. And it’s also the fourth highest reading since the index began publishing results in 1987.

So investors are more pessimistic today about the markets than they were during the covid 19 lows. We look at this reading favorably because it means that fewer sellers are likely left in the market to push prices lower. Additionally, a lot of technical indicators that we follow are flashing oversold ratings across both the domestic stock, international stock and bond markets. So those are indications that we may at least see a short term rally soon.

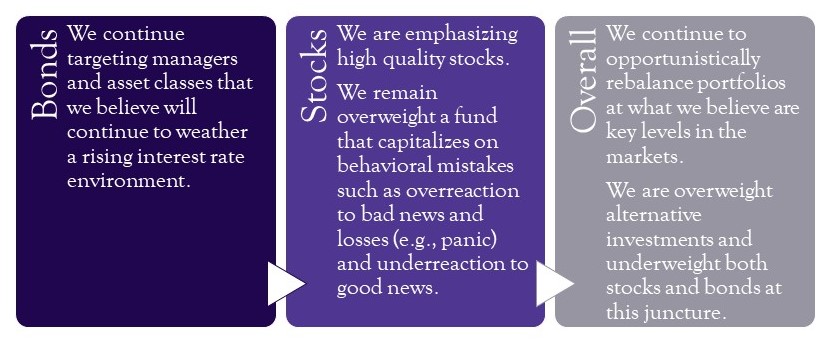

What are we doing overall in the portfolios to manage through this very difficult investing environment? Well, on the bond side, we continue to target managers in asset classes that we believe will continue to weather a rising interest rate environment. We’re targeting asset classes such as floating rate loans whose yield adjusts higher as interest rates increase. As we see that a recession may be getting closer, some of the managers in which we’re investing have been extending duration or interest rate risk and going higher credit quality into government securities, which tend to protect well in a recessionary environment. So those are some things we’re doing under the surface on the bond side.

On the stock side, we continue to emphasize high quality stocks in our portfolios that can weather an economic downturn. We remain focused on a fund that capitalizes on behavioral mistakes such as overreaction to bad news and losses or panic in the markets and under reaction to good news. A behavioral finance fund like that can do very well in terms of a market environment like this where we do see a lot of investor over reaction to bad news as the market continues to be very volatile. And additionally underneath the surface, a lot of the funds in which we invest have been increasing their levels of cash as a hedge for any further down side on within the stock market.

So while you might not be seeing many changes when you’re just looking at your statement, there’s a lot going on underneath the surface that we are keeping tabs on and a lot of the managers are repositioning their portfolios based on the recent news that we’ve had about what the Federal Reserve is going to be doing with the interest rates.

Overall, we continue to opportunistically rebalance portfolios of what we believe our key levels in the markets, and we also remain overweight alternative investments within the light point portfolios and underweight both stocks and bonds. At this juncture, we have let the alternative investments run a bit, which has resulted in in both stocks and bonds being a bit underweight. We continue to assess the global economy in the markets and we will make changes to the portfolios as warranted. As always, thank you for being a valued client of ours, and please reach out to us with any questions that you may have.

Would you like your investments to have a positive impact on the world? Give us a call!?

Do you know what Business Practices You Are Supporting through your Current Investments?

Or Contact Us to Schedule a Phone Call or Meeting.

Call us today! (540) 345-3891