March 1, 2018

February was a volatile month for both stocks and bonds. The major stock market averages dipped in correction territory earlier this month – falling 10% from record highs set on January 26th. The market decline was the inevitable correction of two imbalances that have accumulated since late last year. One imbalance was the product of the stock market gaining quite a bit more than can be justified by the recent tax cuts and the resulting rise in earnings yields. The other imbalance resulted from the stock market’s apparent lack of attention to the rise in bond yields over the last few months. The 10-year Treasury had increased rapidly during December and January; however, the market had largely shaken this off as it cheered tax reform.

The problem with brushing off the increase in yields is that rising interest rates cause risk assets to be repriced. For stocks, this typically means contractions in price-to-earnings ratios and increased competition with government and corporate bond yields. The wake-up call finally came at the end of January as fears of rising inflation sent interest rates even higher and bonds reeling (bond prices generally move inversely to interest rates). The fears were exacerbated as Jerome Powellofficially took the reins from Janet Yellen as chair of the Federal Reserve in early February. While Powell has plenty of experience in the private sector, he is the first Fed chair without a degree in economics since the late 1970s. While our view is that Powell is more of a continuity candidate for the Federal Reserve, the uncertainty surrounding how he will help shape monetary policy is likely to continue for the next several months. Given that the market prefers predictability over uncertainty, this is likely to increase volatility in the near-term.

For the month of February, the Barclays Aggregate Bond Index returned -0.95%. Losses were broad-based in fixed income with government, investment grade corporate, investment grade municipal, and high yield bonds all ending the month lower.While suffering losses in fixed income is not easy for some to endure, the good news is that the bond yields are now in much better sync with the Fed.Our expectation is that the Federal Reserve will hike rates at least three times this year and may be inclined to a fourth, particularly since a series of fiscal measures, including tax cuts and increases in spending, has come to pass since December.We continue to favor opportunistic fixed income managers to navigate what is currently a difficult environment for the asset class.

On the equity side, the stock market experienced a rather quick turnaround after entering correction territory. By the end of February, the S&P 500 Index had recovered about half of its losses and ended the month down 3.69%. While the v-shaped recovery is encouraging, we believe there may be some additional volatility to come. Market breadth (a calculation of how many stocks are participating in the market advance) remains low, and small cap stocks have not been keeping pace with their large cap counterparts. Additionally, investors continue to borrow record sums (margin loans) to bet on stocks. If borrowing continues to rise at the current pace, selloffs and market volatility could become more commonplace as investors are forced to sell securities to meet margin calls.

The good news is that the economic backdrop remains strong. The domestic labor market is healthy. Unemployment is at a 17-year low, and weekly jobless claims are hovering near a four-decade low. The Conference Board’s Leading Economic Index (LEI), which historically has slowed on a year-over-year basis prior to heading into a recession, continues to trend upward. Over the last twelve months we have witnessed the best period of coordinated, above-trend global growth in almost a decade. Global manufacturing is in expansionary territory – signifying that earnings should continue to gather steam. This is lifting investment outlooks across developed and emerging economies. With this backdrop, we believe the probability of a recession occurring in the next 6-12 months is very low. Given that the business cycle is one of the most important drivers of investment performance, this is encouraging for risk assets over the intermediate-term.

We appreciate your continued confidence.Please reach out to us with any questions you may have.

-Hillary Sunderland, CFA

Chief Investment Officer for Beacon Wealth Consultants, Inc.

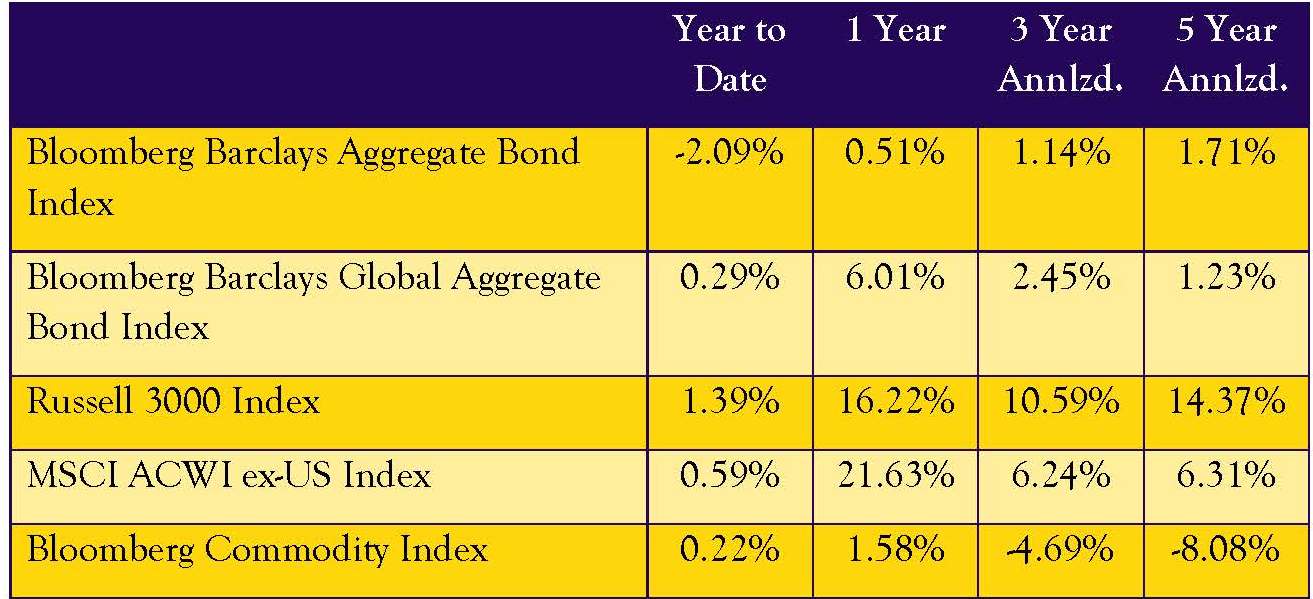

Index Returns

Source: Morningstar® as of February 28, 2018

Source: Morningstar® as of February 28, 2018

Source: Morningstar® as of February 28, 2018

Source: Morningstar® as of February 28, 2018

Disclosures

Financial Planning and Investment Advisory Services offered through Beacon Wealth Consultants, Inc., a Registered Investment Advisor.

The material has been prepared for informational purposes only and is not intended to provide, nor should it be relied upon for, accounting, legal, or tax advice. References to future returns are not promises or estimates of actual returns a client portfolio may achieve. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. Information and data referred to in this document has been compiled from various sources and has not been independently verified. We believe the information presented here to be reliable but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase of any financial instrument. The views and strategies described may not be suitable for all investors.

All returns represent total returns for the stated period. The Bloomberg Barclays Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The Bloomberg Barclays Global Aggregate Index is a flagship measure of global investment grade debt from twenty-four local currency markets. The S&P 500 Index is a market capitalization weighted and unmanaged group of securities considered to be representative of the stock market in general. The Russell 3000 Index is a market capitalization weighted index that measures the performance of the largest 3,000 companies representing approximately 98% of the investable U.S. equity market. The Russell 2000 Index is a market capitalization weighted index that measures the performance of the smallest 2,000 companies in the Russell 3000 Index. The MSCI ACWI ex-US Index is a market capitalization weighted index designed to provide a broad measure of equity market performance throughout the world and is comprised of stocks from both developed and emerging markets outside of the U.S. The Bloomberg Commodity Index is designed to be a highly liquid and diversified benchmark for commodity investments.

Past performance is not indicative of future results. Diversification does not guarantee investment returns and does not eliminate the risk of loss. You cannot invest directly in an index.