Are you worried about inflation and by the recent volatility in the markets? In this month’s commentary, Beacon Wealth Consultants’ Chief Investment Officer Hillary Sunderland, CFA®, CKA® answers four questions that are keeping investors up at night:

- Do I need to worry about inflation?

- Is the increase in interest rates going to cause a recession?

- Should I sell out of bonds?

- Are we nearing the bottom of the market decline?

We hope Hillary’s discussion of these questions helps you understand what is happening in the economy and the markets and gives you hope and confidence to stay the course. While it has been a challenging year for both stock and bond markets, we believe that the portfolios are well positioned based on our economic outlook.

Thank you for your continued confidence and as always, please reach out to us with any questions that you may have.

Full transcript below.

Transcript

Hi, my name is Hillary Sunderland and I’m the Chief Investment Officer of Beacon Wealth Consultants and LightPoint™ Portfolios. We’ve been getting quite a few client questions concerning the market environment, as well as the economic environment, given a lot of the news headlines lately. So I’m doing this May update a little bit early to answer some of the top questions we’re receiving from our clients. We thank you for continuing to be a valued client of ours, and we hope that you find this to be useful. So let’s jump right in.

Do I need to worry about inflation?

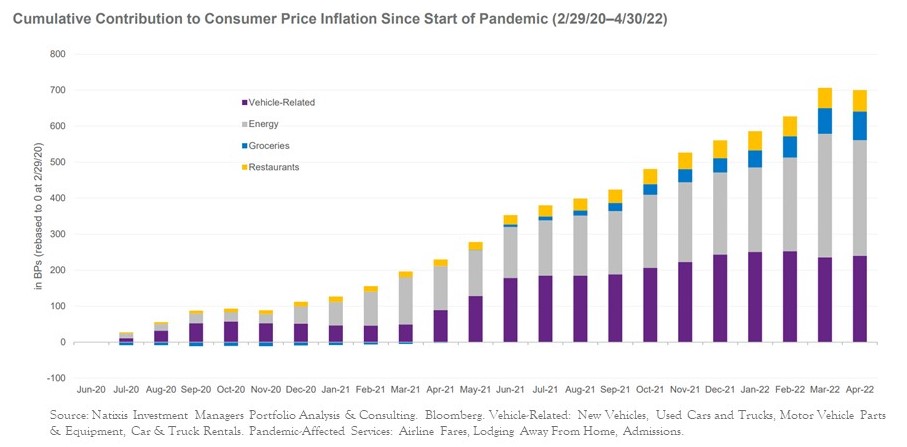

So one of the top questions I’m receiving from our clients is do I need to be worried about inflation? Well, inflation is here, but we do believe that the rate of price increases that we’ve seen is unsustainable. As shown on this chart, a lot of the increase in inflation came from two areas, vehicle related costs, which are shown in purple and energy in gray.

I’m going to address each of these in turn. So used car prices, the purple, will count for about one third of the inflation spike that we saw over the past year. You may recall that when the pandemic hit, auto makers expected car demand to plummet, and as a result, they reduced output. So microchip manufacturers followed suit. With the shortage of new cars, consumers began to use the stimulus checks they were receiving as well as the low interest rate environment to purchase used cars instead of new cars, which drove up the prices of used cars, four times faster than that of new cars, this really was a temporary supply and demand imbalance. What we are seeing now is that the supply and demand imbalance is starting to abate as chip manufacturers are starting to catch up with demand. This has allowed the inventory of new cars to rise and as shown on the chart here, we’re starting to see the price of used cars come down.

So the price of the average used car sold in America has declined for three straight months. And this is one of the major reasons why I don’t think that 8% to 9% inflation that we’ve been seeing is here to stay. Because again, a lot of the increase, about one third of the increase, in inflation came from the increase in the price of vehicles. Okay.

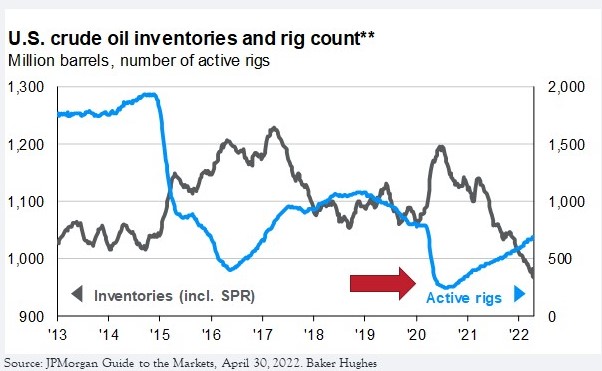

The other area I addressed a minute ago is the big spike in inflation due to energy prices. And I’m sure you’ve all experienced this at the gas pump. Now, one thing to remember here is that during the pandemic demand for energy plummeted. One thing I remember doing is there was one market update where I announced that the price of oil had actually gone negative because of the plummeting demand during the pandemic. The oil rig count shown by the blue line here went down.

So pre-pandemic, there were about 890 active rigs. During the pandemic hundreds of these went offline because they simply weren’t profitable whenever oil was priced as low as it was. So energy companies faced unprecedented write-downs, tens of thousands of job cuts, the rig count plummeted to about 170 at its low. And then when COVID concerns abated and demand started to increase and demand increased in a hurry for people to get back out after being stuck at home for two years. It has just taken a while for these rigs to come back online. Workers have to be rehired. Machinery has to be replaced. Oil companies are having trouble finding workers to be willing to go back to work in some of these areas. And so that has caused a bit of a problem as well with bringing some of these oil rigs back online.

So we are now back to a rig count of about 700, which is about 80 to 85% of where we were pre-pandemic. As these rigs continue to come back online, this should help ease prices, but it’s likely going to take several more months before we are able to get back to full capacity. And the situation in Russia and Ukraine has exacerbated the issue. So even though the U.S. is not reliant on Russia for oil, oil’s still a global commodity. So when prices spike elsewhere in the world due to less supply of an item than is demanded, it still results in increased prices for all of us. So the geopolitical situation certainly bears monitoring, but again, we are seeing that supply coming back online, which should help prices to ease, but likely not until later this summer. Again, though, this is a big part of that inflationary component.

So if we’re seeing a lot of the supplies start to come back online, that should help ease inflation over the second half of 2022.

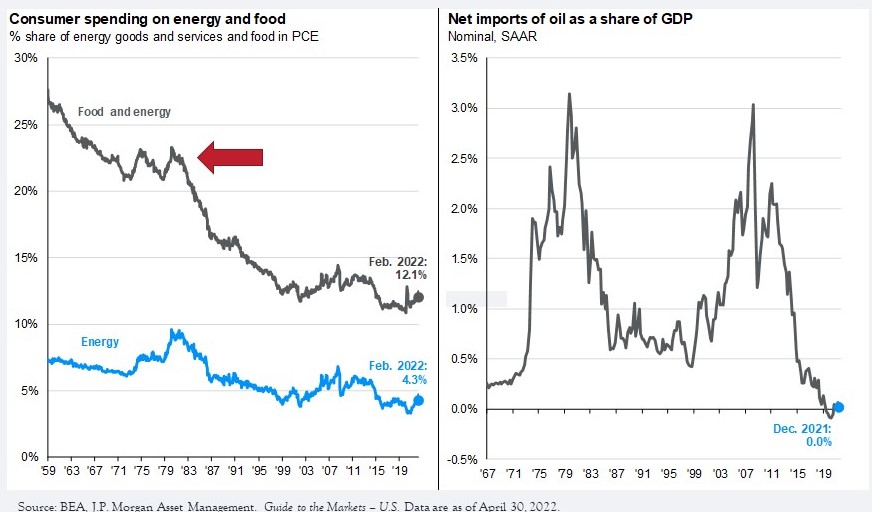

I know that this inflation has been painful, especially for those on a fixed income. We haven’t had an inflationary shock as bad as this for over 40 years. So I thought it would be interesting to show you how this compares to the inflationary shock of the 1970s. As you can see in the left hand side of this chart during the 1970s, about 22 and a half percent of consumer spending was just on food and energy. Due to technological innovation, as well as domestic production and the move to cleaner energy sources, we’re only spending about 12% on food and energy today.

The right hand chart here shows our net imports of oil as a percentage of gross domestic product throughout history, which is down to 0% at the end of 2022, which is quite a remarkable transition in terms of our energy dependence as a nation. We’re simply not in the same place that we were 50 years ago when it comes to the impact that higher oil prices have on our country. Now I know that this is still short term pain, but it’s not as bad as it was. And so I’ve heard a lot of comparisons. So this is the same the 1970s, but when you look at the data, it’s really not the same. This is a very different environment.

Okay, the other thing to note here is that, I know that it hurts when you go to the store, to the gas pump, however, in terms of the stock market, when you think about how the inflation picture will impact the stock market ahead, it’s actually the expectation about inflation that matters to the stock market. Remember the stock market is forward looking, looking ahead, six to 12 months, trying to ascertain what may happen in the future and companies, you know, make decisions based on what they think’s going to happen in the future. And so if we’re starting to see some of these used car prices roll over, we see a lot of these oil rigs coming back online, and that’s accounting for quite a bit of that inflationary spike, as that expectation about future inflation changes you’re going to start to see a change in the stock market, as well as in the bond market because there are a lot inflationary fears there as well. So as we start to see these expectations roll over, that should be beneficial to both stocks and bonds.

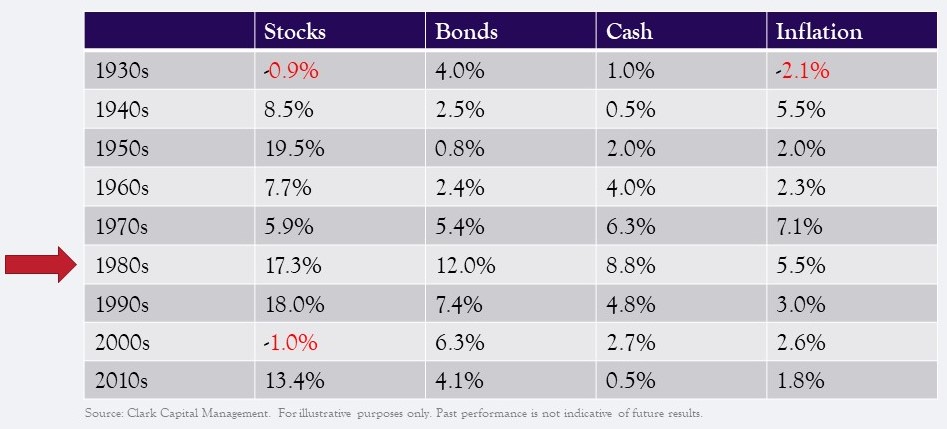

Also, it’s important to note that the media portrays the image that inflation is, you know, the end of the world for the stock market. So let’s take a look at this from a historical perspective. Historically stocks have actually performed reasonably well during inflationary periods. Look at how well stocks performed during the last 5% plus inflationary period: the 1980s.

Remember that when you are investing in the stock market, you’re investing in companies and companies can raise their prices to defend their margins. Okay. So really in terms of my view on this, I believe that your biggest concern in an inflationary environment like this should not be about the stock market and what it’s doing, it should actually be about uninvested cash.

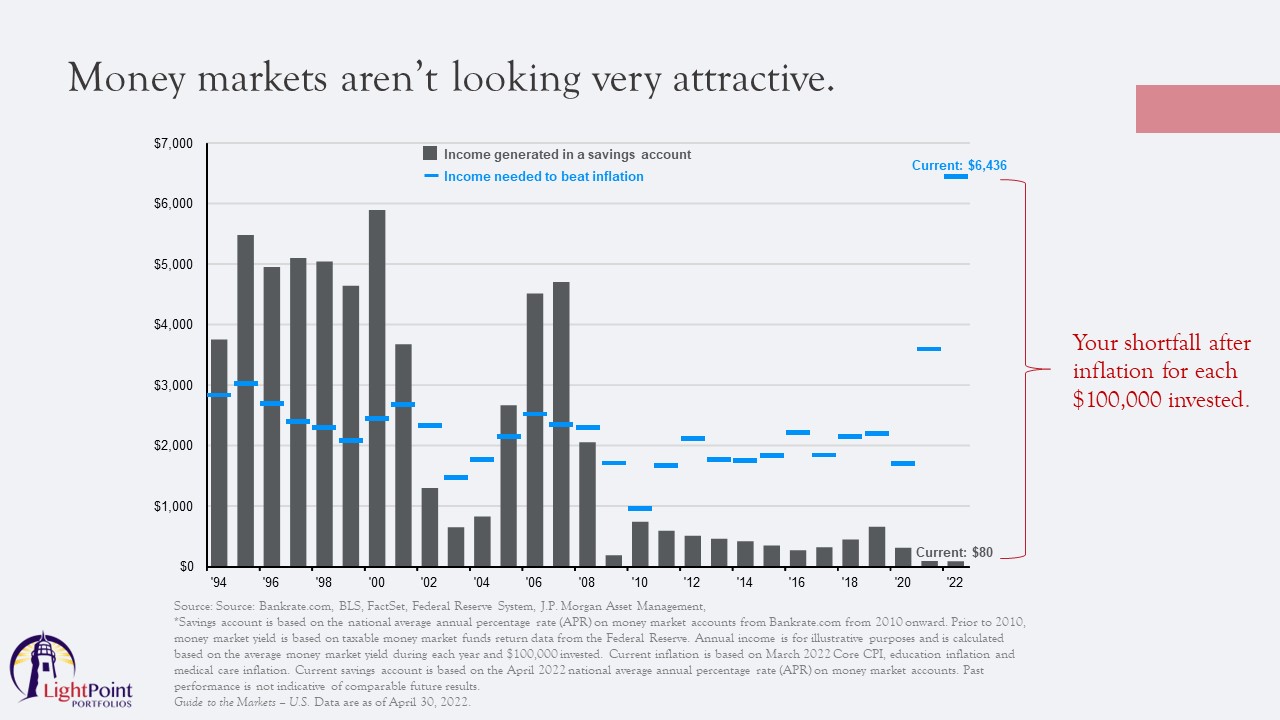

Look at the cash return you were getting in the 1980s, 8.8% when inflation was averaging about 5.5, this is not what we have today. This is not the case today. And so you can’t go back to the 1980s playbook where, well, if I just put everything into cash and my money market is earning more than inflation, I’ll be okay. I can hedge my losses that way. This isn’t the 1980s. We need to have a different playbook for this environment because the amount of money you’re getting in the money market is very, very different today. If you cash out of the market today and go to cash, not only are you locking in losses within your investment account, but you’ll also be locking in a loss when you invest in a money market account. So why do I say this? Well the average money market account is paying next to nothing.

This chart shows how much money an investor should expect to earn based on each $100,000 invested in a savings account. The current national rate is $80 per $100,000 investment. So at the current rate of inflation, you would lose over $6,000 in purchasing power for each $100,000 you have invested in any money market. So remember that the losses on your investment account are only on paper. Once you sell, you realize those losses. And then not only are you locking in your losses on your investment account, but you are also compounding those losses by sticking it in a money market that’s losing purchasing power as well due to inflation. All right.

Is the increase in interest rates going to cause a recession?

So let’s move on to the next question: but isn’t our rise in the interest rates going to cause a recession? So maybe that’s why I want to bail out of the markets. Well maybe, depending on how the Fed engineers this landing of this easy interest rate environment that we’ve had, it could cause a recession, but it might not.

The probability of recession in any given year is about 15%. The probability of recession occurring in 2022, we peg at about 30 to 35%. So that is elevated relative to a normal year, but it’s certainly not the certainty that the media makes it out to be. Another recession only two years after the previous one would be highly unusual. And remember the Federal Reserve raises interest rates if the economy is strong enough that it needs to be slowed down.

So if you watch CNBC, you’re likely to hear a lot about something called a yield curve inversion. I want to go over this because I have seen it all over the news over the last few weeks. A yield curve inversion is an unusual state for the bond market to be in. So usually a yield curve looks like the left hand chart shown here. As investors are willing to invest for a longer period of time on the X axis, they’re compensated by higher yield on bonds.

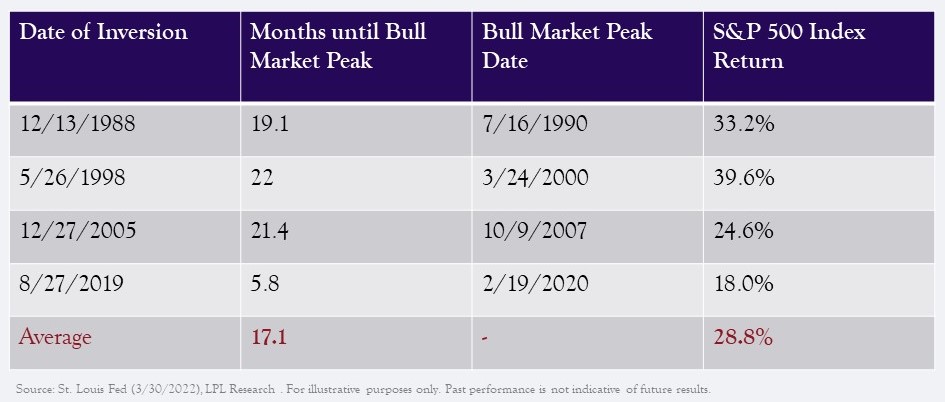

So as you invest in longer maturities, the yield you receive to be compensated for that locked up investment is higher. Okay. A yield curve inversion, which is the right hand chart, occurs when the yield of a short term bond is higher than the yield on a long term bond. So to say it another way, it’s when investors are compensated more for investing over a shorter period of time than over a longer period of time. Now, historically when yield curve inverts, when it looks like what you’re seeing on the right hand side, this is a good predictor of a future recession, which is why you’re seeing all kinds of headlines on the news that a recession is coming. However, one thing to note is that while it is a good predictor of a recession occurring, sometime in the future, it is not a good predictor of when it will actually occur. This chart shows the last four yield curve inversions, which is the two year Treasury versus the 10 year Treasury. So the two to 10 year yield curve inversion, the dates are shown in the first column. Second column is how many months went by after the inversion, before the stock market peaked. When the stock market peaked after the inversion is the third column. And then, in the last column, it’s the return of the S&P 500 index over that time.

So you can see that this is not something that is set in stone. The number of months between when the yield curve inverted and the stock market peak varied by quite a bit each time. And that last one, the 2019 inversion, the bull market peaked February 19th, 2020, that was really precipitated by a global health crisis, a pandemic. And so that one’s a little bit difficult to even take into consideration here because it was an exogenous shock. But if you take the average of the last four occurrences anyway, the stock market continued trending up for another 17 months with an average return of 28.8% after the yield curve inverted. So while a two to 10 year yield curve inversion has a tendency to predict a recession.

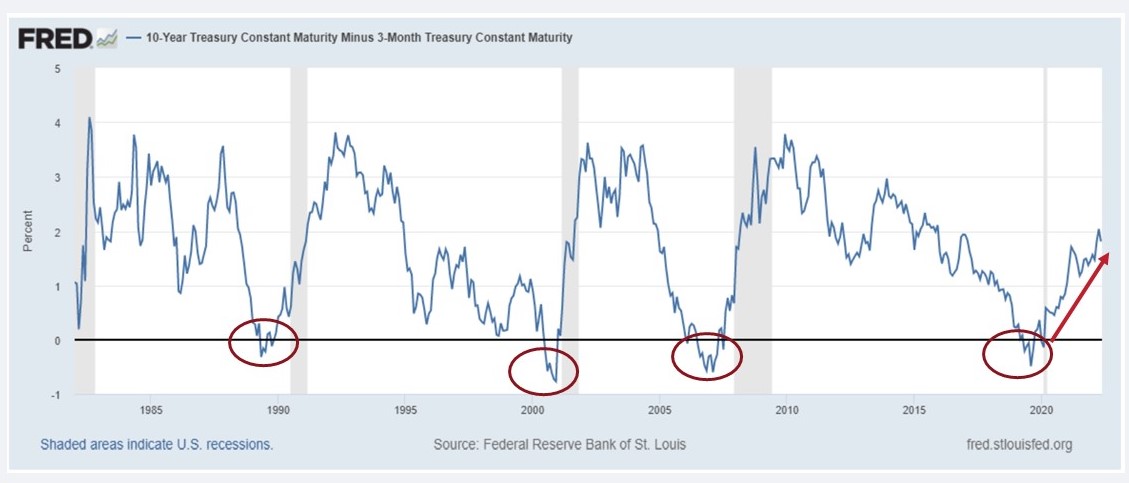

So that part is true. And what you’re seeing on the news, it doesn’t mean that a recession is imminent. We prefer to look at the three month to 10 year yield curve, which is a different yield curve because it’s more of an indicator of the Federal Reserve’s policy. Remember the Federal Reserve sets the interest rate policy for the United States and because that’s actual actually being set by the Fed this tends to be a better predictor of a recession. You can see on this chart that this indicator, the three month to 10 year has inverted prior to each of the last four recessions.

So, whenever you see that red circle there right before the gray bar, the gray bar indicates a recession. You can see that this thing has inverted prior to each of the last four recessions, but note that currently this indicator is not signaling a recession at all. In fact it has steepened. It has done the opposite of what we would expect to see if a recession were imminent. Okay. So what if I’m wrong on this? Well, it’s also important to think about, even if we do get a recession, so even if I’m wrong and this happens anyway, how bad will it be? Well, the textbook definition of recession is a decline in GDP for two consecutive quarters, but what does that actually mean for you as a consumer or as an investor? I always like this quote from Ronald Reagan, “a recession is when your neighbor loses his job, a depression is when you lose yours and a recovery is when Jimmy Carter loses his.”

So, if you’re thinking about a recession in terms of how bad will it be in the jobs market, will I lose my job? Will I lose my income? (And that’s how a lot of consumers frame a recession in their minds.) I don’t think you really have that much to worry about at this juncture. So right now the labor market is extremely tight. The unemployment rate showed in gray here is down to 3.6%, which is about where it was prior to the pandemic. The average unemployment rate in the U.S. historically is about 6.2. So we’re about half of our average historic unemployment rate. So we’re doing really well on the jobs front. The Fed did well with the low interest rates in terms of bringing down the unemployment rate, their dual mandate is to keep the economy strong through jobs and also keep prices in check, keep inflation in check. So while inflation has not been going according to their plan, the labor markets are very, very strong.

The number of job openings is near record highs. In the first quarter, there were 5 million more jobs available than unemployed people in the United States. Okay. So that keeps the labor market very tight and it’s difficult for the economy that is so based on consumer spending to go completely bust. Whenever jobs are plentiful enough that if someone needs to make extra cash to make ends meet, it is very, very easy today to get out there and to find a new job. Okay. So that gives you a few ideas of our thoughts on if there’s going to be a recession or not.

Should I sell out of bonds?

Next topic has been, bonds have had a very, very tough year. Should I be selling out, reallocating my account? Well, I’m going to keep this answer short and to the point, every position that we have in the portfolios is there for a particular reason.

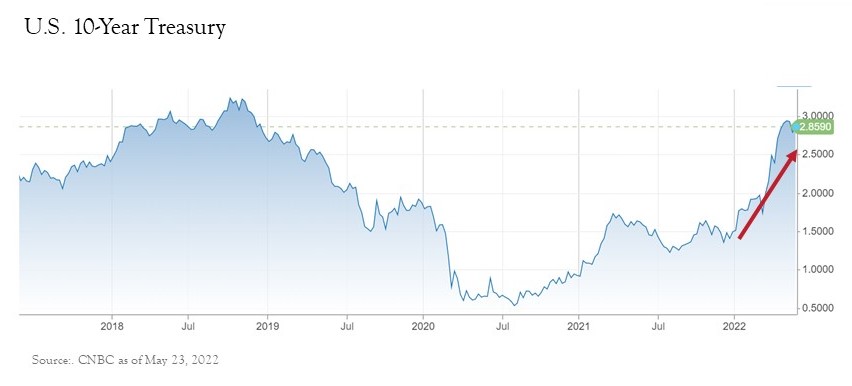

So while it’s true, that it has been a very tough year for bonds so far, the toughest start to the year ever with some bond asset classes down nine to 11%. It’s important to note that the bond market has already priced in about a full year’s worth of interest rate increases by the Federal Reserve. The chart here shows the 10 year Treasury, which has been hovering around the 3% mark lately.

And as you can see, it’s been a very strong move upward in yield. And whenever you have swift moves upward in interest rates, bonds do fall in price. So you’re seeing some of the bonds down a lot more than expected year to date. Okay. But my opinion is that a lot of the interest rate increases that are projected to occur over the next year are already priced into the bond market. Additionally, it’s important to note that we are active managers.

We positioned the portfolios for a rise in interest rates last year, and we’ve weathered the storm quite well in our portfolios. There is also a silver lining here in that it also means that when bonds come due, the proceeds can be reinvested at higher interest rates, which is beneficial for investors with a long time horizon. Over the long run, this is a chart from Loomis Sayles and Company, over the long run the total returns of bonds depends far more on their income than on the changes in price. Since 1956, just over 90% of the average annual return of the U.S. Bond market has come from interest in reinvesting it. So as a bond investor, you’ve had the price declines in your accounts from the increase of interest rates, that is true, but we need to wait for the income to now come in to offset some of those price declines, because historically about 90% of your return comes from those interest payments.

So we really just need to give the bond market some time to recover and, and try not to fall prey to recency bias here. Recency bias is when we believe that the more recent results are indicative of the future. For example, you may think that because bonds are down this year, they’re likely to continue losing value. And that’s a very backwards looking approach to investing. If most of the return on a bond investment comes from interest income, selling out the asset class now when the potential income stream is finally being reset higher after years of low rates, is just not a prudent move at this juncture.

Are we nearing the bottom of the market decline?

And probably the most common question I’m receiving: Are we near the bottom? Is the bleeding going to stop soon? Well, in my opinion, the market is trying to find a bottom. Currently, we’re just shy of a 20% drop in the S&P 500 index. We did hit a 20% drop intraday a few days ago, but from a historical perspective, you should expect this to occur from time to time; to put this in the context, a decline of 10% tends to happen once per year, a decline of 15% or more tends to happen on average once every two years and a decline of 20% or more happens on average every three years, this is a normal part of investing. The fact of the matter is that good investing often feels lousy. It involves contrarian thinking as Warren Buffet put it, “We need to be greedy when others are fearful and fearful when others are greedy.”

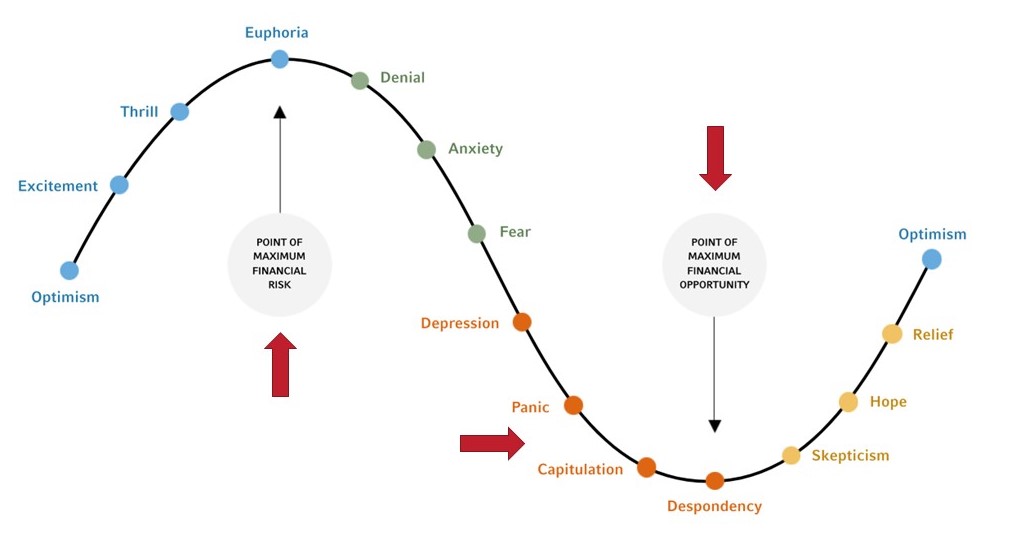

This is what we call shown here, that the chart is the behavioral life cycle. When it comes to investing, humans are emotional and we have a tendency to chase returns after the market has run up, which is actually when you should be fearful of the market. That’s the point of maximum financial risk. And we have the tendency to want to go to cash and change our risk tolerances to be more conservative whenever the markets are down, which is when you should be depositing more into your account in order to buy in at lower prices. Where are we right now in the cycle? I’d say we’re somewhere between panic and capitulation. And that’s just my opinion, but why do I say that? It’s because, well, I look at a lot of research on consumer sentiment or how investors are feeling about the market and investor sentiment, which is a measure of the feeling and the thought process for how long the sell off’s going to continue is very washed out.

Meaning that investors, many, many investors have a very negative view of the markets going forward and that’s action indicator that markets are trying to bottom. Okay. So when I start receiving calls from clients that they want to go to cash, or they want to become more conservative in their portfolio, it’s usually an indication the markets are trying to bottom because again, people get fearful when there is a lot of uncertainty about the future, when they’re losing money. And that’s usually when everyone is going to sell, goes to the market and they sell out. Once you have all these people who are going to sell, who can’t take it anymore, we call it capitulation when, whenever they say, okay, I can’t take it anymore. I’m throwing in a towel. Once you have those investors out of the market, the market tends to find a bottom and then it starts to go back up again.

And so, while it has been a challenging year for both the stock and bond markets, I just hope this helped you to, to see our thought process a bit. We do believe that the portfolios are well positioned based on our economic outlook. I know that there’s a lot of scary headlines out there today. But when you stop and take a look at the data, I do think that some of them are more fearmongering than what’s actually happening in the markets. So I hope this was helpful for you. We thank you for your continued confidence and as always, please reach out to us with any questions that you may have.

Would you like to continue the conversation about the great opportunities in the market and our investing strategies that preserve your values while managing your investments?

Do you know what Business Practices You Are Supporting through your Current Investments?

Or Contact Us to Schedule a Phone Call or Meeting.

Call us today! (540) 345-3891