Many investors are happy to see 2022 in the rear-view mirror. As we begin this new year, what might we expect from 2023?

In our December 2022 market commentary, Beacon Wealth Consultants’ Chief Investment Officer Hillary Sunderland, CFA®, CKA® looks back at how we finished 2022 and looks forward with our initial views for 2023.

Watch our video to learn more!

If you have any questions about your financial situation, please reach out to your wealth advisor and we would be glad to address them for you. Thank you for being a valued client of ours.

Full transcript below.

Transcript

Hi, my name is Hillary Sunderland and I’m the Chief Investment Officer of Beacon Wealth Consultants and LightPoint Portfolios. This is your December 2022 market update.

Well, before I get into our outlook for 2023, I wanted to do a quick recap of asset class returns for 2022. Last year, persistently high inflation, heightened geopolitical tensions, rising interest rates, as well as recessionary fears, caused almost every asset class to sell off. This chart is organized by the best asset class performance to the worst for 2022. And you can see immediately that the only major asset class with a positive return was commodities, which soared on rising agricultural and energy prices in the wake of the invasion of Ukraine.

Domestic investment grade fixed income declined about 13%, which was its worst annual decline on record and by a long shot since its inception in 1976 and even after a very strong fourth quarter rally, international developed markets end of the year down 14.45%.

Global investment grade bonds slumped by 16.25%, as negative yielding debt, heading into a rising interest rate environment, caused hefty losses for investors. Domestic large cap stocks as measured by the S&P 500 index fell 18.11% and emerging markets and small cap domestic stocks declined by just over 20%.

Now you may be thinking, “I just can’t take this anymore. This isn’t going to get any better.” And a statement like that wouldn’t surprise me because people often exhibit what’s called recency bias or the incorrect belief that recent events will occur again soon.

So I wanted to take shark attacks for an example. Shark attacks, especially deadly ones, are extremely rare. For example, in 2021, there were only 73 reported shark attacks worldwide, which is about the yearly average. Nevertheless, after a news report of a shark attack, fewer people swim in the ocean believing that the odds of being attacked by a shark are greater than they actually are.

For investors, recency bias makes people expect that recent events or headlines are going to be more frequent than they actually are, and this tendency is irrational because it obscures the true probability of events occurring. So I wanted to take some time today to add some context to the negative returns of 2022.

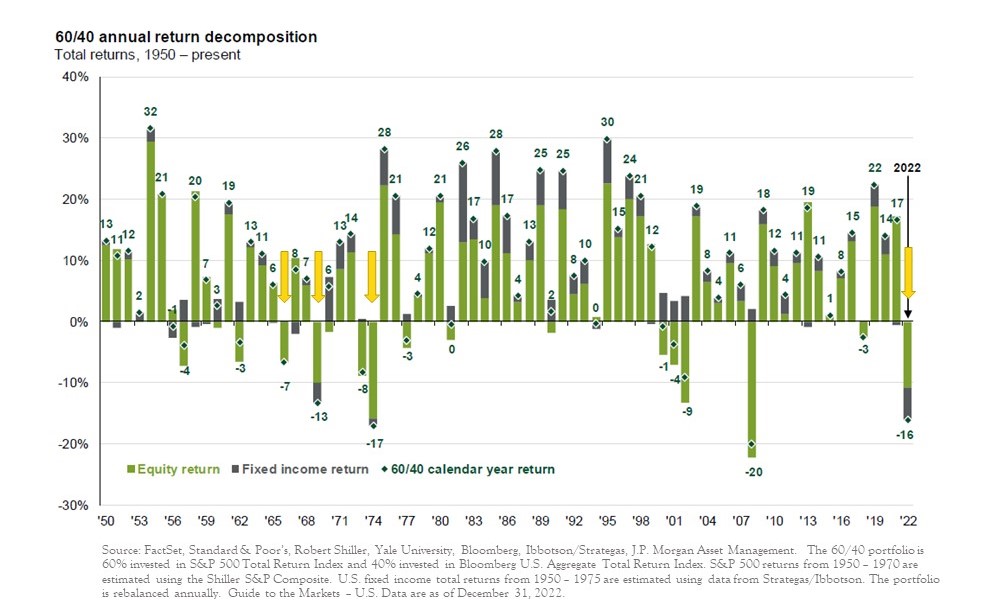

The green bars here show the return of domestic large cap stocks, and the gray bars show the return of US investment grade bonds for each calendar year since 1950. And the diamonds on the chart show the calendar return for a blend of 60% stocks and 40% bonds. So to make this a little bit easier to read, I added some arrows here. These yellow arrows show the four instances since 1950 where both US stocks and bonds were both down in the calendar year. So over the last 72 years, this has only happened four times and a year like this where stocks and bonds sell off is very unusual.

As you can see here, it’s not the norm. What’s overwhelmingly the case is that drawdowns in equity markets are offset by some degree by gains in fixed income, but that didn’t happen in 2022 because bonds started off the year at historically low interest rate levels and the Federal Reserve raised interest rates significantly more than they forecasted.

Just to show you how far off the Fed’s forecast was at the beginning of the year versus where they ended up, I pulled these charts from the Federal Reserve website. On the left you can see a look at the Federal Reserve’s interest rate projection from December of 2021. So their median forecast was that the Fed funds rate, which is the interest rate that they control, would rise to 0.9% in calendar year 2022. However, as of the end of 2022, they actually went ahead and raised interest rates to 4.4% as the war in Ukraine exacerbated many inflationary pressures and this resulted in a massive repricing of the bond market.

So where we stand now is that the Federal Reserve has started to pare back the rate of interest rate increases, and they’re likely to begin holding rates steady sometime in the first half of 2023.

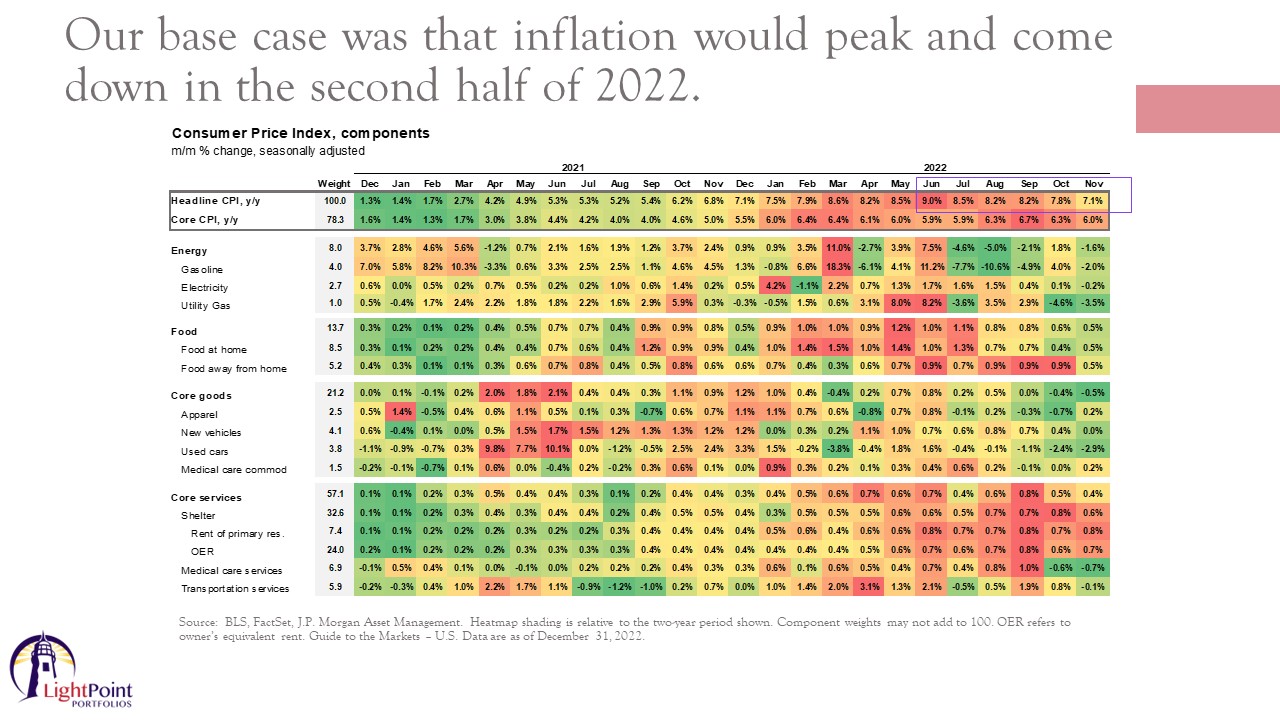

So I say all this because the only way to come to the conclusion that bonds are going to have a year in 2023 like they did in 2022, is to assume that the Fed continues to be way off base on inflation and that they will continue hiking rates at a much higher than normal pace. And we simply don’t see that in the data. You may recall that last year our base case was that inflation would peak and come down in a second half of 2022, and that is what we saw.

What I’m showing here is an inflation heat map. The red means that the inflationary level is very elevated, and as the chart turns from shades of autumn to summer, that means that inflationary pressures are easing to a normal level.

Now, a key point to remember here is that when I say inflation is easing, I’m not saying that prices are going back to where they were in 2021. That would be deflation, which is actually very bad for the economy. When I say that inflation is easing, that means that the rate of price increases is slowing.

So you can see here by that purple box that headline inflation peaked in June and has since been easing when you look at the underlying components of inflation from left to right, so energy, food, core goods and services with the exception of shelter, many of these areas are back to green, which is what we want to see.

Toward the bottom, the shelter inflation remains elevated, but this reflects rent increases from the pandemic with a significant lag. So we expect that that will be cooling down here shortly. And then the remaining problem for inflation is tightness in the labor market and numbers out late last week showed encouraging signs that wages are growing slower than anticipated.

So all things considered, we believe the risk that the Fed continues with these massive rate hikes is very low, and at the bond market has already priced in the next few months of smaller interest rate hikes from the Fed. And this means that the bond market should stabilize. And right now bonds are offering more compelling valuations than they have for the better part of a decade. And if you believe that a recession is going to happen in 2023, owning bonds is likely to be beneficial as the usual negative correlation between stocks and bonds is likely to return in 2023, which should help cushion stock market weakness.

So quickly onto the stock market, the black and red lines here show the movement of the S&P 500 index and the purple overlay denotes a move of at least 5% higher or lower. And you can see here that we have had a tremendous amount of volatility, especially in comparison to the steady ascent we experienced in 2021.

Stocks have been stuck in a bit of a trading range since beginning the summer. As investors think through how much earnings will be hit by a recession.

At this point, I’ll say that recession is a consensus. The debate is how mild or severe it’ll be. A severe recession in my view, is not yet priced into the market, but while there are some very bearish views out there, we are not in that camp. Historically, in order for the economy to have a very deep recession like that that occurred in 2008, it requires excesses and imbalances in the system that need to be corrected. And that usually happens when companies and investors are caught off guard and are overextended. This recession is likely to be one of the most telegraphed recessions on record. Additionally, it’s difficult to expect a deep recession with such a robust labor market.

Domestic stocks could have some further challenges in the year ahead, but with inflation receding, my belief is that the worst is likely behind us. So in terms of stock market valuation or how cheap or expensive the stock market is currently relative to the stream of future earnings, domestic stocks are selling at about 16.7 times future earnings, which is shown by the blue diamond on this chart.

To interpret this means that that investors are willing to pay $16 and 70 cents for each dollar future earnings. So relative to the 25 year average, which is denoted by the purple line there, domestic stocks aren’t cheap or expensive, however, they do offer a much better valuation than they did at the start of 2022. And remember that we invest globally, as you can see here when looking across the global opportunity set. There are areas of the world that look much more compelling, especially international developed stocks, which include areas such as Japan and Europe. Those regions have valuations that are quite a bit cheaper than their historical average, and we’re taking advantage of some of those opportunities.

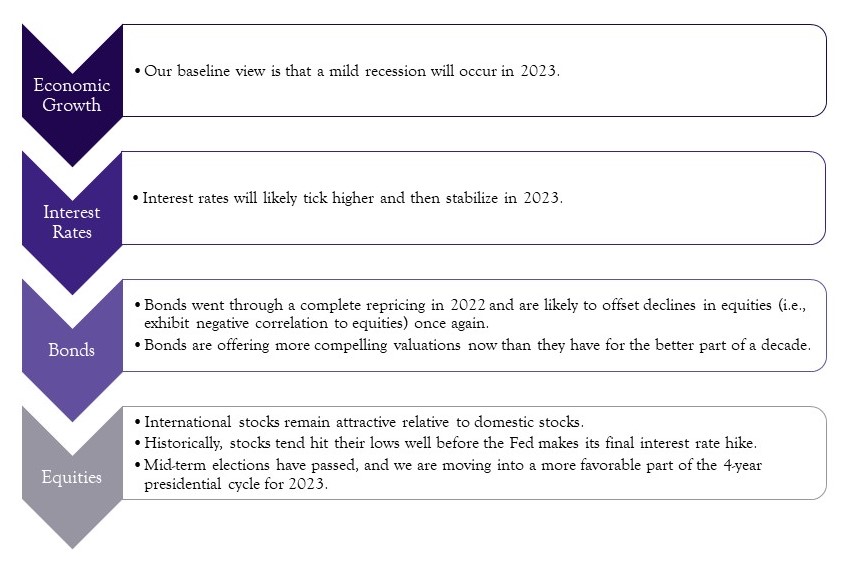

In summary, on economic growth, our baseline view is that a mild recession will occur in 2023. Interest rates are likely to tick a bit higher before stabilizing sometime later this year. Bonds went through a complete repricing in 2022, and we’re of the belief that they’re likely to start offsetting declines in equities once again because they have repriced. A lot of that interest rate move higher at this juncture, and they are now offering more compelling valuations than they have in more than a decade.

On stocks, international stocks remain very attractive relative to domestic. And while we could have some further downside in stocks, it’s important to remember that historically stocks tend to hit their lows well before the Fed makes its final interest rate hike and before a recession is even called.

And additionally, the headwind of a midterm election year has passed and we are moving into a more favorable part of the four-year presidential cycle for the first half of 2023. As always, we believe it is imperative for you to stay focused on your long-term goals and don’t let short-term swings in the market derail you from your long-term objectives. I hope you found this to be informative and I wish you a healthy and prosperous new year.

Want to talk through your financial goals for 2023 and beyond? Give us a call!

Contact Us to Schedule a Phone Call or Meeting.

Call us today! (540) 345-3891