Bond yields continued to capture the headlines for much of May. The 10-year Treasury started the month at a yield of 2.94%, reached a seven-year high above 3%, and then closed the month at a yield of 2.82% as investors assumed a risk-off trade at the end of the month on political turmoil in Italy. While the lower yields gave bond investors a much-needed reprieve in May (given that bond prices move inversely to yield), bonds are still facing the headwind of rising rates year-to-date. Inflation has risen substantially from 2017 lows, and the market is now pricing in a near 100% chance of the Federal Reserve hiking rates again in June. For bond investors, it’s been a very difficult environment with the major bond asset classes – including domestic investment grade, high yield, global investment grade, municipal bonds, and inflation-protected bonds – all experiencing losses year-to-date.Thankfully for our clients, each of our core bond positions in our portfolios have outperformed the broad bond market year-to-date, with some even experiencing gains in this difficult environment.

While that certainly is good news for our clients, some are still concerned about the impact higher bond yields will have on equity markets. Higher interest rates are traditionally seen as a negative for the stock market because companies have higher borrowing costs and, thus, less room to pay dividends to investors. Also, at some point, bond yields will be more enticing to investors and will decrease the desire to own stocks instead of bonds given the additional risk one assumes by investing in stocks. This can lead to a sell-off in equity markets.

While these are valid concerns, history has shown that higher interest rates alone are a poor indicator of subsequent equity returns. Consider that in all but one rate hiking cycle since 1988, domestic equities were able to generate double-digit returns over the following 12 months. This is because what is driving the rates higher is important. Equities can perform well to the extent that higher rates reflect strong economic growth prospects, as is the current case.For example, the economy added 223,000 jobs last month, topping a forecast of 188,000, and the unemployment rate dropped to 3.8%, its lowest since April 2000. Furthermore, the latest retail sales report showed continued strength which is a positive to domestic growth given that consumer spending drives much of our economy. The data highlights the fundamental strength of the U.S. economy, and the positive backdrop we have for the stock market.

So where do we stand year-to-date? Returns in the more prominent stock market indices such as the Dow Jones Industrial Average and the S&P 500, have been mediocre in comparison to the last few years, but there’s a nice bull market going on behind the scenes. Smallcap stocks are less sensitive to interest rates due to smaller dividends and are less sensitive to a rising dollar given that more of their revenues are generated domestically than their large cap counterparts. As such, it should come as no surprise that small cap stocks have been performing well this year, with the small cap Russell 2000 Index up 6.90% year-to-date versus 2.02% for the large cap S&P 500 Index.

Returns abroad have not been as strong. International developed markets, as measured by the MSCI EAFE Index, are down -1.55% year-to-date. Political developments led to a spike in volatility at the end of May with the announcement of new governments in Italy and Spain and the implementation of steel and aluminum tariffs on some of our largest trading partners, including Canada, Mexico, and the European Union, by the U.S.A strengthening dollar also put pressure on returns in May.

Emerging markets have been feeling the brunt of the rising dollar and have been increasingly pressured to support their currencies by halting interest rate cuts or even tightening monetary policy. This has added to investor concerns about growing stresses on their economies and has been a headwind for both the emerging market stock and bond markets as of late. The MSCI Emerging Market Index lost -3.54% for the month, while the JPMorgan Emerging Market Bond Globally Diversified Index lost -0.94%. Emerging market debt returns continued to be dented by significant losses in Argentina and Turkey, where stresses stemming from the increase in the U.S. dollar have caused those countries’ central banks to raise interest rates – with Argentina’s interest rate now at a stunning 40% to support the peso which has lost a quarter of its value over the past year.

Looking ahead, challenges such as protectionist rhetoric, the risk of regulation in the technology sector, and a gradual rise in rates remain. The key for investors is to separate the signal from the noise. While economic global growth has moderated this year, the bar has also been lowered for positive news going forward. While interest rates have increased, this has also reduced the risk of a further rapid rise in rates in 2018, and rates are now more in line which what we would expect given the current economic environment. These developments, coupled with the sideways movement in the large cap equity markets, have created more room for potential upside to risk assets.

Thank you for your continued confidence. Please reach out to us with any questions you may have.

-Hillary Sunderland, CFA®, CKA®

Chief Investment Officer for Beacon Wealth Consultants, Inc.

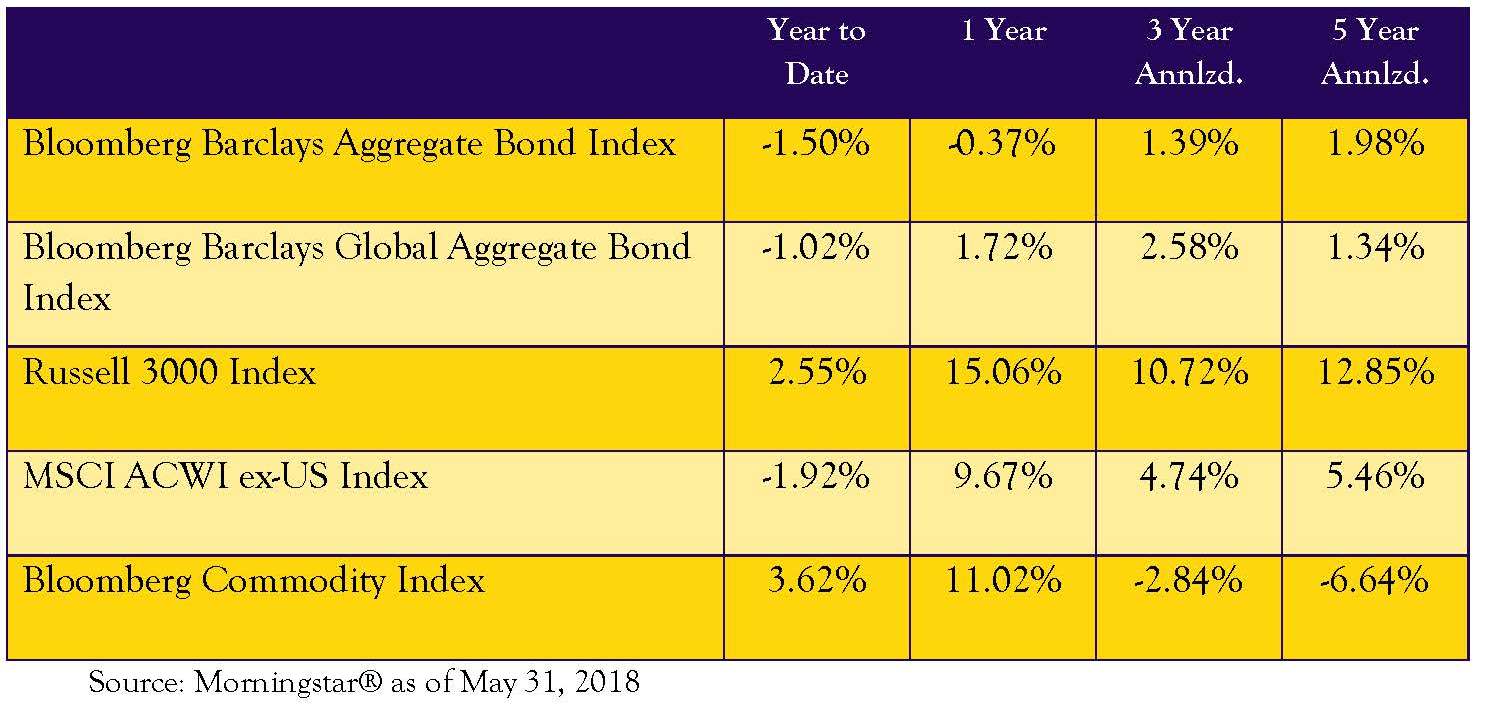

Index Returns

Disclosures

Financial Planning and Investment Advisory Services offered through Beacon Wealth Consultants, Inc., a Registered Investment Advisor.

The material has been prepared for informational purposes only and is not intended to provide, nor should it be relied upon for, accounting, legal, or tax advice. References to future returns are not promises or estimates of actual returns a client portfolio may achieve. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. Information and data referred to in this document has been compiled from various sources and has not been independently verified. We believe the information presented here to be reliable but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase of any financial instrument. The views and strategies described may not be suitable for all investors.

All returns represent total returns for the stated period. The Bloomberg Barclays Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The Bloomberg Barclays Global Aggregate Index is a flagship measure of global investment grade debt from twenty-four local currency markets. The S&P 500 Index is a market capitalization weighted and unmanaged group of securities considered to be representative of the stock market in general. The Russell 3000 Index is a market capitalization weighted index that measures the performance of the largest 3,000 companies representing approximately 98% of the investable U.S. equity market. The Russell 2000 Index is a market capitalization weighted index that measures the performance of the smallest 2,000 companies in the Russell 3000 Index. The MSCI ACWI ex-US Index is a market capitalization weighted index designed to provide a broad measure of equity market performance throughout the world and is comprised of stocks from both developed and emerging markets outside of the U.S. The Bloomberg Commodity Index is designed to be a highly liquid and diversified benchmark for commodity investments.

Past performance is not indicative of future results. Diversification does not guarantee investment returns and does not eliminate the risk of loss. You cannot invest directly in an index.