Fourth Quarter Commentary

Despite plenty of geopolitical turmoil, lofty stock market valuations, and a Federal Reserve focused on increasing interest rates, 2017 was an exceptionally “normal” year for the stock market. The monthly returns of the broad global equity index were normally distributed with no tails of extreme positive or negative performance, which is very rare. For the first time in 90 years, the U.S. stock market posted positive gains in each of the twelve calendar months, while volatility hovered near historic lows. Volatility was so low that there were no days in 2017 with a market drop of at least 2%. In the preceding three decades, a drop of at least 2% occurs, on average, ten times per year.

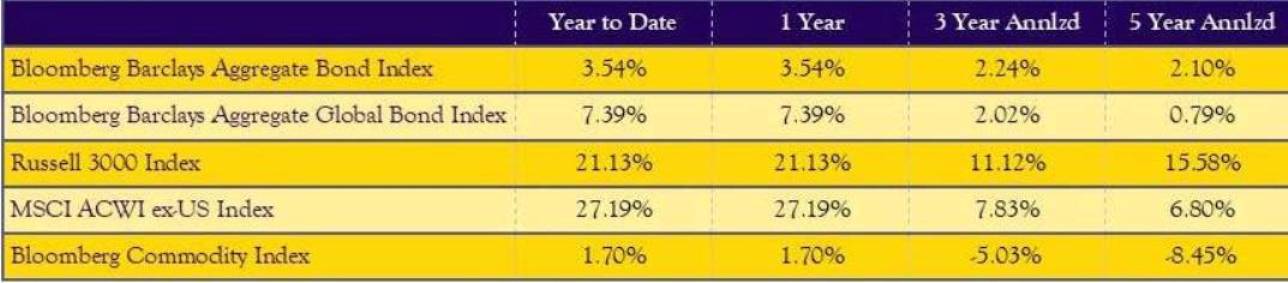

The lack of volatility combined with a 16% rise in global equity earnings gave stocks quite the tailwind. The Russell 3000 Index, which measures the performance of small, mid, and large cap domestic stocks, returned 6.34% for the quarter and a stunning 21.13% for the year. Large cap stocks outperformed small cap stocks by more than 7% as the declining dollar benefited multi-nationals and as the technology sector, which comprises the largest portion of the large cap index, vastly outperformed the other equity sectors.

INTERNATIONAL EQUITY

The international MSCI ACWI ex-US index climbed 5.0% for the quarter and 27.19% for the year – beating domestic stocks for the first calendar year since 2012. The quarterly returns were well-distributed geographically, with the exception of the Eurozone. Euro-area stocks suffered a slight decline on the collapse of the German coalition-building efforts and the unrest in Catalonia but remain poised to reassert their upward trend given relative valuations and positive growth dynamics. Emerging markets fared well and increased 7.44% for the quarter on rising commodity prices.

FIXED INCOME

Fixed income returns were quite muted as the Federal Reserve continued on their path of hiking interest rates. The investment grade Barclays Aggregate Bond Index returned 0.39% for the quarter and 3.54% for the year. Narrowing credit spreads have reduced yields for many fixed income sectors – leaving investors with heightened risk relative to reward. Despite the asymmetric tradeoff, high yield bonds fared better than their investment grade counterparts with returns of 0.41% for the quarter and 7.48% for the year as investors continued to prefer risk assets in a yield-starved environment.

Although the Fed has been increasing short-term interest rates, intermediate- to longer-term U.S. Treasury yields have yet to advance significantly as strong overseas demand and geopolitical tensions have constrained the longer part of the yield curve. The gap between short- and long-term interest rates in the U.S. recently narrowed to the lowest level in over a decade. The “flattening” of the yield curve is concerning given that an inverted yield curve (whereby long-term interest rates are lower than short-term interest rates) has historically been a reliable indicator of future economic downturns. In fact, an inverted yield curve has predicted the last seven recessions since 1970. We will be watching this closely for further deterioration. However, we see no cause for alarm at this juncture given that the gap would need to narrow further before the curve inverts and because the curve usually inverts well before the stock market peaks.

TAX CUTS CREATE OPPORTUNITIES

With the Republican-led tax cuts now signed into law, there are some investment implications to consider heading into 2018. For corporations, a lower U.S. corporate tax rate is likely to boost high-tax sectors such as banks, telecom, and consumer discretionary stocks. In addition, smaller corporations with primarily domestic operations currently face higher effective corporate tax rates than large corporations with operations overseas and should benefit most from the tax cuts. Because the tax cuts are likely to boost corporate earnings in some sectors of the economy more than others, investors like ourselves, who focus on actively managing portfolios instead of on investing in passive indices, should be able to benefit from unique opportunities stemming from the tax cuts as they arise.

LOOKING AHEAD

Over the last twelve months we have witnessed the best period of coordinated, above-trend global growth in both developed and emerging economies in almost a decade. The pickup in global growth and manufacturing looks set to accrue further to corporate earnings over the next year. Increases in corporate earnings combined with easy monetary policy and low inflation is conducive to an environment that is supportive of risk assets. However, given the run over the last year and the euphoria we are seeing in some segments of the market, expectations should be tempered.

It is important to remember that, although rare, bear markets can occur in the absence of a recession. With investor sentiment so high, credit spreads tight, cash allocations hovering near historic lows, and leverage near highs last seen in 2007, volatility can increase rather quickly. Additionally, with interest rates still so low, fixed income provides less of a buffer to stock market declines than it has historically. Because of this, we are continually looking for managers to add to our portfolios to enhance overall diversification and will make changes to the portfolios as warranted.

Thank you for your continued confidence. As always, please reach out to us with any questions you may have. We wish you a blessed 2018!

Hillary Sunderland, CFA

Chief Investment Officer

3 Risks to the Rally

1) Credit Spreads

The limited spread-tightening potential of corporate bonds combined with interest rates near historic lows could lead to increased volatility in the bond market as the Federal Reserve tightens rates. Leverage in credit has increased, and the economic cycle is approaching the point when credit spreads have historically started to turn.

2) Valuations

Stock market valuations continue to be stretched by almost all common valuation metrics as bond yields remain near historic lows.

3) Geopolitical

Although policy uncertainty has faded, it could re-emerge in 2018 as mid-term elections reignite US partisanship.

Continued tensions with North Korea is a cause of uncertainty surrounding the potential effects on the Asian region.

Italian elections and the Brexit also possess disruptive clout.

Economic Backdrop

GROWTH

In the third quarter of 2017, economic growth registered the fastest growth rate since 2014 – hitting an annualized rate of 3.2%. We expect economic growth to remain robust for the fourth quarter reading of gross domestic product given hurricane rebuilding efforts as well as fiscal stimulus. Overall recession risk remains low, and developed market growth remains above-trend.

EMPLOYMENT

In November, the unemployment rate remained at 4.1% while the labor force participation rate (the number of people who are employed or who are actively looking for work) registered a reading of 62.7%, which is near its long-term average. While the U.S. is technically at full employment, the unemployment rate is largely expected to decrease even further in 2018.

INFLATION & INTEREST RATES

Solid economic activity and tight labor markets across the globe have yet to produce a decisive uptick in inflation. In November, U.S. core inflation (inflation less food and energy) fell to 1.7% year-over-year on declines in apparel and housing while the headline consumer price index rose to 2.2% on the back of higher gasoline prices. Our view is that there is limited risk of inflation rising sharply given that wages and oil prices remain contained.

Tame inflation has allowed central banks around the globe to remain fairly accommodative. In October, the European Central Bank reiterated that short-term interest rates will remain unchanged until well after the end of quantitative easing. The Bank of Japan kept policy unchanged as well. In a much-forecasted move, the Federal Reserve hiked interest rates by 0.25% in December, and projections indicate three additional rate hikes in 2018.

Index Returns

Source: Morningstar® as of December 31, 2017

Disclosures

Financial Planning and Investment Advisory Services offered through Beacon Wealth Consultants, Inc., a Registered Investment Advisor.

The material has been prepared for informational purposes only and is not intended to provide, nor should it be relied upon for, accounting, legal, or tax advice. References to future returns are not promises or estimates of actual returns a client portfolio may achieve. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. Information and data referred to in this document has been compiled from various sources and has not been independently verified. We believe the information presented here to be reliable but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase of any financial instrument. The views and strategies described may not be suitable for all investors.

All returns represent total returns for the stated period. The Bloomberg Barclays Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The Bloomberg Barclays Global Aggregate Index is a flagship measure of global investment grade debt from twenty-four local currency markets. The S&P 500 Index is a market capitalization weighted and unmanaged group of securities considered to be representative of the stock market in general. The Russell 3000 Index is a market capitalization weighted index that measures the performance of the largest 3,000 companies representing approximately 98% of the investable U.S. equity market. The Russell 2000 Index is a market capitalization weighted index that measures the performance of the smallest 2,000 companies in the Russell 3000 Index. The MSCI ACWI ex-US Index is a market capitalization weighted index designed to provide a broad measure of equity market performance throughout the world and is comprised of stocks from both developed and emerging markets outside of the U.S. The Bloomberg Commodity Index is designed to be a highly liquid and diversified benchmark for commodity investments.

Past performance is not indicative of future results. Diversification does not guarantee investment returns and does not eliminate the risk of loss. You cannot invest directly in an index.