June 2025 Market Commentary

Hillary Sunderland, CFA®, CKA® and Jake Preston, CFP®, CKA® discuss the second quarter of 2025 including economic commentary, quarterly returns information, One Big Beautiful Bill impact, and More!

Transcript

Jake Preston: Hey, everyone! I am Jake Preston, the Director of Financial Planning here at Beacon Wealth, and I am joined by our Chief Investment Officer, Hilary Sunderland, Hillary. It’s great to be with you.

Hillary Sunderland: Great to be with you, Jake.

Jake Preston: And we are looking forward to providing a bit of a recap of what has happened in the markets over the last quarter, as well as giving you some insight as to what we expect will occur throughout the rest of the year. And so to start, Hillary, can you just give us a recap. It’s been an exciting exciting might not be the right word, but it’s been an exciting last quarter. There’s been lots of things happening. Can you give us a little bit of a recap of the previous quarter?

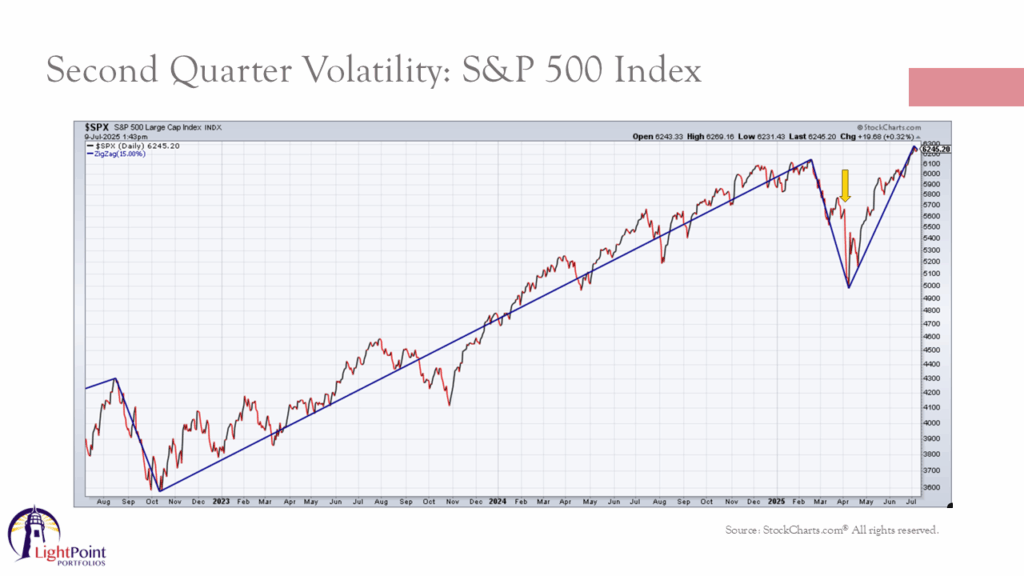

Hillary Sunderland: Yeah, I certainly can, Jake. So the second quarter was really anything but calm. Coming into the quarter. The stock market was already on a little bit of a decline, and then, on April second, right after quarter end, President Trump announced a sweeping tariff plan which sent markets into a tailspin. The yellow error on this chart shows the drop that began just 2 days into the second quarter. The S&P 500 index ended up losing about 12% of its value over just a few days.

Then, a week later, after the financial markets had panicked and the bond market was showing signs of distress. The Administration paused most of the tariffs just as they were about to take effect, which helped the markets reverse course and touched off a 9% rally in a single day.

The dark blue zigzags on this chart show moves of at least 15% from a recent high or low, and I think, really help illustrate how big of a move it was in the second quarter. In comparison to the last few years we had not seen a decline of this magnitude since late 2022 following that big drop we had a very sharp rebound, and the S&P 500 plowed through many other headlines that you would expect to move the markets. But but they really didn’t.

Such as we had a downgrade in the credit rating of us sovereign debt due to our ballooning deficits and interest costs, and there was a lot of geopolitical conflict in the Middle East with Israel initiating strikes on Iran, and then the Us. Conducting strikes on Iran’s nuclear facility. So overall, there were a lot of really big headlines to sort through, and one might expect to see poor returns in that type of market environment. But that was not the case. We ended the quarter with the S&P 500, hitting new all time highs driven by robust corporate earnings, resilient economic data and some investor optimism.

Jake Preston: Yeah. It was a lot of whiplash in the previous quarter, from things way down to things back up. I think it underscores the importance of ensuring that you have a long term plan and not making investment decisions based on the days or the week’s headlines. So appreciate that. So can you give us a rundown, an overview of what the returns of the main asset classes were for the 1st half of 2025.

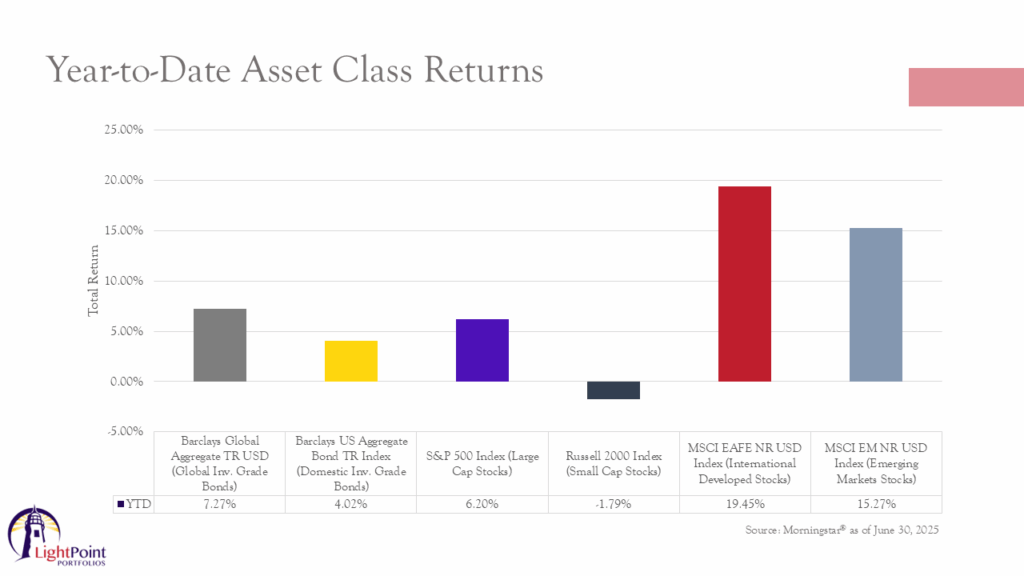

Hillary Sunderland: Sure. Well, you know, it’s been an interesting 1st half coming into the year. I remember talking about our projected returns for fixed income. Given that we believe that the increasing interest rate environment was likely behind us, and we thought that we would see decent returns from the asset class once again. And that has occurred so far this year. In the 1st half. You can see here that global investment grade bonds returned 7.2 7%, while domestic bonds, which is the yellow bar there returned just over 4%. The S&P 500 index. As I just spoke about it, ended up, rising a little bit more than bonds in the 1st half, returning 6.2, but it had substantially more volatility as we just discussed small caps had a rough start to the year with a decline of 1 79, and then international developed and emerging markets had a very strong 1st half, international developed markets, outpaced domestic stocks by over 13% and emerging markets outperformed by over 9%. I think that really shows the importance of global diversification. You know we’re coming off of several years of US exceptionalism, whereby the Us. Stock market was one of the best performing asset classes in the world, and in the 1st half of this year we started to see a bit of a shift away from that theme. And the good news for our clients is that we do run globally diversified portfolios. And so our investors benefited from this trend, away from us stocks and bonds, and toward international stocks and bonds. For the 1st half of 2025.

Jake Preston: Yeah, that’s really interesting. Can you maybe speak to a little bit of the why behind? Why international stocks have performed so well in the 1st half of the year.

Hillary Sunderland: Sure international developed markets. You know, they performed well in their own right. There’s been quite a bit of stimulus in Europe, especially as it relates to shoring up the defense industry in the eurozone. Inflation is largely under control there, and that has allowed central banks in Europe to reduce interest rates which has helped the economy there as well. Additionally, international stocks have been trading at attractive valuations relative to domestic stocks for a few years, and so there was a bit more of a runway there in terms of catching up to their true value. But the other thing that was really beneficial to us, based investors in foreign markets was the drop in the value of the US Dollar. So the value of the US Dollar fell by almost 11% in the 1st half of 2025, and that is the steepest decline since 1973, which marked the collapse of the Bretton Woods exchange rate system under President Nixon, and the drop really reflects uncertainty over President Trump’s trade and tariff agenda.

And what happens? Jake, is when the value of the US Dollar declines versus foreign currencies you benefit if you’re invested in those foreign currencies, because those returns earned abroad have to be translated back into US Dollars, so as such investors receive an additional return component and this is one of the reasons why we maintain globally diversified portfolios for our clients. There are periods of time, such as seasons of currency, fluctuations where the US Dollar gets devalued that can really benefit us, based investors.

Jake Preston: That’s a really important point, that global diversification. I also think it emphasized the importance of having a team that is managing your portfolio and helping you make these decisions and craft a portfolio that is well diversified and helps to mitigate some of the risk in terms of as opposed to something more concentrated from a portfolio perspective. So that’s really fascinating.

Let’s shift gears a little bit and talk about the one big, beautiful bill act that was passed just last week and signed into law by President Trump. Can you talk about any investment implications arising from the passage of this new law?

Hillary Sunderland: Yeah. So the good news is that we finally have clarity on the tax front and markets like clarity. And that’s good for investor sentiment just alone. Right? So it’s also permanent in the sense that the major provisions of the code do not sunset, which will help in the planning process when I say permanent here, I mean it’s permanent until a future Congress changes it. But there are some provisions, such as accelerated depreciation, which are big wins for business owners and some sectors of the economy do stand to benefit more than others for individuals. There are a lot of financial planning implications and opportunities to digest and take advantage of which we’ll save for another video. But from an investment perspective back to your question, Jake.

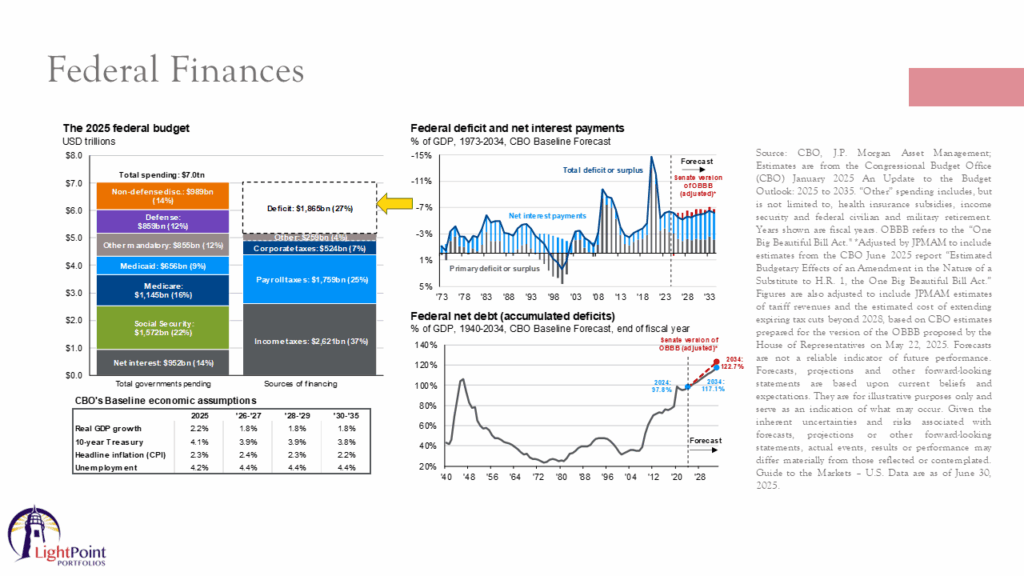

Probably one of the bigger things for investors is that the municipal bond tax exemption was preserved in the bill. That was a big question mark leading up to this, and that’s really good news for investors in high tax brackets, as whether or not they would keep the municipal bond. Tax exemption has really weighed on the municipal bond market over the last 6 months or so, I would say the big question mark on the bill is really the cost of it. This chart on the left shows the 2025 Federal budget. And note that this does include projected tariff revenue. What you can see here is that interest payments and social program obligations have increasingly crowded out other spending.

And the deficit we’re running continues to be very large as noted by that yellow arrow. There. We’ve been on a bad fiscal trajectory for some time, and unfortunately, this is continuing, and it will likely get marginally worse, as shown in the bottom right hand chart. So it’s difficult to say if or when this could lead to a debt crisis in the Us. But it’s something we’re watching closely. It’s not something that we believe will happen in the short term.

But hopefully a future Congress will be able to to shore up the the Federal budget a bit more than what we saw here from the passage of this bill.

Jake Preston: Yeah, for sure. I think. As you mentioned, there are a number of planning implications, as well, you know, making those lower tax rates permanent. There’s the permanence to the expanded estate tax exemption as well as a number of other items, and we will have both a blog and a video coming out shortly, giving a rundown of those implications that might be most relevant for the individuals and families that we serve. So thanks for giving us an overview of that. And so we are halfway through, just over halfway through 2025. Now you’ve given us a recap of what we’ve seen so far in the 1st 6 months of the year. What do you think will happen? I know we don’t have a crystal ball, but what is your expectation for what will happen in the second half of the year.

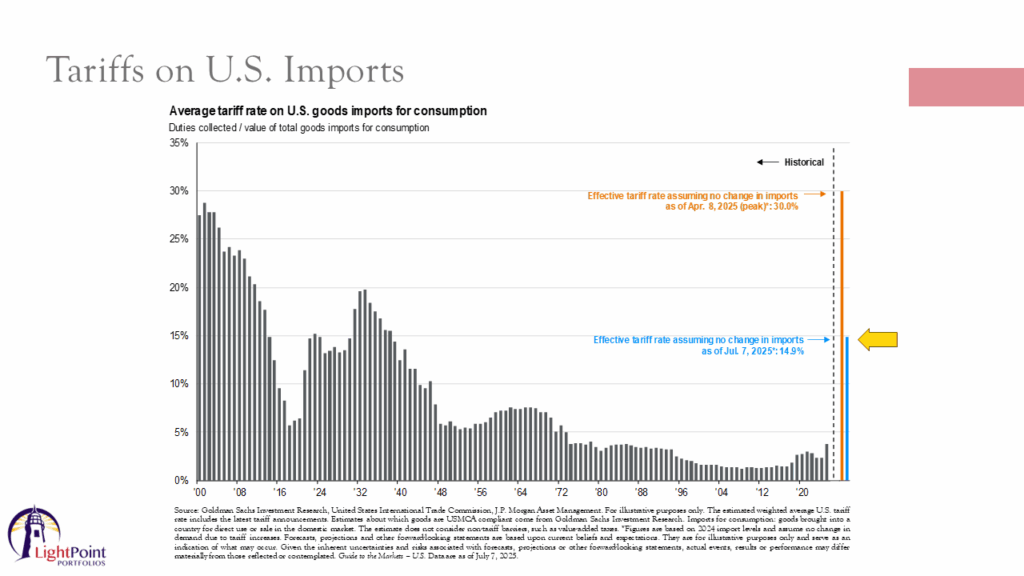

Hillary Sunderland: Yeah. Well, you know, we’ve had a very large move on the books that do need to be digested by the market. So given current stock market valuations and the uncertainty around tariffs, I do think returns will be a little more difficult to get from here. They’re probably not going to be as swift as what we’ve seen over the last 6 months. You know much of what happens from here has to do with what tariffs are implemented, and when, because that could have a really big impact on businesses and the consumer, this chart shows the effective tariff rate in orange.

After the announcement in April, on Liberation Day, as I stated earlier, President Trump paused. The implementation of this tariff plan for 90 days, effectively giving countries a 90 day negotiating window for a new tariff plan. However, as the end of the quarter approached, it was clear that very few countries would have deals by the July 9th deadline. As of June 30th only United Kingdom and Vietnam had reached a deal by the end of the quarter. So now we have to estimate what the effective tariff rate will be, and our current estimate is about 15%, which is shown by that blue bar there. Now, this is much lower than what it was just 3 months ago, but it’s still very substantial relative to history. We have not had tariff rates this high since the 1940s and there are still many more tariff rate announcements yet to come. Just this week 25% tariffs were announced on Japan and South Korea with much higher rates for other nations, such as 50% for Brazil. And these tariffs have to be eaten by someone, either by businesses or by the consumer. So if the business absorbs the tariff it reduces profit margins, and hence future earnings. And that’s a problem. Because when you invest in the stock market, that’s what you’re buying, you’re buying a stream of future earnings.

Businesses, you know. They can’t just move their supply chains overnight or their manufacturing operations overnight. These things often take years to sort out, and so we do think some of that cost will be borne by businesses. But it’s going to take many years for them to maybe reshore some of their operations. That’s ultimately what they want to do. If the cost is passed on to consumers, there’s going to be less consumer spending overall because it’s going to hit everyone’s wallets. And this will cause the economy to slow because consumer spending accounts for about 2 thirds of domestic economic growth. Right now, estimates are that about 60% of the cost of the tariffs will be passed on to consumers.

And just because we haven’t seen tariffs show up in the inflation reports. Yet it doesn’t mean that we won’t remember that the larger tariffs were paused 3 months ago and tariffs take a while to work their way through the system to the consumer and is a lagging effect. Many companies build up substantial excess inventories ahead of the April tariff announcements, so I don’t think the tariffs have really been incorporated into the inflation data just yet. We’re likely going to see some price increases over the course of the next few months and inflation is likely to tick up. Because of that, we think probably to 3%, or maybe even to 3.2 to 3.5% really depends on the amount of the tariffs that are actually enacted and which sectors they’re enacted on. At the same time, though, the passage of the big, beautiful bill will stimulate the economy over the next few months. It was a retroactive tax break that was applied that is stimulative for the economy. And so the good thing out of that is that while it does increase our issues in terms of our debt, long term in the short term.

The passage of that act, and the retroactive tax cuts does reduce the probability of recession over the short term. So what we’re really forecasting here is for the economy a little bit of a heating up because of those stimulus of tax breaks. But then, as those tariffs start to kick in, we do think you’ll see a bit of a slowdown in the months ahead.

Jake Preston: Well, thanks so much, Hilary. There’s certainly a lot to navigate a lot to think through in the second half of this year, and I know for myself personally, as an advisor, I’m extremely grateful to have Hillary and her team helping us walk through all of these challenging issues and helping to make investment decisions that are in the best interest of our clients. I think all of this really underscores and emphasizes the importance of having a long term plan both a financial plan and a plan for your investments that reflect your values. And so we are honored to be able to walk alongside our clients in that long term plan. If you have additional questions that arose as a result of this market commentary, please feel free to reach out to us, we’d be happy to answer those for you. Thanks again, Hilary, and we look forward to doing it again next time.

Hillary Sunderland: Thanks. Jake.

Sign up for our newsletter!

Get news, market commentaries, videos, and faith-based investing articles from Beacon Wealth Consultants in your inbox.