A Sideways Performance

A Sideways Performance

The biggest theme of the first quarter was the return of volatility as equity investors experienced a much bumpier ride than what they’ve become accustomed to over the last year. In 2017, there were zero days of +/- 2% moves in the S&P 500 Index. However, over the past three months, investors endured six trading days of +/- 2% moves.

Several themes led to the increase in volatility. As discussed in our March 24th Special Market Update, the deepening rift between China and the U.S. sent a chill through financial markets given the negative global economic consequences that are likely to result from a trade war. In addition, news of Facebook’s massive data breach and President Trump’s continued tweets concerning Amazon’s tax status and its use of the U.S. Postal Service sent technology stocks reeling in March. Declines in Facebook, Apple, Amazon, Netflix, and Google, collectively referred to as the FAANG stocks, have an outsized effect on the performance of the S&P 500 Index given that, together, these five stocks comprise more than 11% of the Index. Trouble in Silicon Valley leads to trouble for index investors due to this concentration risk, which is yet another reason why we believe in active management. Because technology stocks comprise about 25% of the S&P 500 Index, the broad market index will likely continue to struggle if tech continues to come under pressure. However, active managers will be able to underweight the sector as appropriate.

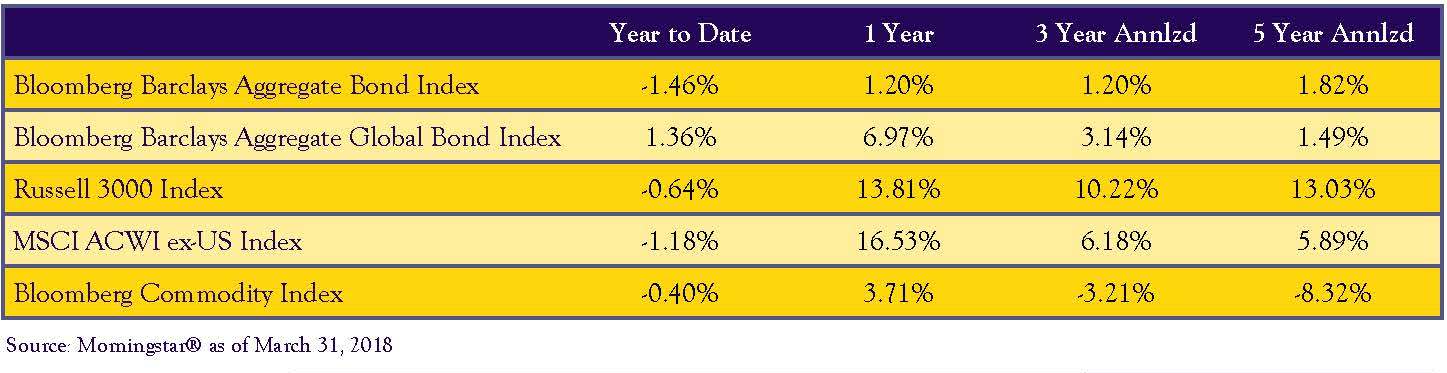

As shown on the chart above, while the first quarter was a bit of a roller coaster, the end result wasn’t as bad as it may have felt. The S&P 500 Index lost only -0.76% for the quarter. Domestic small cap stocks outperformed large cap, while growth stocks continued to lead value. Looking abroad, the MSCI ACWI ex-US Index, a measure of foreign developed and emerging markets stocks, lost -1.18%.

Among the worst performers for the quarter were real estate investment trusts (REITs) and master limited partnerships (MLPs). The FTSE NAREIT All Equity REIT Total Return Index lost -6.66% on rising interest rates and slim earnings growth rates. The Alerian MLP Total Return Index declined -11.12% year-to-date after the Federal Energy Regulatory Commission (FERC) ruled on March 15th that they would no longer allow interstate natural gas and oil pipeline MLPs to recover an income-tax allowance in their cost of service rates. While the tax ruling will materially impact only a small segment of the MLP asset class, a broad selloff occurred. We believe the selloff in MLPs was overdone based on current valuations.

One would expect bonds to perform well during the first quarter given the decline in the stock market, but this was not the case. Ten-year Treasury yields only managed to drop 0.03% (bond yields move inversely to price) the same week that the Dow Jones Industrial Average tumbled more than 1,400 points, which was its worst decline in two years. The meager backup in yields provided little protection to diversified investors. On the whole, the Barclays Aggregate Bond Index declined -1.46% for the quarter – marking only the eighth time in the last 30 years that both the S&P 500 and the Barclays Aggregate Bond Index had a negative total return in the same quarter. Bonds came under pressure on steadily rising interest rates after the Federal Reserve raised interest rates for the fifth time in the last 15 months and signaled two more rate increases are on the way by the end of the year. The central bank also boosted by one the number of rate hikes it expects in 2019 and 2020. Given already tight credit spreads and the rising rate environment, we expect bonds to continue to offer low returns over the short-term and may not provide the ballast investors have come to expect during stock market selloffs.

Looking ahead, we retain our conviction in the base case of steady global growth and caution against reacting to negatively to protectionist rhetoric. While we are once again experiencing a strong bout of volatility on the first trading day of the second quarter, we are not surprised by the current retesting of the stock market’s mid-February lows. Corrections (defined as a drop of 10% – 20% from a recent high) usually take place in three waves: the first leg down, a recovery, and then a retest of the prior low. This retest is very much expected, and while we need a few more days to tell, this could be a normal correction within a longer-term uptrend. While swift moves in the market can be unnerving to investors – especially after a year of historic calm in the markets – one must remember that volatility causes securities to dislocate from their true values, which creates opportunities for active investors like ourselves. In the words of Robert Arnott, one of the world’s most respected financial analysts, “In investing, what is comfortable is rarely profitable.”

Thank you for your continued confidence. As always, please reach out to us with any questions you may have.

-Hillary Sunderland, CFA

Chief Investment Officer

3 RISKS TO THE RALLY

1) CREDIT SPREADS

The limited spread-tightening potential of corporate bonds combined with interest rates near historic lows could lead to increased volatility in the bond market as the Federal Reserve tightens rates. Leverage in credit has increased, and the economic cycle is approaching the point when credit spreads have historically started to turn.

2) EARNINGS GROWTH

Earnings growth beyond 2018 is likely to slow because of higher interest costs and higher wage costs.

3) GEOPOLITICAL

Continued trade tensions with China could disrupt supply chains for domestic companies and lead to accelerating inflation in the U.S. Higher inflation could encourage the Federal Reserve to raise interest rates more quickly than anticipated, which would likely slow the U.S. economy.

Economic Backdrop

GROWTH

For the fourth quarter of 2017, economic growth was revised upward to 2.9%. The lagged effect of favorable financial conditions and the coming financial stimulus in the U.S. keeps overall recession risk low for 2018.

EMPLOYMENT

In February, the unemployment rate stayed flat at 4.1%, while the labor force participation rate (the number of people who are employed or who are actively looking for work) registered a reading of 63.0%, which is near its long-term average. Average weekly jobless claims dropped in February, which is a positive for the economy. As more workers remain employed, their spending power increases, which drives aggregate demand in the economy.

INFLATION & INTEREST RATES

We are starting to see signs of gradually firming inflation, which is in line with the Federal Reserve’s expectation that inflation should gradually move upward toward its 2% target this year. In February, U.S. core inflation (inflation less food and energy) was 1.8% year-over-year, while headline CPI was up slightly to 2.2%. A synchronized rise in global inflation expectations is fueling higher bond yields and creating a headwind for fixed income investors.

In a much-forecasted move, the Federal Reserve hiked interest rates by 0.25% in March to a range of 1.50% to 1.75%. The Federal Reserve’s projections indicate three additional rate hikes in 2018 while boosting the number of rate hikes in 2019 from two to three. Given that the Fed is also running down its balance sheet at an accelerating pace this year, the days of easy monetary policy and suppressed volatility are likely coming to an end.

Index Returns

Disclosures

Financial Planning and Investment Advisory Services offered through Beacon Wealth Consultants, Inc., a Registered Investment Advisor.

The material has been prepared for informational purposes only and is not intended to provide, nor should it be relied upon for, accounting, legal, or tax advice. References to future returns are not promises or estimates of actual returns a client portfolio may achieve. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. Information and data referred to in this document has been compiled from various sources and has not been independently verified. We believe the information presented here to be reliable but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase of any financial instrument. The views and strategies described may not be suitable for all investors.

All returns represent total returns for the stated period. The Bloomberg Barclays Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The Bloomberg Barclays Global Aggregate Index is a flagship measure of global investment grade debt from twenty-four local currency markets. The S&P 500 Index is a market capitalization weighted and unmanaged group of securities considered to be representative of the stock market in general. The Russell 3000 Index is a market capitalization weighted index that measures the performance of the largest 3,000 companies representing approximately 98% of the investable U.S. equity market. The Russell 2000 Index is a market capitalization weighted index that measures the performance of the smallest 2,000 companies in the Russell 3000 Index. The MSCI ACWI ex-US Index is a market capitalization weighted index designed to provide a broad measure of equity market performance throughout the world and is comprised of stocks from both developed and emerging markets outside of the U.S. The Bloomberg Commodity Index is designed to be a highly liquid and diversified benchmark for commodity investments.

Past performance is not indicative of future results. Diversification does not guarantee investment returns and does not eliminate the risk of loss. You cannot invest directly in an index.