The U.S. economy grew at a 4.2% annualized rate in the second quarter – marking the most rapid growth in the last four years as massive tax cuts for companies acted as a considerable stimulus for the economy. Approximately 83% of U.S. companies beat second-quarter earnings estimates, and sales growth remained strong. The U.S. unemployment rate continued to hover near 18-year lows, while inflation remained stable. Overall, this positive economic backdrop translated into nice returns for the domestic stock market with the Nasdaq, S&P 500, and Russell 2000 Indices all hitting record highs in August.

While we are pleased with the performance of U.S. stocks this year, performance at the portfolio-level has left many investors scratching their heads. The S&P 500 is up almost 10% year-to-date, but many investors have captured portfolio returns that fall well short of that. For example, many moderate investors (i.e., investors with allocations of 50% to 60% stocks) have captured portfolio returns in the 2.5% – 3.5% range gross-of-fees year-to-date. The reason for the difference inportfolio-levelperformance versus the performance of broad U.S. stock indices is largely due to prudent diversification, including significant allocations to bonds.

Diversification is the act of spreading investments across a variety of asset classes and styles. The bible recommends diversification in Ecclesiastes 11:2, “Divide your portion to seven, or even to eight, for you do not know what misfortune may occur on the earth.” Assuming the investments you own don’t move in lock-step with one another, there is an inherent benefit to owning a wide variety of asset classes that are likely to react differently as market conditions change. Inevitably, asset classes go out of favor, which can result in significant losses to investors who are not properly diversified.

The difficult aspect of diversification, and one that is rarely spoken of, is that owning some laggards is built into the equation. Because people dislike “owning losers,” emotionally, it can be difficult to stick with a diversified portfolio during periods of time when one or two asset classes are dominating the rest, and that is exactly where we are this year.

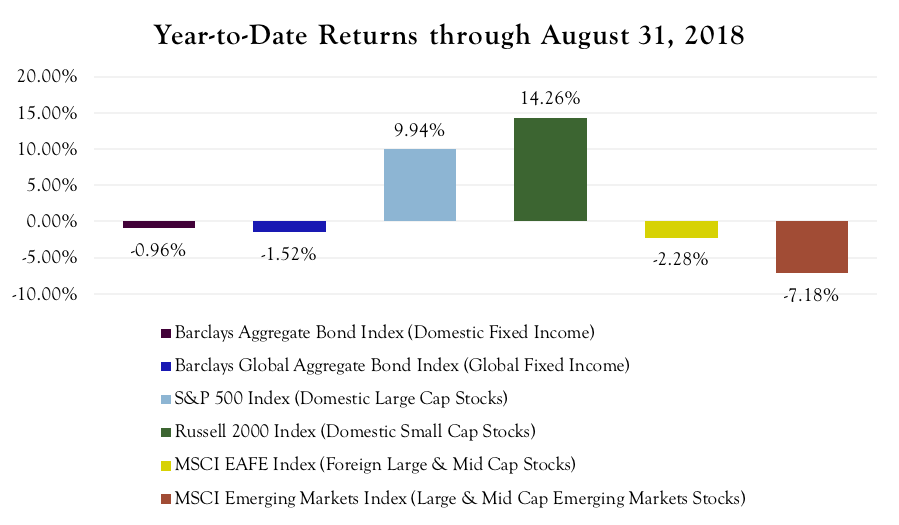

As shown in the chart below, U.S. stocks have significantly outperformed both bonds and foreign stocks. The S&P 500 Index has outperformed the MSCI EAFE Index by over 12% and has bested emerging market stocks by over 17%. Bonds remain negative for the year with a return of -0.96% as rising interest rates continue to pressure returns.

Source: Morningstar® as of August 31, 2018

Source: Morningstar® as of August 31, 2018

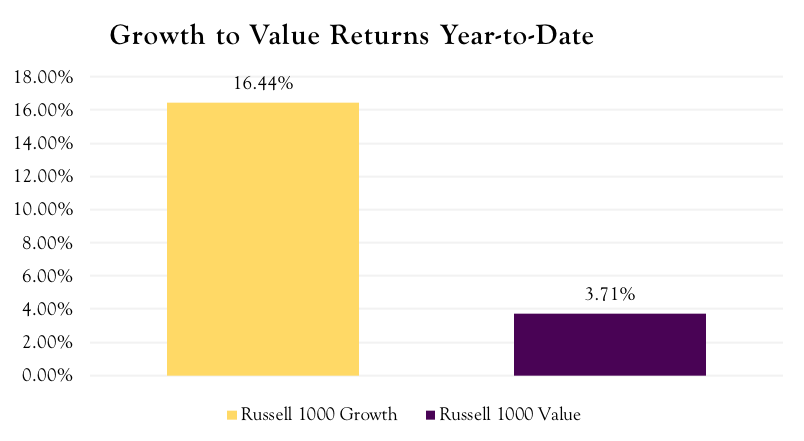

Additionally, there has also been a marked divergence between the performance of domestic growth stocks (e.g., U.S. companies that are anticipated to grow at a rate significantly above average for the market) and the performance of value stocks (e.g., U.S. companies that are thought to be undervalued by the market relative to comparable companies) – resulting in frustrating returns for conservative investors who tend to be more focused on dividend-oriented value stocks to generate income.

Source: Morningstar® as of August 31, 2018

Source: Morningstar® as of August 31, 2018

In this type of environment, portfolio performance that is well short of the S&P 500 Index is expected for diversified investors, but we believe it will be short-lived. International stocks are currently trading at significant discounts to U.S. stocks, and the U.S. dollar is likely to come under pressure over the next 12-18 months, which would benefit investors in international stocks. Additionally, the disparity between growth stocks and value stocks is at an extreme not seen in over a decade.

While bond returns are likely to remain low, we caution investors against reaching for performance at this stage. The outlook is murky in the short-term as trade disputes continue to take center stage, and September is typically a difficult month for the stock market. We monitor the market continually and will make changes to the portfolios as warranted.

Thank you for your continued confidence. Please reach out to us with any questions you may have.

-Hillary Sunderland, CFA®, CKA® Chief Investment Officer for Beacon Wealth Consultants, Inc.

Disclosures

Financial Planning and Investment Advisory Services offered through Beacon Wealth Consultants, Inc., a Registered Investment Advisor.

The material has been prepared for informational purposes only and is not intended to provide, nor should it be relied upon for, accounting, legal, or tax advice. References to future returns are not promises or estimates of actual returns a client portfolio may achieve. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. Information and data referred to in this document has been compiled from various sources and has not been independently verified. We believe the information presented here to be reliable but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase of any financial instrument. The views and strategies described may not be suitable for all investors.

All returns represent total returns for the stated period. The Bloomberg Barclays Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The Bloomberg Barclays Global Aggregate Index is a flagship measure of global investment grade debt from twenty-four local currency markets. The S&P 500 Index is a market capitalization weighted and unmanaged group of securities considered to be representative of the stock market in general. The Russell 3000 Index is a market capitalization weighted index that measures the performance of the largest 3,000 companies representing approximately 98% of the investable U.S. equity market. The Russell 2000 Index is a market capitalization weighted index that measures the performance of the smallest 2,000 companies in the Russell 3000 Index. The MSCI ACWI ex-US Index is a market capitalization weighted index designed to provide a broad measure of equity market performance throughout the world and is comprised of stocks from both developed and emerging markets outside of the U.S. The Bloomberg Commodity Index is designed to be a highly liquid and diversified benchmark for commodity investments.

Past performance is not indicative of future results. Diversification does not guarantee investment returns and does not eliminate the risk of loss. You cannot invest directly in an index.