What caused the recent market volatility and what should investors expect next?

In this quarterly market update, Beacon Wealth’s Chief Investment Officer Hillary Sunderland joins Director of Financial Planning Jake Preston to break down what happened in the markets during the first quarter of 2026 and what it means for your portfolio moving forward.

After a strong 2025, markets faced new uncertainty driven by geopolitical tensions in the Middle East, a sharp spike in oil prices, and ongoing questions around inflation and tariffs. In this video, we provide context, perspective, and guidance to help you stay grounded in a long-term investment strategy.

In this video, we cover:

- What drove market volatility in Q1 2026

- How stocks, bonds, and other asset classes performed

- The impact of rising oil prices and inflation concerns

- Recession risk and the strength of corporate earnings

- Updates on tariffs and global trade policy

- Why diversification and long-term investing still matter

While short-term market movements can be unsettling, history shows that volatility is a normal part of investing. Staying disciplined and focused on long-term goals is key to navigating uncertain times.

If you have questions about your portfolio or financial plan, our team is here to help.

Full transcript below

Transcript

Jake Preston: Well, hi everyone, welcome to our quarterly market update. I’m Jake Preston, I’m the Director of Financial Planning here at Beacon Wealth, and I’m joined by our Chief Investment Officer, Hillary Sunderland. Hilary, it’s great to be with you.

Hillary Sunderland: Great to be with you, Jake.

Jake Preston: And in this video, we’re going to be walking through what happened in the markets over the past quarter. We’re going to talk about what’s driving headlines, as well as looking forward into the upcoming quarter and throughout the rest of the year, and what our team expects. And so, Hilary, the market started the year on strong footing, but pretty quickly turned volatile. Can you walk us through what happened and how different asset classes performed during the first quarter?

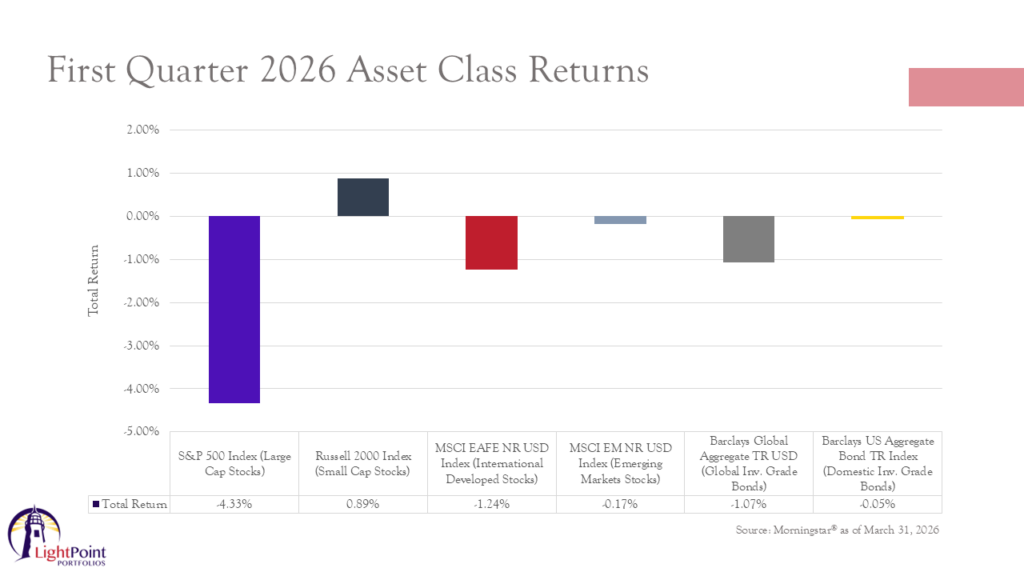

Hillary Sunderland: Sure. Well, in 2025, we had robust returns across asset classes, and many investors came into this year feeling very optimistic. We had a strong start in foreign stocks, but as you said, strength quickly reversed following the announcement of Operation Epic Fury in the Middle East, which drove a sharp rise in oil prices.

Brent crude oil prices spiked more than 60% in the month of March.

Which was not our base case scenario heading into the quarter, and this pressured stock and bond markets alike. As shown on this chart, from left to right, domestic large cap stocks were down 4.33%, small-cap stocks slipped into correction territory, but ended the quarter up just shy of 1%.

Both international and emerging market stocks were pressured by a rising U.S. dollar, and were down 1.24% and 0.17%, respectively.

And then on the fixed income side, interest rates rose on concern that a rapid rise in energy prices would put upward pressure on inflation, and that resulted in a slight decline for broad global and domestic bond markets, as this created a lot of uncertainty ahead for the direction of interest rates.

Not shown on this chart, but even gold, which is typically viewed as a safe haven asset, was down in March and lost about 11%. Gold tends to exhibit an inverse relationship to both rising bond yields and a stronger U.S. dollar. And so overall, not a great quarter, but we are following up on a very strong year of returns in 2025.

Jake Preston: Yeah, that’s helpful for perspective. Well, as you mentioned, oil prices are back in focus, given a lot of what’s happening in the Middle East, and that’s raising concern about inflation and the markets.

How big of a risk is this energy spike, maybe both for consumers and for investors, and what should we be watching next?

Hillary Sunderland: Yeah, well, rising energy costs can ripple through all parts of the economy, affecting the cost of goods and services, increasing inflation expectations, and complicating central bank decisions on the direction of interest rates, and this, in turn, does create a more challenging environment for both fixed income and equities, particularly if inflation proves to be more persistent than expected.

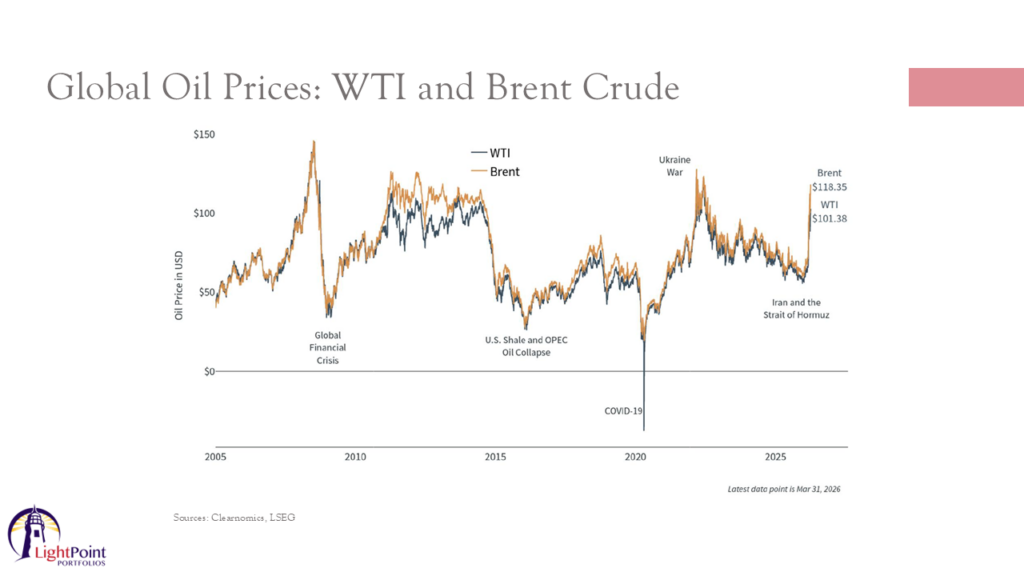

Really, the key question for investors is whether the current spike in oil prices represents a temporary risk that will fade, or the beginning of a more sustained supply shock that will reshape the inflation outlook.

This chart shows oil prices over the last two decades, and it really highlights just how volatile energy markets can be. We’ve seen sharp spikes followed by steep declines around events like the global financial crisis, COVID-19, where the price of oil actually went negative for a period of time.

As well as the invasion of Ukraine, reminding us that oil shocks are often dramatic, but they are also frequently short-lived. The most immediate impact is really being felt at the gas pump, which I know is top of mind for many of our clients.

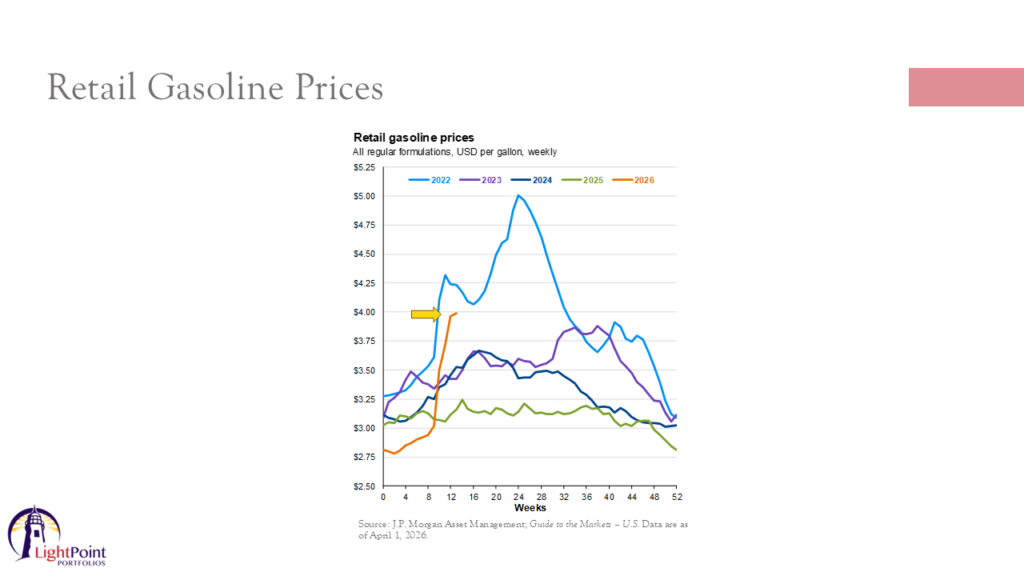

This chart shows gasoline price changes over the last 4 years, with the current year highlighted in orange.

While prices are still well below the peak in 2022, the recent upward trend does matter, right? Because higher gas prices put pressure on consumers, particularly lower-income households, and can also weigh on financial markets as well. This is something the Trump administration is aware of, especially, heading into midterm elections. So I do think, you know, uncertainty around the security of the Strait of Hormuz is likely to persist.

Despite taking out much of Iran’s military, it’s not really possible to make traffic absolutely safe coming through the strait, given the narrowness of the Strait and the enormous distances between the top of the Gulf and the Gulf of Oman, you really need, only a few bad actors to continue to cause issues in that region. And so, I do think that’s likely to keep oil prices elevated in the near term.

However, periods of elevated commodity prices have typically been self-correcting. Higher prices incentivize additional supply to come onto the market, which does take some time, while also simultaneously curbing demand. So, historically, higher energy prices do often create short-term inflationary pressures.

But past experience indicates that these effects typically ease unless disruptions to the supply are very prolonged.

Jake Preston: That’s interesting and helpful. So with these geopolitical tensions and a lot of the things that are happening in the Middle East, they’ve pushed energy prices higher, and investor sentiment overall appears to be pretty cautious.

How vulnerable do you think the U.S. economy is to a potential recession? I know we’ve talked about that a lot over the past couple of years. And what are you seeing beneath the surface in terms of corporate earnings and broader market fundamentals?

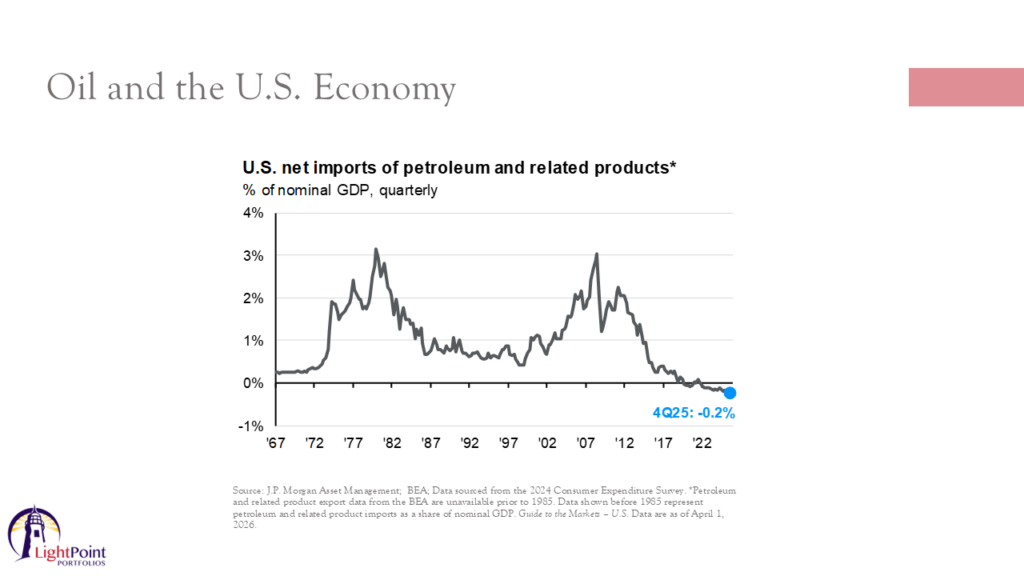

Hillary Sunderland: Yeah, well, barring a significant escalation in the war, or a long, drawn-out war, I don’t think the price of oil is currently high enough on its own to push the U.S. economy into recession. If you look at this chart and zero in on periods like the late 1970s and just before the 2008 financial crisis.

The U.S. was spending roughly 3% of gross domestic product on imported oil. Today, the U.S. is a net energy exporter, and has been for several years now. And that makes the U.S. economy far less vulnerable to oil price shocks today than it was historically. So the price of the, you know, the probability of recession has risen a bit. It’s risen to about 30% to 35% over the course of the next year, but it’s not significantly elevated, because we are a net exporter of oil.

Overall, you know, investor sentiment or, you know, how you feel about the market has weakened, but when you look under the hood and you look at the underlying fundamentals, particularly corporate profits, those remain resilient. Earnings expectations have moved higher, not lower. The strength is broad-based. Energy companies have benefited from higher oil prices.

And we’re also seeing upward earnings revisions in other sectors, like technology, materials, and utilities. So even first quarter earnings expectations continue to trend higher, despite the war breaking out in the Middle East. And even if you allow for some downside risk, and higher energy costs and input costs were to create about a 5% drag on corporate profits, earnings growth would still remain in the double digits. So overall, while markets are reacting a bit emotionally to headlines surrounding the war, the underlying data, profits, balance sheets, earnings trends, that remains solid right now.

Jake Preston: Well, that’s helpful clarification, for sure. I think it also emphasizes the importance of being invested, you know, being diversified within your investment portfolio, as well as investing in really solid companies that can withstand some of these shorter periods of volatility and uncertainty.

And so, as we’ve mentioned, the last quarter has been pretty volatile, and I’m sure that as clients have seen the headlines and even potentially looked at their accounts, it can cause some nerves and some stress, potentially, especially given how solid the performance has been over the previous 3 years. It can be a bit shocking when we have a period of volatility like this. Do you have any thoughts for our clients as it relates to navigating periods of uncertainty like we’re walking through right now?

Hillary Sunderland: Yeah, well, you know, periods of uncertainty are exactly why we build our portfolios the way that we do. Rather than trying to predict geopolitical outcomes, we focus on controlling what we can. So, we like to hedge known risks and diversify across those we can’t foresee. So our portfolios are already built to include exposure to inflation-sensitive asset classes. We’re maintaining broad diversification across global equity and fixed income markets.

And really, what we have as a result are, you know, a suite of portfolios that are designed for resilience. By staying diversified across different sectors and asset classes and geographies, and avoiding concentration in any single area, we are positioned to navigate a wide range of economic environments.

Jake Preston: Yeah, that’s helpful. Thank you.

Well, switching gears a bit, a year ago, tariffs were a major source of market turbulence. What has changed since then, and how should investors think about today’s tariff levels as compared to those earlier fears?

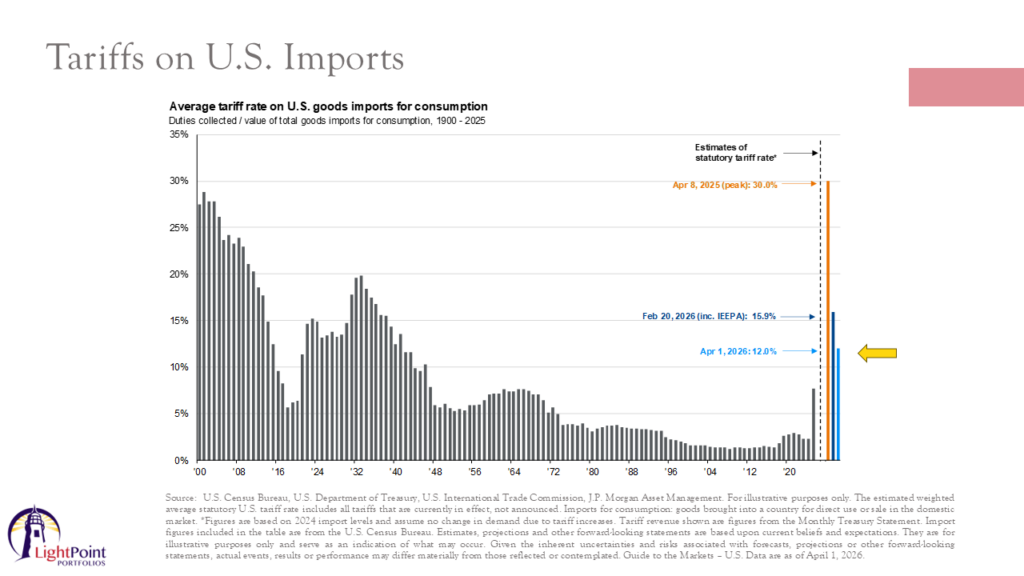

Hillary Sunderland: Well, a year ago, in April of 2025, we had some market turmoil resulting from the Liberation Day tariffs imposed by the Trump administration, and at the time, as shown on this slide by the orange bar, those proposals represented a worst-case scenario. So, a level that, if implemented, would have marked the most extreme shift in tariff rates in modern history. Since then, tariffs have moderated meaningfully and came down even more during the first quarter.

In mid-February, the Supreme Court found Trump’s tariffs imposed under the International Economic Powers Act, the IEEPA illegal. In response, the administration swiftly proposed a new 15% baseline tariff on all countries under Section 122, but right now, they’re only levying them at 10%.

Which gives us an estimated weighted average tariff rate of about 12. So as of now, tariffs are still higher than they have been for several decades, but well below the extremes we were worried about just a year ago.

Jake Preston: So, as a follow-up to that, where do you think tariff rates are headed from here?

Hillary Sunderland: Well, pulling back and, you know, looking at the big picture, tariffs are unpopular, especially when inflation is already front and center. With the midterm elections approaching, there’s really little appetite to push costs even higher for consumers, and so our view is that that tariff wave is starting to roll back.

The court decision eased some of the immediate cost pressures on companies, especially retailers, which is a good thing for earnings. There is still quite a bit of uncertainty surrounding how and when the U.S. government will refund the payments that companies made on tariffs which have since been declared illegal. But overall, compared to April of 2025, today’s lower tariff environment is a positive, and should help ease some of that inflationary pressure, that had been building over time.

Jake Preston: That seems like good news and a positive development, for sure.

My final question is, how are you helping investors place recent market performance, like we’ve experienced over the last quarter, in a long-term historical context, particularly during, like I mentioned, the pullback that we’ve experienced over the last couple of months?

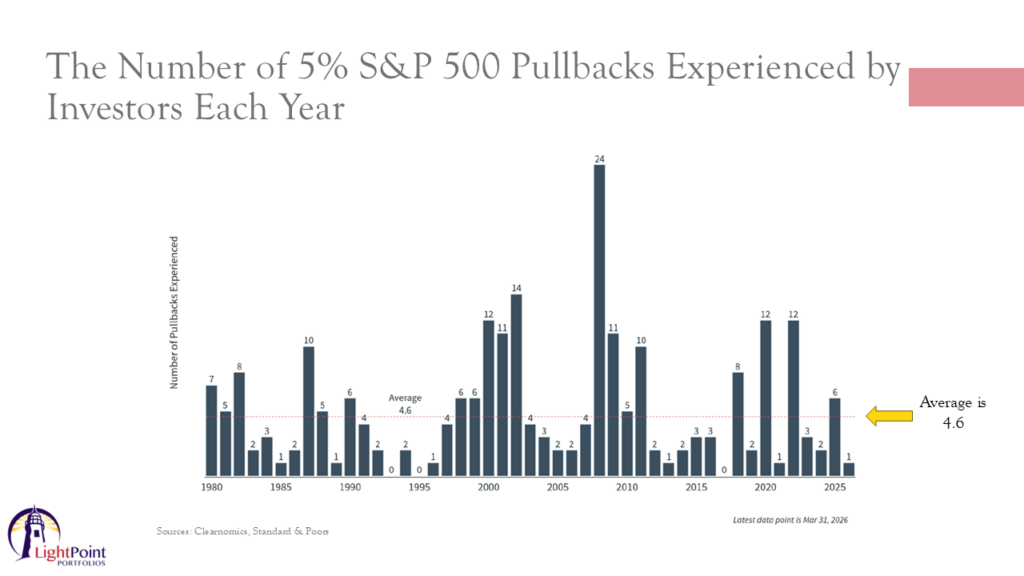

Hillary Sunderland: Yeah, well, pullbacks can always feel unsettling, but it’s always important to view these periods in context. So, stock market declines are a normal and expected part of investing, and one of the most valuable disciplines an investor can have is keeping emotions in check. The reality of investing is that returns are earned by taking on risk.

Right, and so this chart illustrates the number of S&P 500 pullbacks. A pullback is defined as a decline of at least 5% from a recent high. This chart shows the number each year since 1980, and on average, investors have experienced 4.6 pullbacks per year, underscoring how common these movements truly are.

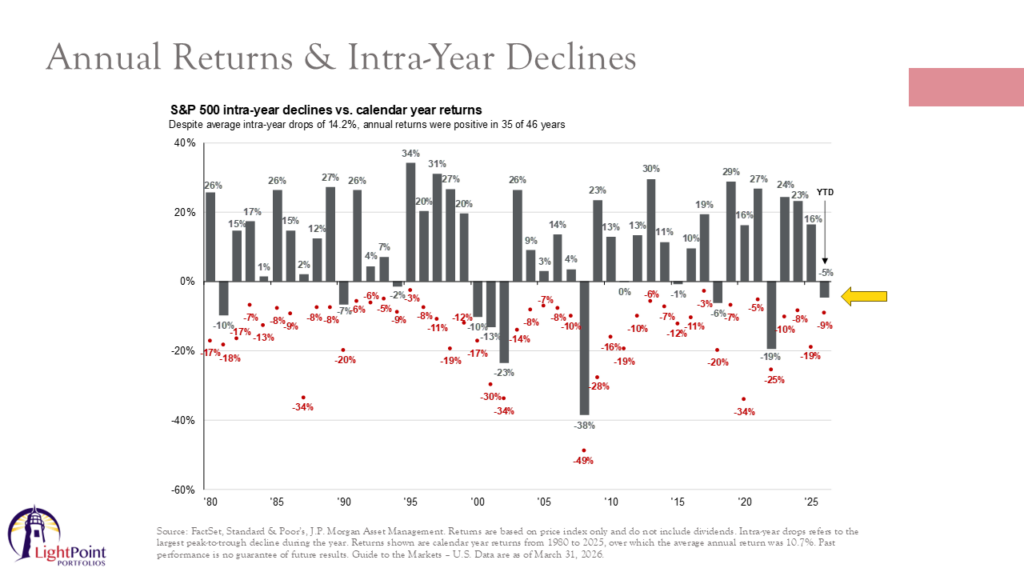

And I think the next chart further reinforces this concept by comparing the annual returns of the S&P 500, shown in gray, with the maximum inter-year drawdown, shown in red. Although investors have frequently endured meaningful inter-year declines, averaging about 14.6%, the market has ultimately delivered positive returns in most years. And so this pattern really highlights the long-term benefit of staying invested.

And reminds us that this year’s decline remains well within the range of what investors should reasonably expect to see on a regular basis.

Jake Preston: that’s really beneficial context and perspective. I think it also emphasizes the importance that we use this quote all the time, that investing success is not determined by trying to time the market, but by time in the market. And we also believe this underscores the importance of having an advisor who can walk alongside you through periods like this, be able to point you back to your financial plan that has taken into account market drawdowns and pullbacks, such as we’re experiencing now. And so we hope that all of this is helpful context and bring some perspective, and as always, we are here to answer any of your questions that you have. We are grateful for your continued trust, and Hilary, it has been great, as always, to be with you.

Hillary Sunderland: Thank you, Jake!

Jake Preston: Thank you.

Sign up for our newsletter!

Get news, market commentaries, videos, and faith-based investing articles from Beacon Wealth Consultants in your inbox.