Many of you are wondering when the market volatility and inflation will end. In our August 2022 market commentary, Beacon Wealth Consultants’ Chief Investment Officer Hillary Sunderland, CFA®, CKA® looks at several topics including:

- Year-to-date returns of different asset classes

- An update about inflation trends and recent comments by the Fed about future interest rate hikes

- How inflation is affecting bond and stock prices

- How Beacon Wealth Consultants is responding within our portfolios

We hope this update gives you more information to understand what is happening in the markets and confidence to stay the course during these trying times. Thank you for your continued confidence.

Please reach out to us with any questions or worries that you may have, it is our pleasure to walk with you through times like these.

Full transcript below.

Transcript

Hi, my name is Hillary Sunderland and I’m the Chief Investment Officer at Beacon Wealth and LightPoint™ Portfolios. And this is your August 2022 market update.

First, I want to thank you for being a valued client of ours. On a monthly basis one of the things I like to do for you is to provide you with an update about what’s going on in the markets or the economy, or maybe even sometimes offer you an update on some of the values-based investment themes in our portfolios. For this month, we’ve been getting a few client questions around the recent market volatility. So I wanted to address that for you today.

Well, I thought this picture was an appropriate one to illustrate what it has been like to be an investor this year, we’ve had to ride out waves of volatility in both the bond and the stock markets.

And honestly, some of them have made even me a little sick to my stomach, but just like when you’re on a boat and riding the waves of volatility, investors have to focus on their final destination and keep in mind that the volatility won’t last forever, even if it does feel uneasy at times.

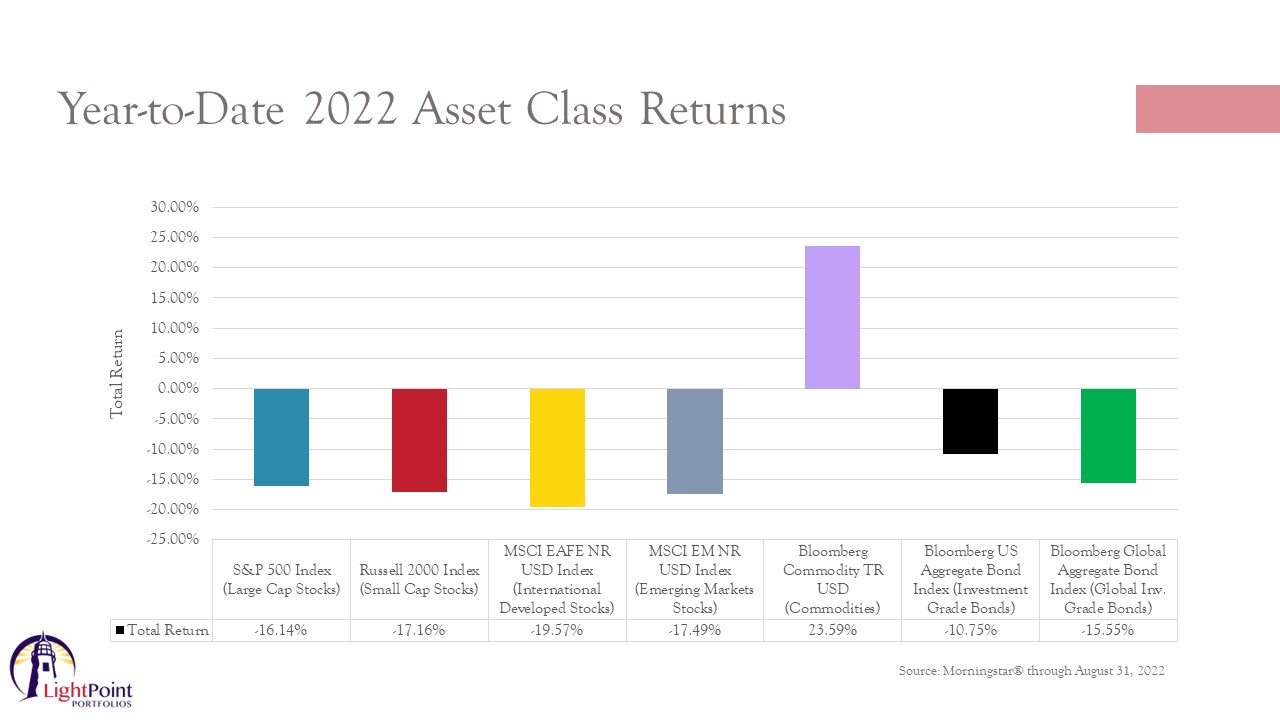

It’s been quite a difficult year for both stocks and bonds. And to frame this for you in case you haven’t been keeping up with the markets, we’re going to go from left to right across this chart.

On the equity side year to date the S&P 500 index, which is a measure of the performance of the 500 largest publicly traded stocks in the U.S. is down 16.14%. Small cap stocks are down a little more at a loss of 17.16%. International developed markets, which includes countries like France and Germany have lost 19.57%.

And emerging markets are down as well. That that includes countries such as China and India down 17.49%. The lone bright spot is the broad commodities index. The commodities index includes things like oil and wheat, which took off significantly in price after Russia’s invasion of Ukraine. Commodities are up 23.59%. And while that’s a very nice return this year, compared to the other indices listed here, still notably off its highs from earlier in the year. On the bond side of the equation, the black bar there, it’s been an extremely difficult year. Bonds have not protected in a down market for equities like they normally do given concerns around inflation, as well as rising interest rates. The broad investment grade bond index in the U.S. is down 10.75% while global investment grade bonds are down even more with a loss of 15.55%.

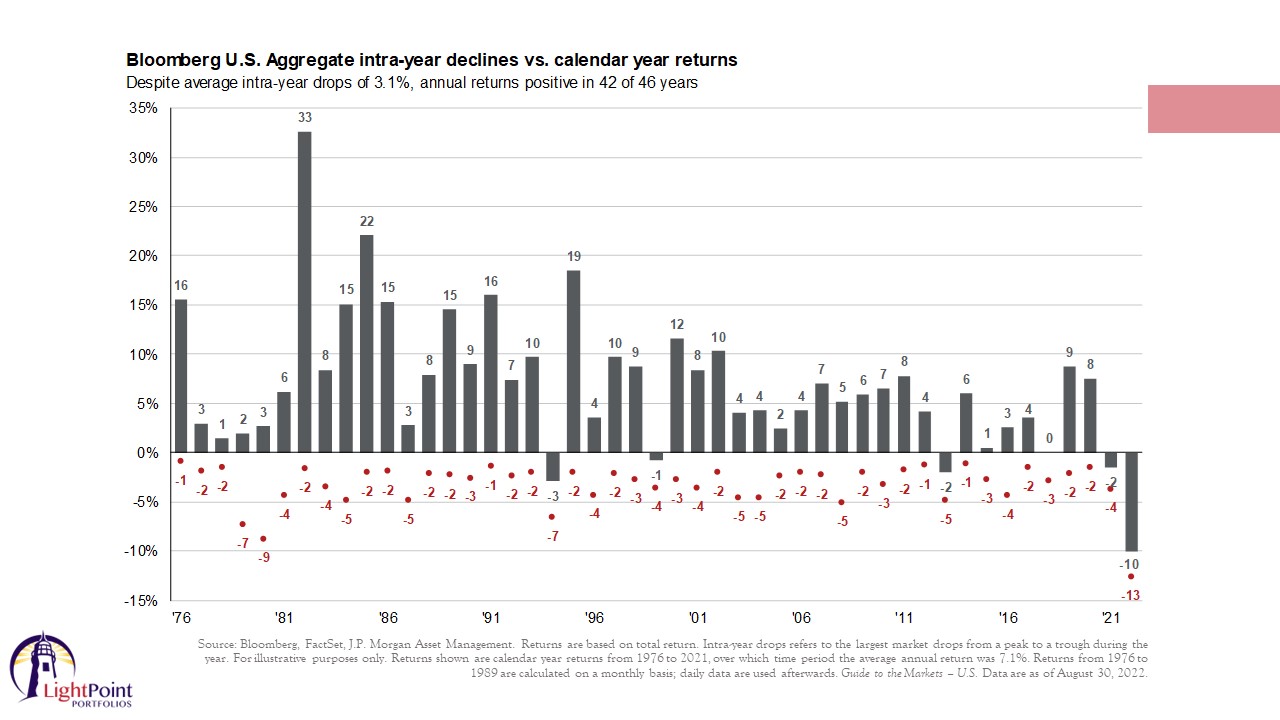

On this chart, you can see the counter year returns for the bond market in the gray bars and the red dots beneath that show the worst peak to trough decline for each year going back to the index’s inception in 1976. So despite an average intra year decline of 3.1%, the bond market has still managed to have a positive calendar year return 91% of the time. But this year we’ve had the largest peak to trough decline on record, about 13%. Now we are off those lows a bit, but the decline is still quite stunning for those who look to bonds to protect their capital. The reason why we’ve had such a decline of bonds is because we’ve had a massive repricing and interest rates across the yield curve.

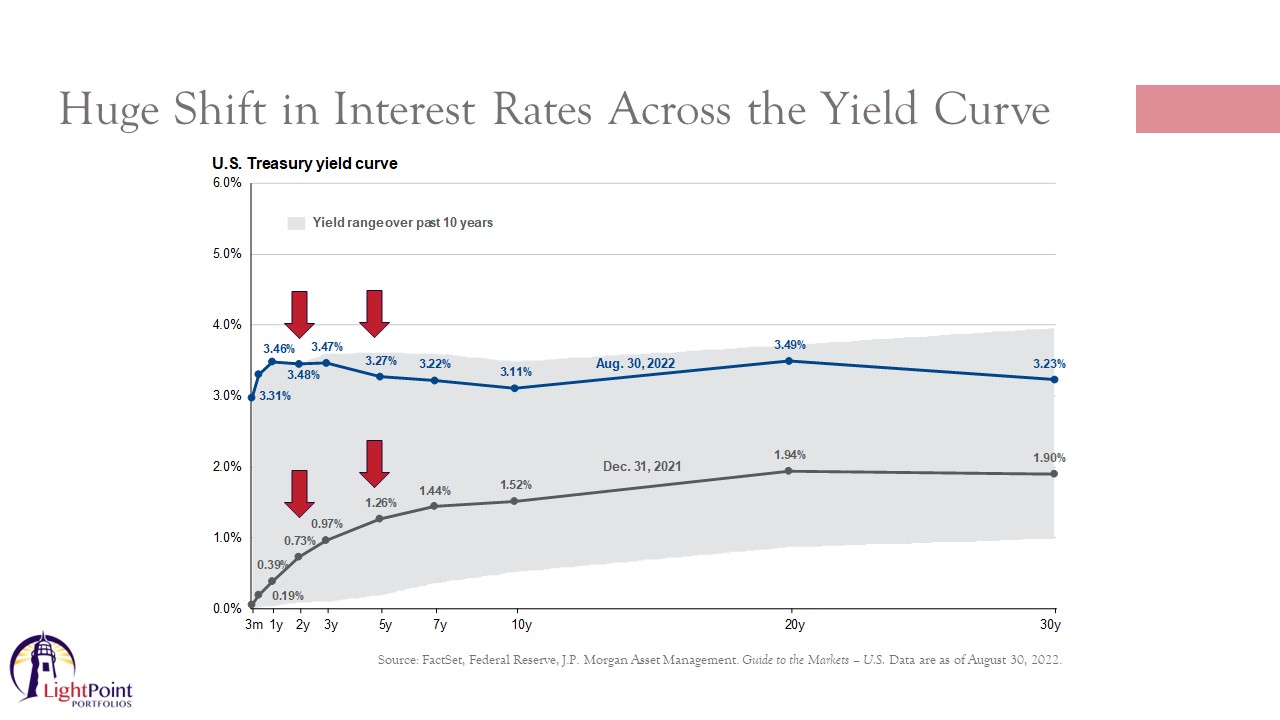

This chart shows the yield of U.S. Treasuries across different maturities and the further right you go on the chart, the longer the maturity of the bond. I want you to zone in on the dark gray line. And this is what yields were as of December 31st, 2021. A two year Treasury on that date was yielding 0.73% and a five year Treasury was yielding 1.26% and so on. So just eight months later, by looking at the dark blue line, you can see that the two year Treasury went up from 0.73% to 3.48 and the five year went from 1.26 to 3.27.

This is a massive move in bond yields. And remember as yields go up, new bonds are issued at these higher rates, which means that in order to increase competitiveness and attract investors to older already issued bonds, those bonds have to decrease in price because they were issued at a lower fixed rate to begin with. So that is why as interest rates rise, bonds decline in price. And that is why the bond market is down so much in 2022.

Now this move in interest rates didn’t only affect the bond market, it affected the stock market, as well. As interest rates rise the cost of capital for those businesses also rises, which cuts into their earnings. And if earnings are expected to decline, investors are less willing to pay up for these companies and stock prices have to come down in order to entice more buyers into the market. And that’s led to a pretty big repricing in stocks this year, as well as, as I showed you on the last slide.

So this begs the question, why have interest rates risen so much and so quickly in 2022? And the reason is that the Federal Reserve, which sets short term borrowing rates for banks has been trying to reign in inflation. As the Fed raises short term interest rates, banks pass along the higher interest rates to consumers and businesses, and as goods and services become more expensive, businesses and consumers tap the brakes on their spending. When there’s less demand chasing supply, price pressures ease.

So the big question we really have today is when is this repricing in both the bond market and the stock market going to end? Well, a lot of that has to do with our expectation around inflation and interest rates.

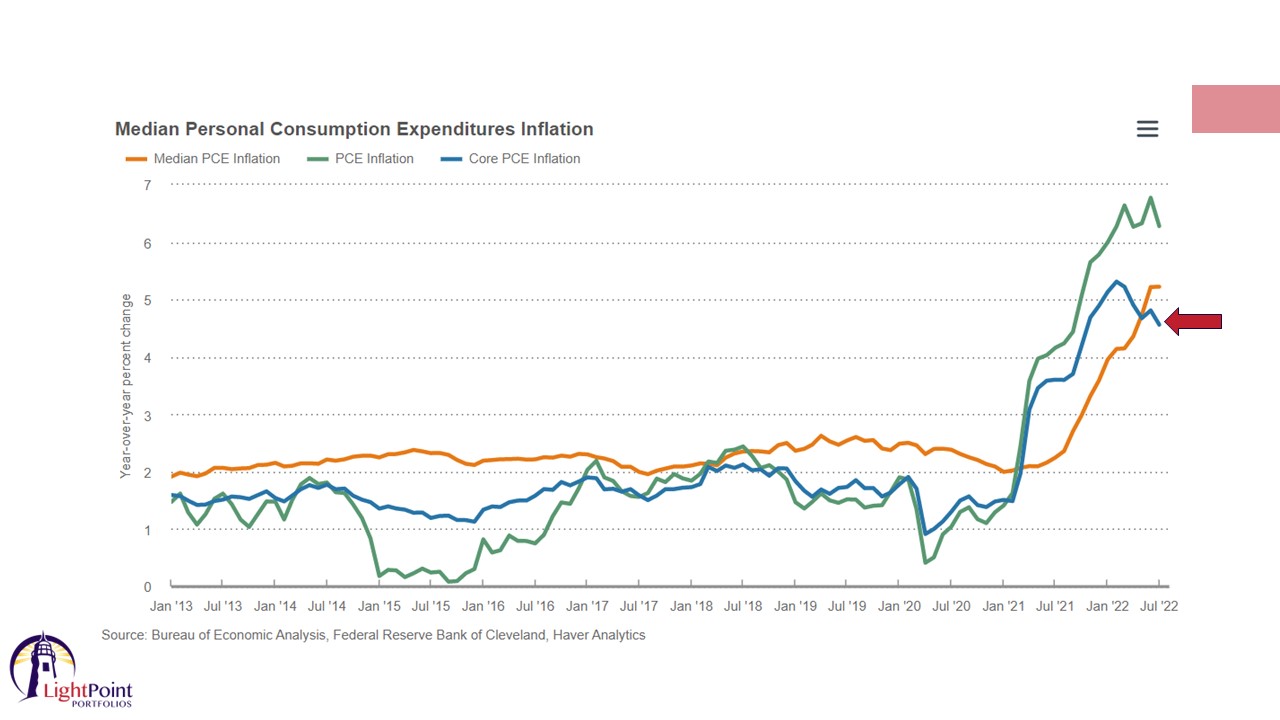

So on the inflation front, I told you earlier in the year that we expect to see inflationary pressures start to abate in the second half of 2022. And that is actually what we are seeing now a few days ago, the Federal Reserve’s preferred measure of inflation, which is the personal consumption expenditures index or PCE for short, recorded its first monthly decline in more than two years for the 12 month period that ended in July.

You can see how the dark blue line here, which is the core PCE, is rolling over. And another measure of inflation, the consumer price index, which isn’t shown here, but that one didn’t rise at all in July and additionally supply chain pressures have ease considerably.

So combined this suggests that consumer price pressures are beginning to ease as we projected would be the case. But despite these encouraging inflation reports, there was a selloff in both stock and bond markets at the end of August. Federal Reserve chair, Jerome Powell was in Jackson Hole, Wyoming for an annual meeting and during a speech that he gave, he pledged to forcefully use the Fed’s tools to bring down inflation and stated that doing so will bring some pain to households and businesses. And this strong language that he used in his speech caught many by surprise, given that the inflationary data continues to show consistent moves to the downside as shown here. So let me give you a few takeaways on what this could mean.

First, we need to consider how high is the Fed going to raise interest rates? How high are short term interest rates likely to go?

Well, the forecast right now is that the Fed will take short term interest rates up to 3.75%. To put that into context today, the Fed has interest rates pegged at 2.25% to 2.5%. And there’s no reason that the Fed won’t go up to 3.75. Even though we see inflationary pressure starting to abate, as we expected to be the case, inflation’s still pretty high relative to historical standards. So another one and a half percentage move higher likely in interest rates is still likely.

Now in terms of what is that going to do to the bond market? The good news is I believe that most of that is already priced into the markets at this point. On the chart I showed you earlier, shorter term bond rates are already higher than 3% because remember the bond market moves in anticipation of what the Federal Reserve is likely to do. So I do think that most of the pain is behind us on the bond side.

Finally, we need to consider how long the Federal Reserve will keep rates that high. And this is what’s caused a bit of a sell off in the stock market. Going into last week, the expectation was that the Fed would actually cut interest rates in 2023. Over the last week, they said that they’re likely going to keep rates near 3.75% for some time. And the cost of higher interest rates for longer is that this will slow economic growth and lead to a higher unemployment rate, which naturally is going to lead to some repricing in stocks and some short term volatility until we get a better picture of what the Federal Reserve is actually going to do here. As we get more information concerning inflation over the next couple of weeks, the Fed may change their minds on that as they seem to do often these days, but it’s more of a wait and see approach right now in terms of inflation.

So what are we doing about this? Well, to highlight a few key areas: on the bond side, we’ve been positioned for higher rates for quite some time for well over 18 months. And we did this by reducing our exposure to interest rate risk. And we also put an allocation to alternative investments within most of our portfolios. And this has really helped our more conservative investors especially, because they have a higher allocation to bonds, hedge some of the rise in the interest rates, and we are maintaining our allocation to these investments. Alternative investments are really good as diversifiers because they have a low correlation with both stocks and bond markets. And that means that they can enhance risk adjusted returns for investors because they’re offering very unique exposure to investors, such as exposures to commodities.

On the equity side of the equation we are emphasizing high quality stocks that we believe have the ability to perform relatively well in a slowing economy and stocks that we believe are positioned to capitalize on long term global trends. Remember, these are long term investments. We are looking out several years and positioning portfolios in businesses that we believe will continue to earn value for investors and also have a positive impact on the world. These are not short-term investments, and we need to wait for those investment theses to play out, which usually takes several years. And we also continue to engage in opportunistic rebalancing and tax loss harvesting for those clients that are in very high tax brackets.

I hope this update was helpful for you in providing you with some insight into what’s going on in the market, as well as in your portfolio. As always. We thank you for your continued confidence, and please reach out to us with any questions that you may have.

Would you like your investments to have a positive impact on the world? Give us a call!?

Do you know what Business Practices You Are Supporting through your Current Investments?

Or Contact Us to Schedule a Phone Call or Meeting.

Call us today! (540) 345-3891