December 5, 2017 – Recent headlines have been dominated by the prospect of tax reform which is now in its final stages. While the tax reform bills are largely uniform between the House and the Senate, there are still some significant differences that need to be ironed out – including how the bills treat the taxation of flow-through entities, whether alternative minimum tax will be eliminated or preserved, and whether the estate tax will be repealed.Some market pundits have suggested that tax reform will give the stock market a “shot in the arm” and send domestic stocks higher. Investors are cheering the progress that’s been made and are not waiting for the tax bill to take its final shape. Over the last week, we’ve seen a rotation out of the technology sector and into cheaper, undervalued stocks which have been laggards for much of the year. Sectors such as banks, retailers, energy, and transportation are expected to benefit from a stronger economy, higher interest rates, and lower taxes. Domestically-oriented small cap stocks are showing relative strength for the same reasons and are once again outpacing their large-capitalization counterparts.

While tax reform creates opportunities at the sector and company level (which is great for active managers like ourselves),the tax bill’s fiscal stimulus will likely have a more muted effect on the broader economy. It is important to note that when it comes to tax cuts, not all sectors are created equal. While the headline corporate tax rate in the United States currently stands at 35%, the rate that S&P 500 companies actually pay (the effective corporate tax rate) is only 25.6%, and significant dispersion exists across sectors when it comes to effective tax rates. For example, telecommunications companies have the highest effective tax rates and stand to benefit greatly from reform, but real estate investment trusts (REITs) do not pay taxes at the corporate level and technology companies already have operations set up around the world in an effort to pay the lowest taxes possible. Because the tax cuts will not benefit all sectors in the same manner, the flow-through effect to employee wages, hiring, and investment spending will likely not be broad-based, and it will take time to assess the overall impact on the economy. That being said, there are legitimate reasons for optimism among investors. In the U.S., the unemployment rate is sitting at its lowest level in 17 years, economic growth hit a three-year high of 3.3% in the third quarter, and, for the first time in years, we are witnessing a backdrop of robust and broad-based global GDP and corporate profit growth.

I noted in last month’s commentary that bonds were trading with very tight credit spreads – leaving investors in high yield bonds with heightened risk and little room for capital appreciation. In November, there was a notable selloff in high yield bond spreads mid-month as some companies lowered revenue guidance and investors had jitters over the deductibility of interest in the new tax bill. By month-end, the underperformance of high yield was partly mitigated by strength in the oil sector. The Morningstar® US High Yield Bond Fund Category Average lost 0.27% in November. Global government bond yields were broadly flat in November. We continue to expect a very gradual pace of policy tightening in the U.S. and elsewhere and a trend toward higher levels.

On the equity side, world markets suffered a bit of a selloff in mid-November as investors took profits but rebounded to close out the month. The S&P 500 Index gained 3.07% in November while the international MSCI EAFE Index gained 1.05%. A strengthening euro and sterling versus the U.S. dollar caused much of the lag in international versus domestic stocks. Overall, we remain constructive on international stocks, especially in Europe, as November business survey data reaffirmed the euro area’s position as the major economy growing most above trend.

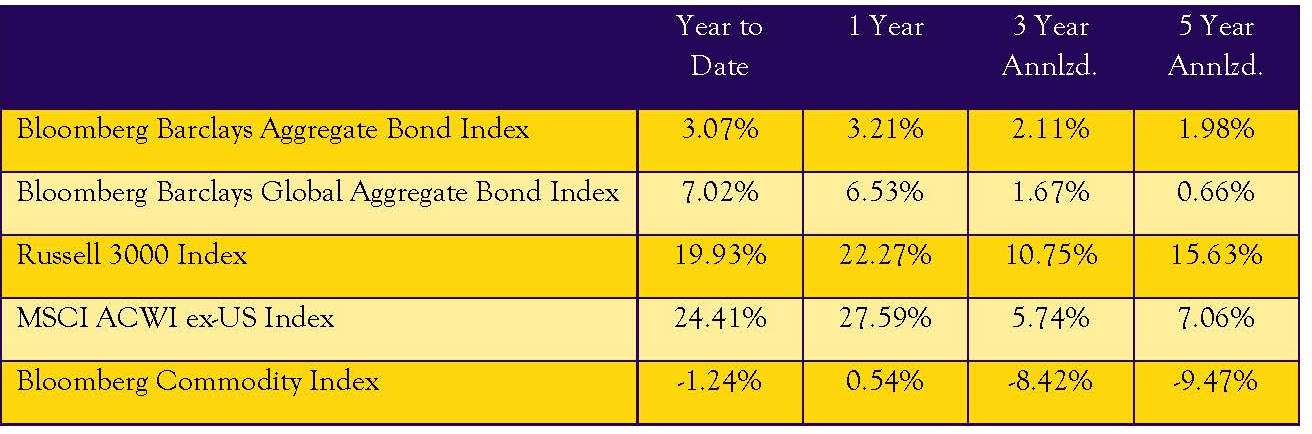

Year-to-date, the Russell 3000 Index, a broad measure of domestic stocks, is up a stunning 19.93% while the Barclays Aggregate Bond Index is up a mere 3.07%. Unless a dramatic reversal takes place in December, stocks will outperform bonds for the seventh consecutive year in 2017. Stocks have only outperformed bonds for seven consecutive years on three occasions in the past 220 years, the last of which was in 1928. Apart from the Roaring ‘20s and the Golden ‘50s, it has seldom been the case that equities, bonds and credit have been similarly expensive at the same time. History shows us that elevated valuations often signal that investment returns over the medium- and long-term will be lower. At this juncture, a lowering of return expectations heading into 2018 is prudent. As part of our process, we are continually looking for managers and investment opportunities that can further diversify portfolio risk and will incorporate them into our portfolios as appropriate.

We appreciate your continued confidence.Please reach out to us with any questions you may have and have a blessed Christmas.

-Hillary Sunderland, CFA

Chief Investment Officer for Beacon Wealth Consultants, Inc.

Index Returns

Disclosures

Financial Planning and Investment Advisory Services offered through Beacon Wealth Consultants, Inc., a Registered Investment Advisor.

The material has been prepared for informational purposes only and is not intended to provide, nor should it be relied upon for, accounting, legal, or tax advice. References to future returns are not promises or estimates of actual returns a client portfolio may achieve. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. Information and data referred to in this document has been compiled from various sources and has not been independently verified. We believe the information presented here to be reliable but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase of any financial instrument. The views and strategies described may not be suitable for all investors.

All returns represent total returns for the stated period. The Bloomberg Barclays Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The Bloomberg Barclays Global Aggregate Index is a flagship measure of global investment grade debt from twenty-four local currency markets. The S&P 500 Index is a market capitalization weighted and unmanaged group of securities considered to be representative of the stock market in general. The Russell 3000 Index is a market capitalization weighted index that measures the performance of the largest 3,000 companies representing approximately 98% of the investable U.S. equity market. The Russell 2000 Index is a market capitalization weighted index that measures the performance of the smallest 2,000 companies in the Russell 3000 Index. The MSCI ACWI ex-US Index is a market capitalization weighted index designed to provide a broad measure of equity market performance throughout the world and is comprised of stocks from both developed and emerging markets outside of the U.S. The Bloomberg Commodity Index is designed to be a highly liquid and diversified benchmark for commodity investments.

Past performance is not indicative of future results. Diversification does not guarantee investment returns and does not eliminate the risk of loss. You cannot invest directly in an index.