In this month’s Market Commentary, Beacon Wealth’s Director of Financial Planning Jake Preston and Chief Investment Officer Hillary Sunderland discuss what’s driving today’s strong markets and what investors can expect as we close out 2025.

👉 In this update, you’ll learn:

- Why stocks defied seasonal trends to deliver strong third-quarter returns

- How global diversification has paid off in 2025

- What to make of record market highs and why new highs aren’t necessarily a reason for concern

- The latest on inflation, interest rate cuts, and the potential effects of new tariffs –How the federal government shutdown could impact the economy and markets

- What all this means for your faith-based investment strategy

Hillary also shares key insights on earnings trends, fixed income performance, and the importance of staying invested for the long term, not trying to time the market.

💡 At Beacon Wealth Consultants, we help Christian investors align their portfolios with their faith and values through Biblically Responsible Investing (BRI).

📞 Have questions about your portfolio? Give us a call!

Transcript

Jake Preston

Well, hello everyone. I am Jake Preston, the Director of Financial Planning here at Beacon Wealth, and I am joined again today by our Chief Investment Officer, Hillary Sunderland. Hillary, it’s great to be with you again.

Hillary Sunderland

Great to be with you, Jake.

Jake Preston

And we are looking forward to providing you with an update on the markets, unpacking what has happened in the third quarter of this year, as well as looking ahead through year end. And so Hillary, first, could you give us a recap of how the major areas of the market have performed during the third quarter?

Hillary Sunderland

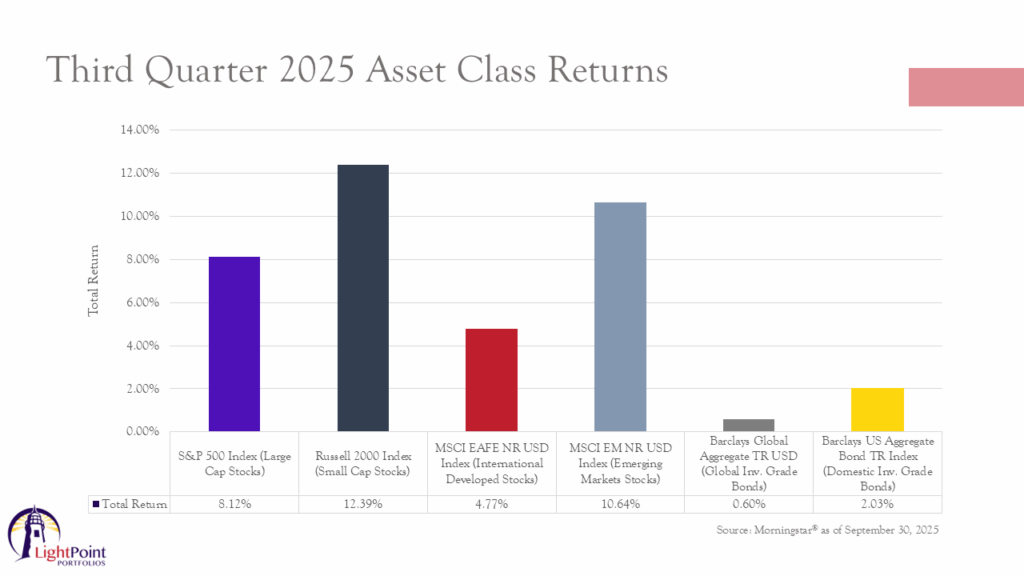

Sure. Well, while August and September are usually fairly weak months for stocks, this year bucked that seasonal trend. Artificial intelligence continued to be a really powerful theme in the markets, and that fueled investor demand for tech stocks, particularly those involved in AI and cloud services.

We also saw really resilient corporate earnings, and the Federal Reserve cut interest rates during the quarter as well, which boosted investor sentiment. So for the quarter, we had a really good, really good returns across the board. Domestic large cap stocks rose 8.12 percent, small cap stocks fared a bit better, returning a little over 12. Outside of the U.S., developed international rose by almost 5 percent, while emerging markets, which includes countries like China and India, they rose just over 10 percent. And fixed income posted small but positive returns for the quarter also.

Jake Preston

So it sounds like we had a very strong third quarter. So can you tell us a little bit about how the markets are shaping up for the year overall?

Hillary Sunderland

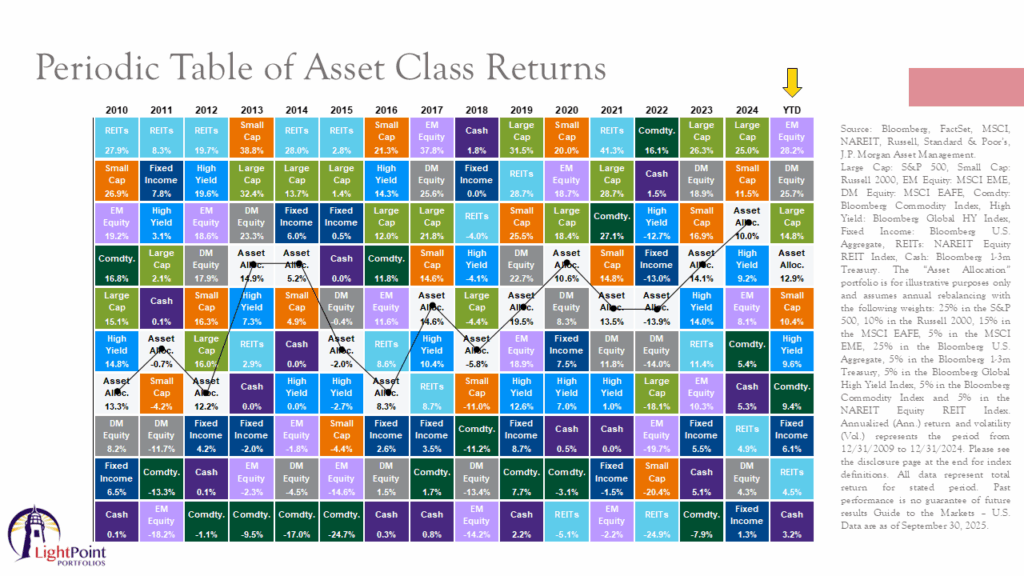

Yeah, so so far this year, markets have shown remarkable strength. This chart is the periodic table of asset class returns, and it ranks asset classes from the best performance to the worst performance for each calendar year. And I like it because it’s a really powerful visual of how different investments can go in and out of favor over time and what has stood out.

In 2025 is the clear advantage of global diversification markets outside of the U.S. So those light purple and gray boxes there have outperformed domestic large cap stocks by more than 10 percent. And that’s really a sharp contrast to 2023 and 2024 when U.S. large caps and a handful of mega cap companies led the charge with double digit gains. The shift really reminds us that the leadership in markets is always evolving and diversification remains key.

Earlier this year, we also discussed how starting yields made a very powerful case for bonds over cash. And that outlook has proven accurate. Fixed income has also delivered strong performance year to date.

It’s up a little over 6 percent. And this is, you know, despite the Federal Reserve not lowering rates as much as we thought they would, the Fed has maintained interest rates higher throughout most of the year than we expected coming into the year. And so while cash has held up and has had good yields, it’s also lagged significantly, landing in the bottom of return rankings with a return of only 3.2 percent year to date. So it’s a clear reminder that it doesn’t always pay to sit on the sidelines in cash.

Jake Preston

Yeah, for sure. And to your point, you know, it underscores the importance of having a globally diversified portfolio, not getting overly concentrated in one area. It’s really fascinating to think about where we were earlier in the year, just in early first quarter, the S&P 500 was down 20 percent.

And to see such a robust year in returns now here at the end, beginning of the third quarter, beginning of fourth quarter, which kind of brings up a question, with such positive performance for the year in the markets, should investors be worried that stocks are hitting new highs?

Hillary Sunderland

Well, that’s an interesting question, Jake. And it’s one that I hear often. As markets hit new highs, it does make some investors uneasy, just as new lows during a bear market can cause some hesitation.

But investing at all time highs isn’t necessarily a bad thing. Ultimately, what we want is for stocks to be hitting new highs. And if you think about it logically, what really drives the value of any business is earnings.

So as companies make more money, they should see the values of their companies go up over time. And this year we had really good earnings season. And so while stocks are hitting new highs, earnings have also been strong, which is a good fundamental backdrop.

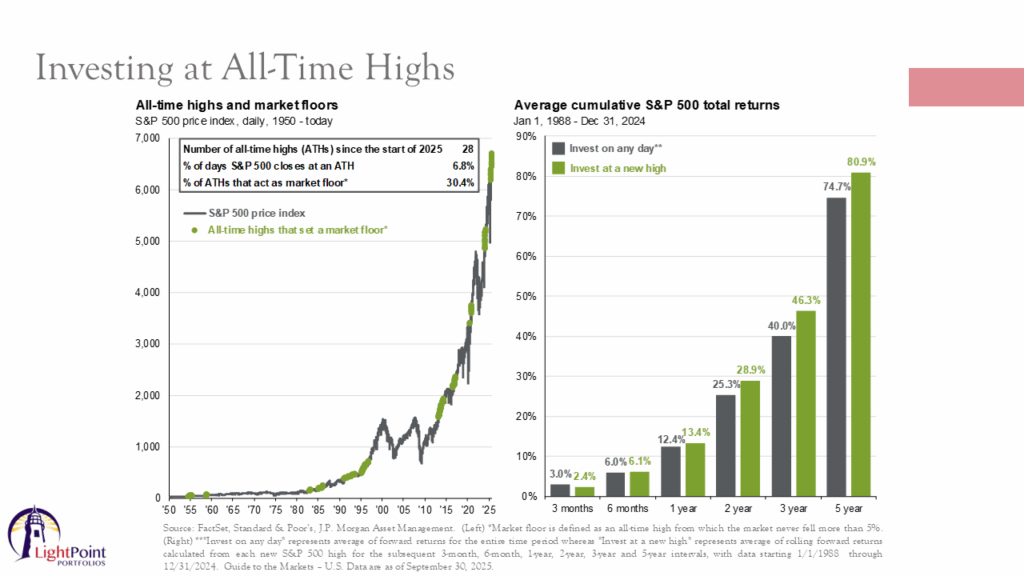

I thought it’d be good to show you this chart, which I thought was fascinating. The green bars on the right represent the average forward returns when investing in the S&P 500 at a new high, while the gray bars show the average returns from investing on any random day. And surprisingly, since 1988, investors have actually done better by buying at new highs than by trying to time a better entry point in investing on any other given day.

As shown on the left-hand side of the chart, since 1950, 30% of the time that the S&P 500 closes at a new high, that acts as a market floor. So seeing on the news that the market closed at a new high should not necessarily be concerning to investors. That is ultimately what we want to see in the markets.

But all that being said, it’s also important to remember that markets don’t typically move in a straight line up. Valuations are currently elevated, which makes the market more sensitive to any negative surprises. Earnings season is just around the corner.

So in about two weeks, earnings are going to start to roll in and any disappointing results could trigger some shorter term market volatility. Historically, we do tend to see a correction, which is defined as a drop of at least 10% from a high. That typically occurs once per year, and we typically see pullbacks of at least 5% occur three times per year.

And as you stated, Jake, the last notable drawdown really came in the spring following the tariff announcement. Right now, stocks appear to be a little bit overbought, and I would personally welcome a period of consolidation. But the key here is that I would view any near-term weakness as a buying opportunity.

Market participation has broadened out across sectors and across different sizes of companies. It’s not just a few companies leading the market higher this year, it’s very broad-based. And fundamentally, corporate earnings have exceeded expectations and forward earnings are expected to be very good as well.

So together, all of these factors really support a continuation of the current uptrend as we head toward year end.

Jake Preston

That’s really interesting and helps to kind of clarify and set some realistic expectations. It takes me back to the quote where it talks about how investing success is determined not by trying to time the market, but by time in the market. And I think that’s a helpful reminder for all of us.

So let’s switch gears a little bit and talk a bit about inflation. So it’s likely that many of us have seen in the headlines that the Federal Reserve is starting to cut interest rates. And so a question that might result from thinking about those lowering interest rates is, should we be worried about inflation coming back again?

Hillary Sunderland

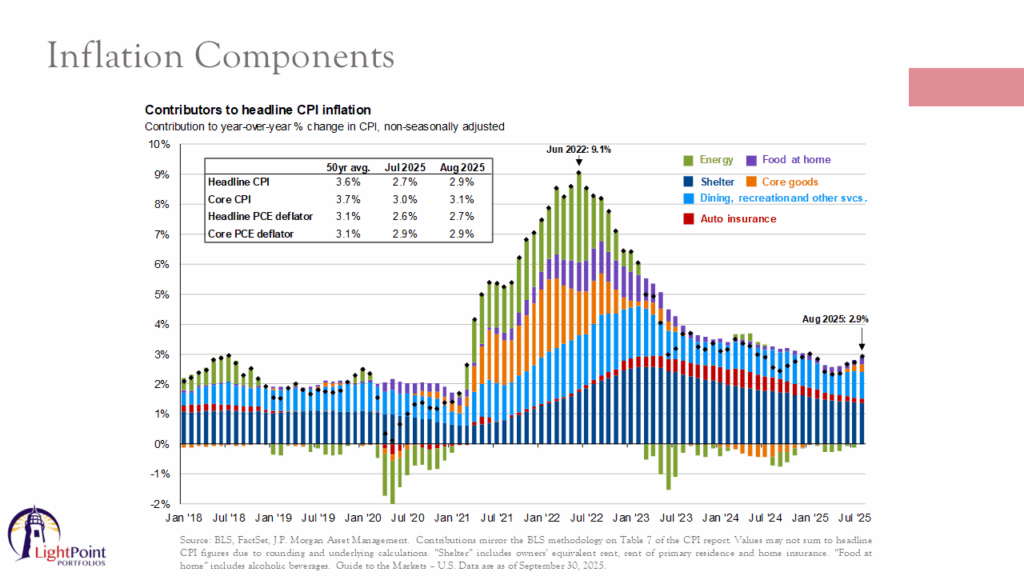

Yeah, that’s a question I get a lot. And I think about a lot too, as I go to grocery shopping every week. Inflation peaked back in June of 2022, over three years ago, as you can see on this chart.

And while we haven’t quite reached the Fed’s 2% inflation target, inflation has eased significantly depending on the measure that you use. When I say that inflation is falling, it’s important to note that doesn’t mean prices are falling. It simply means that prices are rising at a slower pace than they were before.

We’re currently sitting in the upper twos to low 3% range on inflation. What I really want you to zoom in on here is, if you look at the orange bars in the center of that chart, that orange bars represent core goods, which saw significant inflation during the pandemic due to supply and demand imbalances. That pressure is starting to reemerge, as we saw in August.

These same goods are now facing steep tariffs. And while retailers haven’t yet passed on those costs to consumers, we do believe that they will. Inflation is likely to rise gradually and may not peak again until the summer of 2026.

But we don’t anticipate a sharp or sustained spike, more of a temporary bump before stabilizing once again. And just one more thing to note, as this has also been on the news, we do think that tariffs are likely to stay. There was a recent ruling by the Court of Appeals that President Trump exceeded his authority by declaring a national emergency to impose tariffs in the first place.

That case is now headed to the Supreme Court with opening arguments scheduled for the first week of November. And opinions are really divided on how the Supreme Court might rule on that. If they uphold the appeals court decision, it can mean the original basis for the tariffs is invalid.

However, it is important to note that the Trade Protection Agreement includes alternative provisions that could still allow for tariffs to be implemented under different legal grounds. And so we do think that the tariffs are likely to stay in place, which should cause a temporary, shorter term bump in inflation over the next couple of months.

Jake Preston

Okay, very helpful. Thanks for sharing that. We’ll be keeping an eye on that case.

So shifting gears one final time to something that is really dominating the headlines right now is the fact of the federal government shutdown. And so can you just explain a little bit about the both the economic and the market implications of the shutdown and how it might impact investors?

Hillary Sunderland

Sure. Well, unfortunately, government shutdowns are nothing new. And while they do create a drag on economic growth, the impact does tend to be modest if the shutdown is brief.

Certain federal activities like loans and grants, those come to a halt, and federal workers may go unpaid temporarily. Now, historically, those working through the shutdowns have been reimbursed afterward. But the longer it lasts, the more it disrupts the economic momentum and creates uncertainty, especially as government data becomes increasingly scarce.

And this lack of government data, such as what’s going on in the jobs front, and such as leaving a lot of gaps in the economic picture, those gaps are going to widen the longer the shutdown persists. So we do expect the economy to, you know, go through a temporary soft patch for picking up again next year. We don’t have a booming economy right now.

But it’s also not signaling an imminent recession or stagflation either. From an investment standpoint, we wouldn’t recommend making any major changes based on the shutdown alone. It’s unclear how long it’ll last.

And at this point, it hasn’t altered our broader outlook. The longer the shutdown continues, the more likely it is that the Federal Reserve will respond with interest rate cuts. Because as we have a lack of data coming through on different parts of the economy, such as jobs, they’re probably going to want to be more conservative and cut rates more quickly, just to make sure that it doesn’t cause an issue down the road.

And their next meeting is at the end of October. We anticipate that they’ll cut rates then and likely again in November as well.

Jake Preston

Great. Well, this has all been incredibly insightful for me. And I’m sure it has been for everyone watching as well.

Thank you so much, Hillary, for all that you and your team do. And thanks to you for watching. If you have any questions, we would be glad to answer those for you.

You can reach out to your advisor. And we look forward to seeing you at our next market commentary update.

Hillary Sunderland

All right. Thanks, Jake.

Sign up for our newsletter!

Get news, market commentaries, videos, and faith-based investing articles from Beacon Wealth Consultants in your inbox.