Year-end tax surprises are no fun, and you may be surprised to learn that it’s possible owe capital gains taxes even though your account is down in value for the year. How is this possible?

In our November 2022 market commentary, Beacon Wealth Consultants’ Chief Investment Officer Hillary Sunderland, CFA®, CKA® explains this situation and what we do at Beacon Wealth Consultants to manage the tax exposure of our clients’ accounts with tax loss harvesting.

Watch our video to learn more and get a better understanding of some of the work we do behind the scenes.

If you have any questions about your financial situation, please reach out to your wealth advisor and we would be glad to address them for you. Thank you for being a valued client of ours.

Full transcript below.

Transcript

Hi, my name is Hillary Sunderland and I’m the Chief Investment Officer of Beacon Wealth Consultants and LightPoint Portfolios. This is your November, 2022 update.

Well, as you’re probably aware, 2022 has been a very difficult year for investing as both stocks and bonds have sold off on inflationary pressures, significant increases in interest rates, as well as geopolitical issues such as the Russia-Ukraine crisis. And as a result, most accounts from conservative to more aggressive accounts have had some amount of negative performance year to date, which as you know, happens from time to time when it comes to investing.

But what you may not know is that even though your account may be down in value for the year, if you have a taxable account such as an individual account, a joint account, a corporate account, or a trust account, you may still have a surprise come tax time as many investors could still owe taxes this year, even though the market is down, unless those accounts are managed very diligently for their tax exposures.

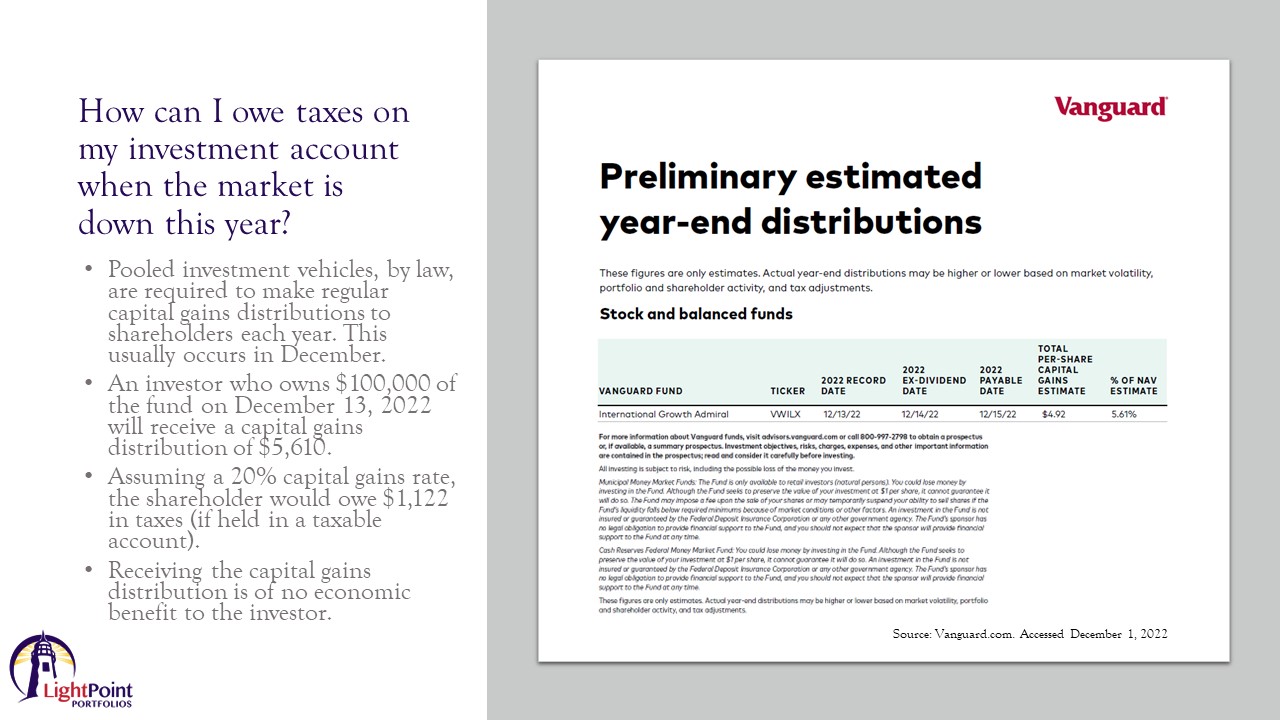

So I want to take some time today to walk through how we are managing that issue on behalf of our clients. So your first question is probably, well, how can I owe taxes on my investment account when the market is down this year? Well, the reason for that is if you ‘re in a pooled investment vehicle, such as a mutual fund or an exchange traded fund, by law, the funds are required to make regular capital gains distributions to shareholders. And you can think of a capital gains distribution this way: if a fund manager decides to sell assets within the fund, whether due to a changing outlook or to meet investor redemptions, the fund must distribute at least 95% of its gains and the resulting taxes to shareholders once per year. And that usually occurs in December of each year. So I wanted to show you how this works with an actual example that I randomly chose.

You can see a snapshot there from the Vanguard website of preliminary estimated year end distributions. So if you were to own the Vanguard International Growth Fund on December 13th, 2022, you will receive a capital gains distribution of $4.92 cents per share, which equates to a distribution of 5.61%. So if you have $100,000 invested in this fund, you’ll receive a taxable capital gains distribution of $5,610.

Now, if you own the fund in an IRA, that doesn’t matter because you don’t have to pay taxes on it. But if you own it in a taxable account, you will have to pay long term capital gains tax. So assuming that you are in the 20% capital gains rate, you would owe the IRS $1,122 in taxes even though the fund is down a little over 27% year to date through the end of November.

Now you may be thinking, well, how can a fund distribute a taxable gain if it’s lost over 25% of its value this year? And the reason for that is because fund distributions are based on the fund’s fiscal year, not the calendar year. So if the fund’s fiscal year ended during the spring, the gains are based mostly on what was earned prior to the majority of the market downturn this year.

Now, it’s important to note that receiving a capital gains distribution is of no economic benefit to you because it is not a return on your investment, it’s actually counted as a withdrawal from your investment. So managing year end capital gain distributions is extremely important. And if you didn’t know what you were doing and you happened to buy this fund on December 12th, just one day prior to the record date, you would still owe the tax even though you only owned the fund for one day.

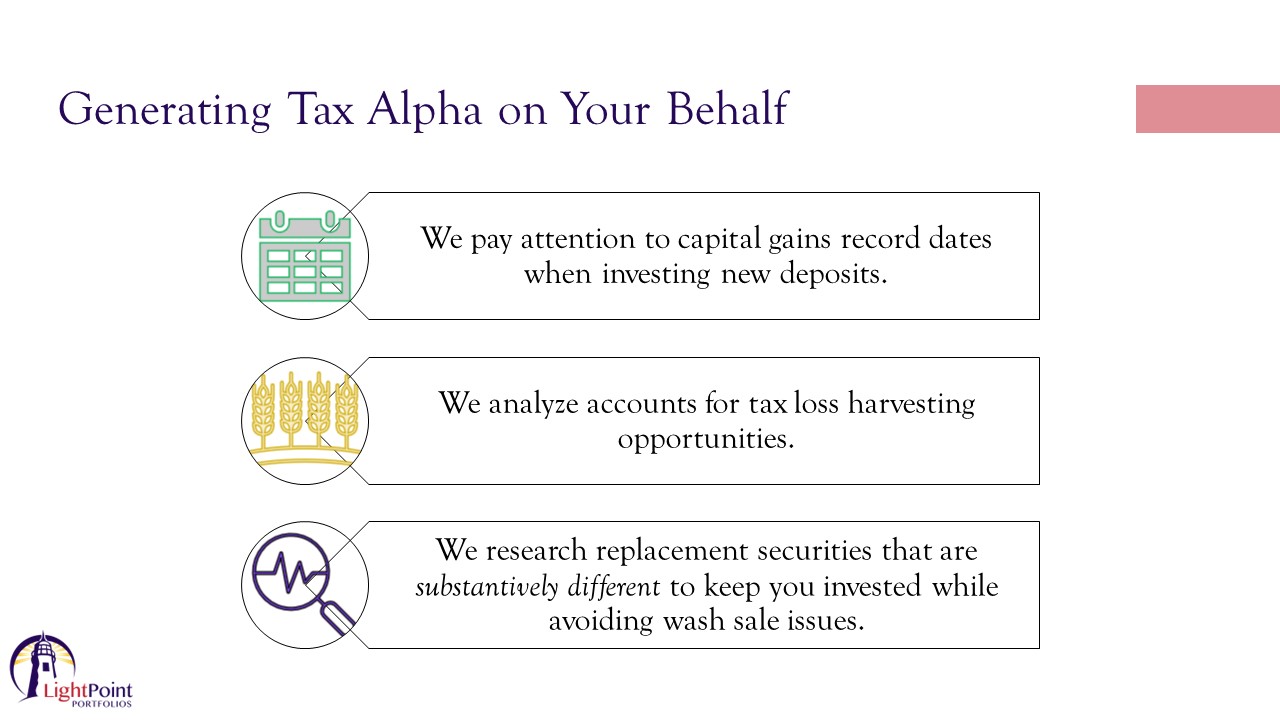

So you may not be aware that we do this for you each year, but behind the scenes we manage these issues on your behalf if you have a taxable account with us. In the investment world, this is called “tax alpha” in which we are seeking to maximize after tax returns for investors by optimizing the available tax strategies.

Now, usually we don’t talk much about this, but because this year is one of those more unique years in that capital gains payouts are so high, while returns are mostly negative, I want to walk you through how we manage this for our clients. So first, our investment team spends a considerable amount of time tracking and assessing those year end distributions, their record dates and their payable dates. And then we strategically invest around those dates in order to avoid large capital gains distributions where we can.

We also analyze each account for tax loss harvesting opportunities and throughout the year we also identify and research replacement securities that we can use to keep you invested while we are employing tax loss harvesting strategies. I’ll explain more about that in a few minutes, but first let’s get into what exactly is tax loss harvesting and how does that work?

Tax loss harvesting is really a critical tool for reducing your overall taxes. When you sell investments that have increased in value within a taxable account, you typically have to pay taxes on those earnings. You might have to pay 15% or 20% if you hold the assets for more than a year, depending on your income level. Or, if you held securities for one year or less, you pay taxes based on your marginal tax rate.

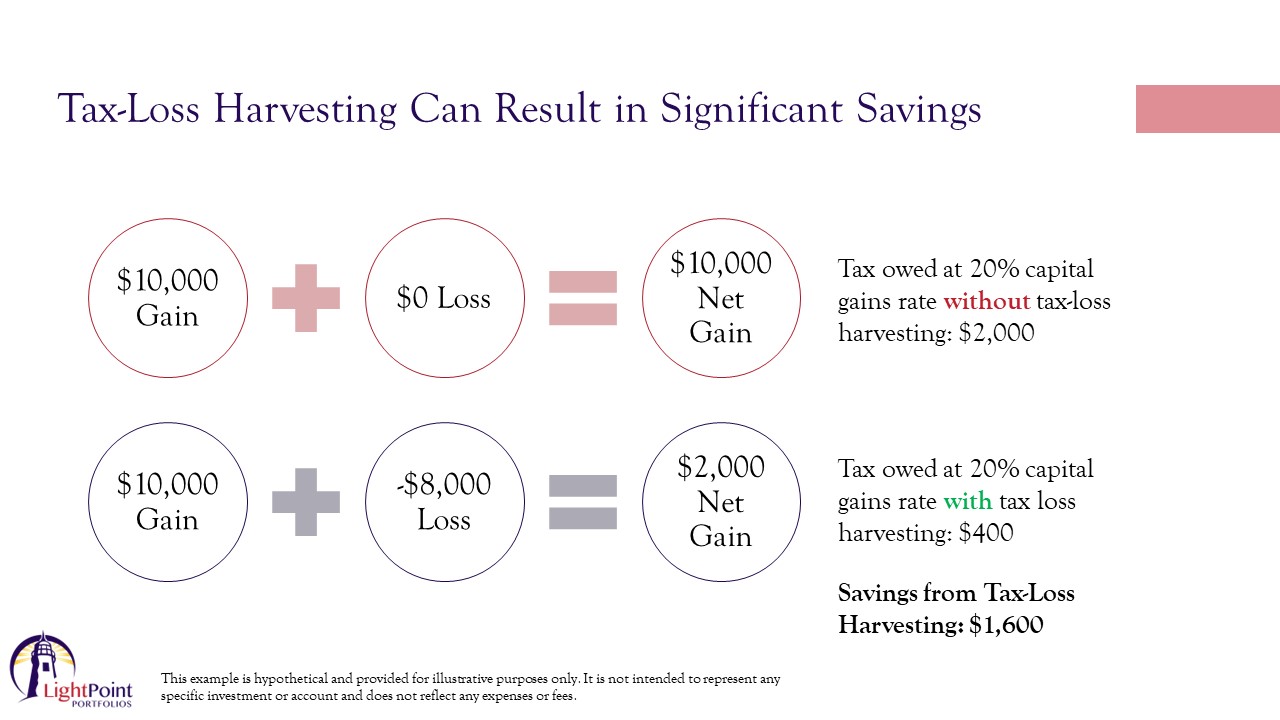

When we engage in tax loss harvesting, what we do is we look to sell securities that are at a loss to offset securities that we had taken at a profit or to offset expected capital gains distributions from funds. While this does not restore your previous position, when you take a loss, it does lessen the severity of a loss. So I wanted to walk you through mathematically how this works.

So for example, suppose you sold a security at a gain of $10,000 or you get a $10,000 capital gains distribution. If you do nothing to offset it, you will have a net gain of $10,000 for the year. If you pay taxes at the 20% capital gains rate, you would owe $2,000 in taxes. However, if you offset that $10,000 gain by selling a security that is at an $8,000 loss, your net gain is $2,000. If you pay taxes at the 20% capital gains tax rate, you would owe $400 in taxes, which is a savings of $1,600 over doing nothing.

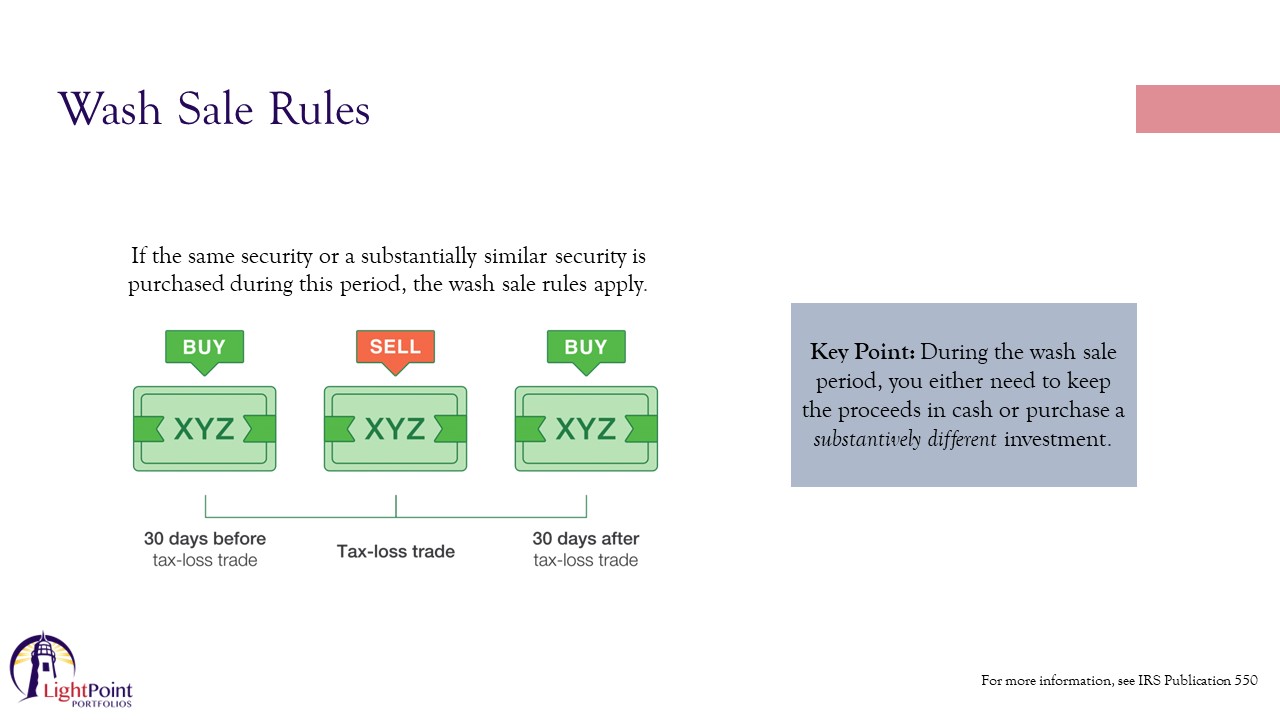

So you can see here how the strategy allows investors to realize significant tax savings, but it does take some time to implement and a lot of thought. Selling a loser in a portfolio has obvious tax advantages. However, it does inevitably disrupt the balance of the portfolio due to what the IRS calls the wash sale rule.

If you sell a security at a loss in a taxable account, you can’t buy it back for at least 30 days in the same account or in any other account that your tax ID is associated with. So for example, you can’t sell a stock in your joint account in order to take a loss and then buy it back immediately within your IRA account in order to keep the same market exposure to the security doing so would disallow the loss and this is called a “wash sale.” In other words, when wash sale rules are triggered, any harvested losses from the original sale are no longer deductible. What we have to do with the proceeds if we sell a security to take a loss is we have to figure out where to reinvest it. The proceeds can’t be reinvested in the same asset or in anything that’s substantially similar to it or else your loss will be disallowed.

So for example, you can’t sell the iShares S&P 500 ETF and then buy back the SPDR S&P 500 ETF, even though they’re issued by different fund companies, they track the exact same index. These are substantially similar securities. And so doing that would most likely disallow the tax loss.

So a big decision we make for you and we harvest losses in your portfolio is we have to decide what to do with the proceeds while we wait out that 30 day window after the sale. During that period, we either need to keep the proceeds in cash or buy a substantially different investment. Both of these introduce you to the risk that the new investment won’t generate the same performance as the original one. And so we have to put a lot of thought and research into this for you.

So if you have a taxable account with us, keep this presentation in mind as you review your year end statements. You will likely see some higher than normal trading activity in your accounts this year, as well as shorter holding periods on some investments within your account. This trading activity is due to tax loss harvesting as we seek to lessen your overall tax burden.

I hope this gives you a better understanding of some of the work we do behind the scenes. And as always, if you have any questions about your particular financial situation, please reach out to your wealth advisor and we would be glad to address them for you. Thank you for being a valued client of ours.

Are you tired of trying to manage tax loss harvesting yourself? Give us a call!

Contact Us to Schedule a Phone Call or Meeting.

Call us today! (540) 345-3891